Key Points

- Stocks have struggled a bit lately, but the overall damage is still relatively minimal. A further pullback seems possible, but could likely be a buying opportunity.

- The labor market has picked up steam, with various segments of the economy improving. Wage increases are gaining some traction, but the Fed remains dovish; as such, there is growing concern it may be falling behind the curve.

- Economic growth in the eurozone has weakened, but we believe it's a temporary slowdown; while both European and Chinese equities look like attractive, against-the-grain opportunities for the relatively risk-tolerant investor.

The long bull market in the United States remains intact but there have been some recent stumbles. We would like to see some further selling in order to correct some of the overly optimistic sentiment (a contrarian indicator) that's built up. The Ned Davis Research Daily Crowd Sentiment Poll recently hit its most optimistic level since the end of last year, near levels that have typically preceded a relatively decent pullback. Additionally, midterm election years (like 2014), have historically brought decent-sized pullbacks in each year going back to 1962—ranging from -8% to -38% with the average decline being -19% (thanks to Strategas Research Partners), but those pullbacks have been followed by substantial rallies over the subsequent 12 months, ranging from 12% to 58% and averaging a whopping 32%. We haven't seen that type of pullback yet, and history doesn't always repeat, but it does often rhyme. Bottom line—in our view the possibility of correction is elevated, but we would view such an occurrence as a buying opportunity for those who have been under allocated to equities.

Valuations are being debated, with concerns about overvaluation growing—exacerbated by comments from the Fed related to biotechnology and social networking stocks. Given continued low interest rates and inflation, the market can likely maintain higher valuations, and current levels are roughly inline with where history has shown they should be. So while the market is no longer a significantly undervalued story, we don't believe valuations have become an impediment to this bull market.

Second quarter earnings season and results overall should be better than expectations, as has been the trend over the past few quarters. Helping was the elevated negative preannouncement ratio coming into the reporting period. Market reaction will likely focus on forward-looking statements, as well as the top-line revenue growth, to determine whether demand is picking up. One thing we have noticed is that the market seems to be less forgiving of missed expectations or lower guidance, raising the bar for companies and risks for stockholders in the near term.

Modest growth continues—labor accelerates

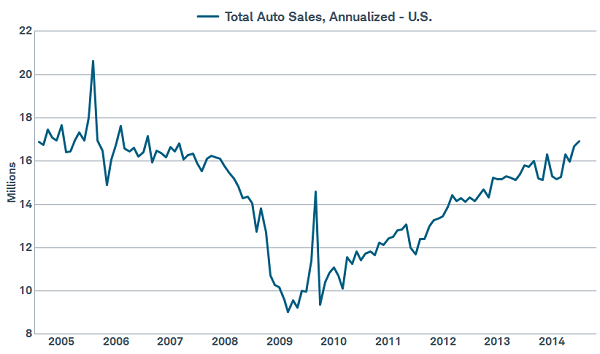

Fueling our continued confidence in the market beyond the short-term is the pickup in the economy. Growth has picked up from the weather-hit first quarter, while job growth has accelerated. First, the Institute of Supply Management's (ISM) Manufacturing Index ticked only slightly lower in June to a still robust 55.3 and even more encouraging for the future outlook was that new orders gained two points to 58.9. A similar story is unfolding on the service side as the ISM Non-Manufacturing Index fell slightly, but remained at a healthy 56.0, while new orders jumped to 61.2. Additionally, despite the spike in automobile recalls, auto sales reached their highest annualized level since February of 2006.

Autos' strength point to a better consumer environment

Source: Bloomberg. As of July 14, 2014.

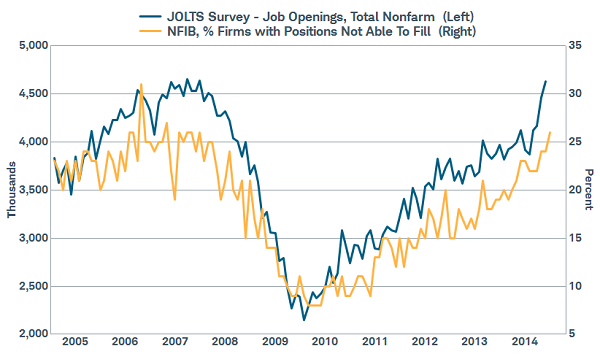

Most important has been the acceleration in improvement in the labor market. ADP reported June payrolls rose by 281,000 jobs, while the Bureau of Labor Statistics Labor Report showed an increase of 288,000. Previous months' readings were revised higher and the unemployment rate fell from 6.3% to 6.1%. And although the National Federation of Independent Business (NFIB) report showed that confidence declined a bit in the most recent reading, the number of businesses reporting that jobs were getting harder to fill grew. Finally, one report that has been largely ignored over the past several years, the JOLTS (Job Openings and Labor Turnover Survey) release, has gotten more attention as of late—largely because Fed Chair Janet Yellen has pointed to it as one of her favorites. In its latest release, job openings increased to the highest level since March 2007, while the "quits" rate also increased, indicating growing confidence in the labor market.

Labor market tightening?

Source: FactSet, Nat'l Fed. of Independent Business, U.S. Dept. of Labor. As of July 14, 2014.

Behind the curve?

With the improvement in the labor market, concerns are rising that the Federal Reserve could fall behind in its return to "normal" monetary policy. It is interesting to note that from the end of May to the beginning of July, the two-year Treasury note rose 16 basis points, to the highest level since September of last year. And while the official measure of wage gains continues to be relatively muted, signs are increasing that could accelerate in the near future. While this would be good news for workers, it could also fuel further gains in inflation that has already started to show signs of increasing. This could cause the Fed to move more quickly than the market is expecting. While we don't think rate hikes are imminent, the possibility of sooner-than-expected tightening is a growing risk in our view.

With "friends" like these…

While politicians talk about the need to improve the economy and get Americans back to work, they have turned their attention to "corporate inversions." Driving companies to acquire foreign companies is the benefit from the acquisition target's lower corporate tax rate. Most everyone agrees that the U.S. tax code remains unbelievably complex and the U.S. corporate tax rate is globally noncompetitive, as evidenced by the surge in inversions. Additionally, while the Fed wants banks to make more loans to get the velocity of money going, the regulatory burdens continue to grow. In fact, regulatory uncertainty is a growing anvil around the U.S. economy overall. Within the NFIB survey, there's a question about what's most vexing for small business—the combination of regulatory and tax policy ranks at the top of the list.

Europe slowing before it even gets started?

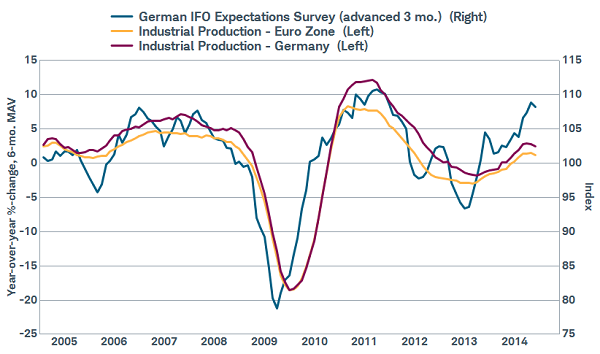

The eurozone was viewed to have emerged from recession after posting positive growth in aggregate beginning in the second quarter of 2013. However, the prolonged length of sustained slow growth has some economists questioning whether the eurozone recession actually ended or whether the recession merely paused. Indeed, recent economic data has disappointed, including declines in industrial production in Germany, France and Italy; as well as a decline in German factory orders and a fall in German and French business confidence.

Exporters such as Germany leading the decline

Source: FactSet, German Federal Statistics Office, IFO National Institute of Research, Eurostat. As of July 15, 2014.

There have been some glimmers of hope though, as Spain's manufacturing PMI rose to the highest level since the global financial crisis, Spanish employment has gained nearly 2% from a year ago, and Spanish home prices appear to have stabilized in recent months. Within the composite PMI for the euro zone, new orders rose to the highest level in three years, and the fall in prices was the smallest in two years in July.

We are concerned about the recent slowdown in the eurozone, but believe it is a temporary blip. This year has seen a rotation of one-off reasons for country-specific weakness: weather hitting the U.S. economy in the first quarter, a shadow banking crackdown hurting growth in the first quarter in China, and Japan's economy slowing in the second quarter due to the after-effects of a sales tax increase. A strong euro has also hurt export-oriented countries such as Germany. The crisis in Ukraine was cited as damaging business confidence in the German Ifo Business Climate Index – notably over 6,000 companies are active in Russia according to Reuters. It's possible economic activity continued to be suppressed in late June and early July due to World Cup distractions; and the onset of European holiday season isn't going to help in the near-term. In fact, this earnings season may be difficult for the stock market as companies could continue to miss estimates.

However, for investors who take a longer view, we believe the eurozone is on the mend and remain bullish on European equities. Lending appears to be bottoming, much-needed reform momentum is gaining ground in France and Italy, and the European Central Bank has committed to doing "whatever it takes", including pursuing outright bond purchases, if growth slips too far. Profit margins in the eurozone remain below the 2007 peak, and if the economy and corporate sales experience sustained improvement, earnings growth could outpace economic growth.

China's economy stabilizing

China, the world's second-largest economy, appears to be stabilizing, a positive development for the global economy. Second quarter gross domestic product (GDP) improved slightly to 7.5% from 7.4%. The pickup was the result of a number of targeted stimulus measures: increased railway spending and accelerating full-year spending by local governments; an easing of credit issuance due to targeted reserve requirement rate (RRR) cuts for qualified banks; and changes to the way loan-to-deposit ratios are calculated. The spillover effect has resulted in positive upside surprises to industrial production and home sales, which has prompted some economists to raise their 2014 GDP forecasts for China.

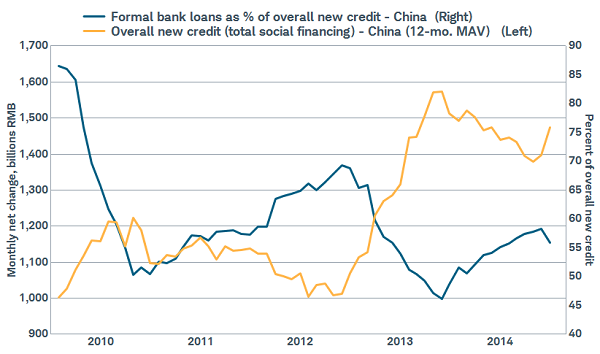

Credit has rejuvenated China for now

Source: FactSet, Bloomberg, People's Bank of China, National Bureau of Statistics. As of July 15, 2014.

It seems as though investors are hard to please however, finding reasons to be skeptical despite the better economic data and questioning the sustainability of the economic stabilization. In fact, the rapid growth of credit in recent years, particularly from sources outside formal bank loans, is a burden that could continue to suppress growth.

While there is the need for infrastructure spending in some interior portions of the economy, local Chinese governments are limited in their ability to spend. Obstacles to municipal spending include a heavy reliance on the shadow banking system and land sales for sources of funding, while pilots to allow local governments to access capital markets directly are just now starting. Additionally, a correction in the property market, which influences 23% of China's GDP according to Moody's Analytics, is likely to continue to stall home construction in coming months, even though the value of homes sold rose 33% month-over-month in June.

China's policymakers have embarked on a reform plan to transition away from debt-led investment growth. One aspect of this reform is to shift the focus of state-owned enterprises from being job maximizers to increasing return on investment. While theoretically this would involve closing unused excess capacity, in practice this is difficult to do because it could cause job losses and social unrest, something the government is simultaneously trying to avoid. Excess capacity has hurt company profits and resulted in 28 months of negative producer prices. As a result, businesses have been incented to destock inventory in recent years, further suppressing growth.

Many dysfunctions in China's economy remain, but we believe it makes sense for the government to take a measured approach to addressing China's problems, rather than pursuing rapid change that would be destructive to both growth and confidence. We believe Chinese policymakers have done a decent job balancing growth and reform. There has been little slowdown in the pace of reforms, which should slowly benefit the economy in coming years.

Bears rattle off the numerous risks for China's economy, including the potential for a shadow banking crisis, excessive local government debt, industrial overcapacity and a property bubble. While we share these concerns, they are well known by investors and we believe the stock market has priced in a lot of future bad news. We believe the risk/reward is favorable for owning Chinese stocks within a market weight to emerging market (EM) stocks overall.

Read more international commentary, including our article 4 Mistakes to Avoid in International Investing at www.schwab.com/oninternational.

So what?

Any near-term correction would be healthy in the context of an ongoing secular bull market. Trying to time the market is always difficult, even though the market is in a potentially weak phase, both in terms of the annual and election cycles. And while sentiment is elevated in the United States, both Europe and China provide opportunities to invest where the mood is decidedly less enthusiastic.

© Charles Schwab