We don’t usually think of rising rates as being good for homeowners. That may be because we’re accustomed to thinking of financing (and refinancing) as the key to reviving sagging housing markets. And it’s true that financing availability remains tight, at least by historical standards, and isn’t going to get looser with rising rates.

Instead, it’s about the proverbial rising tide that floats all boats: the improving economy led to the Fed signaling that it will soon begin to taper its bond-buying program, and that led in the last few weeks to a sharp rise in intermediate- and long-term interest rates. And, the same improving economy led to more residential buyers on the market and consequently to rising home prices.

In a neat virtuous circle, rising home prices helped to further improve the economy. Home prices continue to increase, driven by very tight inventory levels of new, existing and distressed properties for sale.

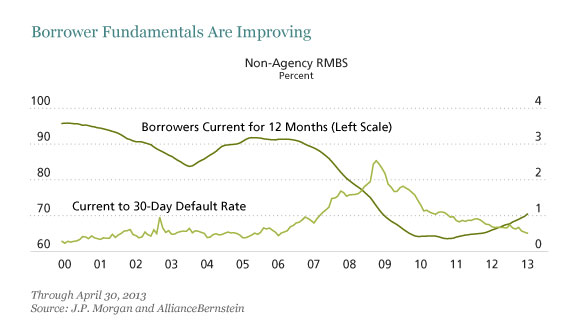

We expect these improving housing fundamentals to translate into better performance for the collateral underlying non-agency residential mortgage-backed securities (RMBS) and commercial mortgage-backed securities (CMBS). Specifically, we anticipate lower default rates and loss severity, as shown in the display below.

Window Opens with Wider Spreads

That sharp rise in interest rates over the past few weeks created considerable global volatility across the financial markets, with “risk-free” and riskier assets experiencing a hit at the same time—an unusual occurrence, as explained here.

Less liquid assets were hit particularly hard. Legacy non-agency RMBS and CMBS “AJ” prices declined on average five to 10 points between late May and the end of June, with loss-adjusted yields returning to levels last seen near the end of 2012. Trading volume is low and bid/ask spreads have gapped out.

We see this as an entry point. Over time, improving collateral performance, derived from better fundamentals, should serve as a catalyst for spread tightening.

In our view, a carefully chosen and managed portfolio of non-agency RMBS and CMBS may help to diversify a traditional fixed-income allocation. Past experience has taught us that even though periods of elevated volatility can persist (especially when pegged to government policy), investors with a longer-term investment horizon can view this as an opportunity to enter the market when fundamentals are attractive and spreads are wide.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

Matthew D. Bass is Vice President in the Fixed Income Group.

© AllianceBernstein