For years, the Magnificent Seven tech giants commanded investors’ attention, dominating the S&P 500 Index and determining which way the overall stock market was headed. Those days are over.

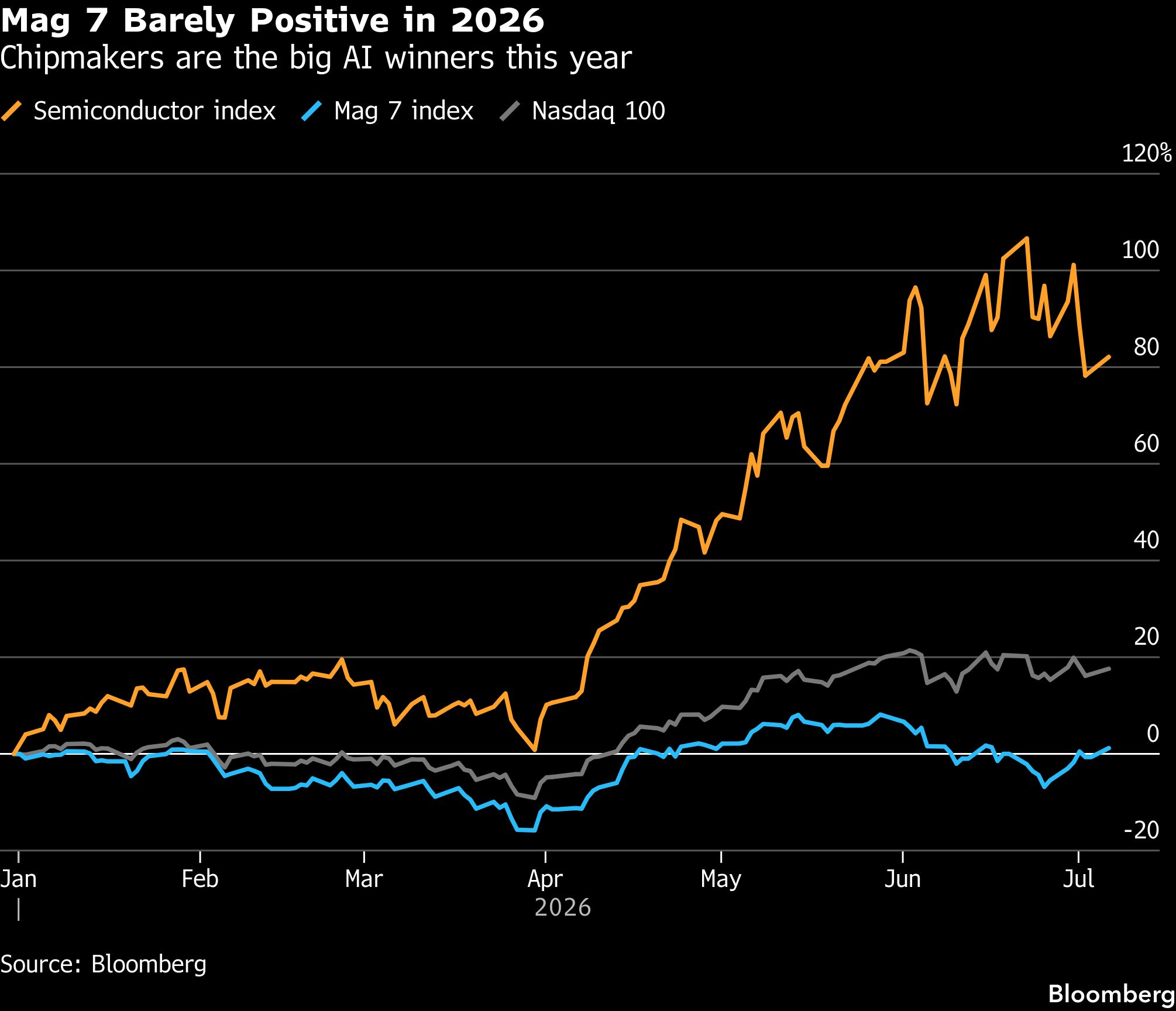

While the technology-heavy Nasdaq 100 Index is up almost 18% in 2026 and the S&P 500 has climbed 10%, an index of the Mag 7 has gained just 1.1%. The artificial intelligence trade that made a market force out of those tech behemoths — Nvidia Corp., Alphabet Inc., Apple Inc., Microsoft Corp., Amazon.com Inc., Meta Platforms Inc. and Tesla Inc. — is still on. But it has changed.

Investors are now focused on the biggest beneficiaries of the wave of cash dedicated to building out AI. At the same time, they’re growing skeptical of the companies doing the spending. That has put memory chipmakers like Micron Technology Inc. and Sandisk Corp. at the top of the leaderboard, while relegating the Mag 7 stocks to something of an afterthought. The Philadelphia Stock Exchange Semiconductor Index is up 82% 2026, on pace for its best year since 1999, and is coming off its best quarter ever.

“The Mag 7 used to be one of the only places you could go to reliably get earnings that were much better than the market,” said Brian Barbetta, co-head of Wellington Management’s technology team and co-portfolio manager on the global innovation strategy. “People are now more focused on reasons to not like them.”

To get a sense of how quickly this has turned, consider that in April the Mag 7’s 40-day correlation to the Nasdaq 100 peaked at above 0.95, a near-perfect correlation. It recently dropped below 0.7, its lowest since 2017. Big tech and the S&P 500 “are moving together about as little as they were in 2015, when these names were only 10-11 pct of the index,” Jessica Rabe, a co-founder at DataTrek Research, wrote in a note to clients on June 30.

Yet the seven tech giants still represent roughly 37% of the Nasdaq 100’s weight and almost a third of the S&P 500.

The decoupling of the Mag 7 from the broader market is perhaps the clearest reflection of how the AI trade is evolving to focus on the new winners, notably memory and storage chipmakers. They’ve been hot for a while, but what’s different now is the group is moving largely without Nvidia, the erstwhile AI bellwether that has long dominated the stock market. This year, however, it’s the third worst stock in the semiconductor benchmark with a paltry 4.9% gain.

Among the remaining six stocks in the Mag 7, performance has been mixed. Three are in the green, with Alphabet leading the way based on the perception that it’s likely to emerge an AI winner. Microsoft, on the other hand, is down 20% and June was its worst month since 2000 due to twin concerns about its aggressive AI spending and its vulnerability to the technology as a software maker.

As a result, investors pulled $786 million in June from the Roundhill Magnificent Seven ETF, the most on record, while pouring $9.3 billion into the Roundhill Memory ETF, according to data compiled by Bloomberg. “Positioning in large-cap tech was ‘extreme’ at the end of May” but has “now returned to a more neutral stance,” Deutsche Bank strategists wrote in a June 30 note.

Skepticism about heavy spending on AI is largely behind the rotation. Microsoft, Amazon, Alphabet, and Meta are dramatically accelerating their capital expenditures, which is weighing on their cash flows while it isn’t clear how well those investments are paying off.

“Markets are now debating whether cloud companies will see less compelling returns on capital and margins,” Barbetta said.

Meta CEO Mark Zuckerberg reportedly told a company town hall that its AI agent development has not “accelerated in the way we expected.” The company also is reportedly developing plans for a cloud infrastructure business to sell excess computing power. That AI spending has gone straight to memory chipmakers like Micron and Sandisk.

“Investors go where growth and returns are the strongest,” Barbetta said. “Right now companies like Micron and Sandisk are not only growing earnings faster, but they’re seeing some of the strongest positive estimate revisions.”

That said, not everyone on Wall Street is convinced the rotation is here to stay. The gap will ultimately be resolved “as hyperscalers and AI model providers as well as users see improvements in monetization, revenues and earnings and they start to catch up, capturing a bigger share of the overall AI value added pie,” JPMorgan global market strategist Nikolaos Panigirtzoglou wrote in a July 1 note to clients.

Meanwhile, momentum in chip stocks appears to be fading as investors shift back to this year’s laggards, including AI hyperscalers, according to Morgan Stanley’s US equity strategy team, led by Mike Wilson. “You can’t have this divergence continue, it’s not sustainable,” Wilson said.

However, the earnings momentum needed for Big Tech to flip the narrative just isn’t there — at least not yet. The Mag 7 are expected to post an 18.9% increase in net income next year, but three months ago that estimate was 21.4%, according to Bloomberg Intelligence. Earnings estimates for chipmakers, on the other hand, have been revised dramatically higher in the past three months, to 48.5% from 34.3%, Bloomberg Intelligence data shows.

This alone is why the Mag 7 stocks are likely to continue trailing the current leaders for the foreseeable future, said Mark Lehmann, vice chair of commercial banking at Citizens.

“The Mag 7 are still relevant, but investors used to be very sure about their prospects, and now there’s more disbelief and more debate about how much you should pay for them,” he said. “Their earnings look second or third tier compared to Micron and Sandisk, and expectations keep rising for those companies. It’s hard to see how the Mag 7 can compete with that.”

Tech Chart of the Day

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Ryan Vlastelica