Key Points

- Stocks suffered some of their bigger daily and weekly declines of the year recently with geopolitical and Fed concerns the likely culprits. We don’t believe this was the start of a sustainable downtrend, although there could be further selling to come in the near-term.

- The U.S. economy appears to be strengthening, leaving us optimistic on the longer-term outlook for stocks. Likewise, worries over the Fed and the timing of the first rate hike have increased, but the initial stages of a tightening cycle tend to be positive for equities.

- We are downgrading our view on European equities due largely to economic softness and uncertainty surrounding Russian sanctions. But despite the recent rebound in China, we continue to be optimistic about its relative performance prospects; although we’d like to see an acceleration of financial and economic reforms.

The dog days of summer were jolted with a 300-plus point drop on the Dow during what was one of the worst trading weeks in two years. Thinner volumes due to summer-ending vacations can exacerbate market moves. But there has been a rise in volatility as the conflict in Russia threatens to expand and cause more economic damage, while investors adjust to the idea that the Fed may tighten sooner than what had been expected.

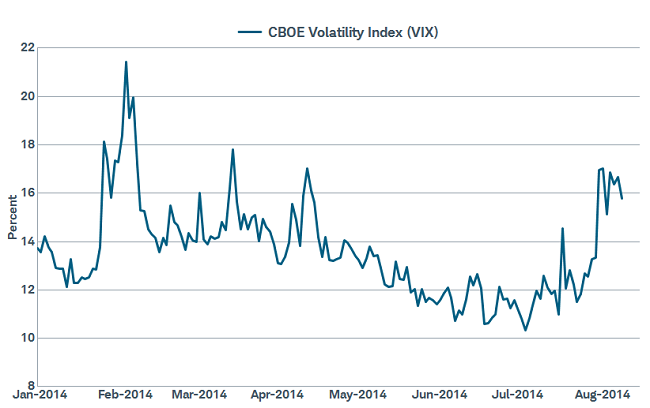

Volatility rises off very low levels

Source: FactSet, Chicago Board Options Exchange. As of Aug. 8, 2014.

The broader S&P 500 Index remains up for the year; however, we still haven’t had an official correction (+10% decline), and volatility has not come close to the highs we’ve seen during other times of uncertainty. Positively, investor sentiment (a contrarian indicator) has become more pessimistic. The Ned Davis Research Daily Trading Sentiment Composite recently dropped into extreme pessimistic territory, which is typically a good sign for stocks in the following months. Additionally, some of the more frothy areas of the market have been knocked down, including high yield fixed income and small cap stocks, while overall stock valuation metrics have improved. Second quarter earnings season is largely in the books and was much better than expected. Combine higher earnings (E) with lower prices (P) and the P/E ratio of the overall market has come down—potentially helping alleviate some valuation concerns.

Certainly there are risks in the market, and, as always, the possibility of more severe selling exists. Escalating tensions on the Ukraine border, the Israel/Gaza conflict, violence and military action in Iraq, economic concerns rising in Europe, and the possibility the Fed may move sooner than expected are all ingredients in the cocktail of risk. But the famous “wall of worry” may be building again, helping set the stage for the next move higher. As discussed below, the Russian situation seems to be the most concerning at this point, with sanctions hurting a Russian economy that was already struggling, but also potentially impacting some European companies in the near term. We are heartened that it is not in Russia’s best economic interest to take this too far, or to cut off energy supplies to Europe as that is where much of their income comes from. Unfortunately, as we’ve seen, logic doesn’t always prevail and we’re watching the situation closely.

The star of the show

As mentioned, despite these concerns, we believe the market remains in a longer-term bullish trend and we suggest using these pullbacks to add to positions as needed. Bull markets typically end when a recession is in the offing, which doesn’t appear to be the case currently. United States companies just completed a better-than-expected earnings reporting season, besting even some of the more optimistic predictions, while economic data continues to show improvement. The July Institute for Supply Management’s (ISM) Manufacturing Index rose to 57.1 from 55.3, indicating very solid strength; while the new orders component spiked to 63.4 and the employment reading jumped over five points to 58.2. Even more encouragement came from the ISM Non-Manufacturing Index, representing the service side of the economy, rising to 58.7, which is the highest reading since December 2005. Both the new orders and employment components showed solid rises in this survey as well.

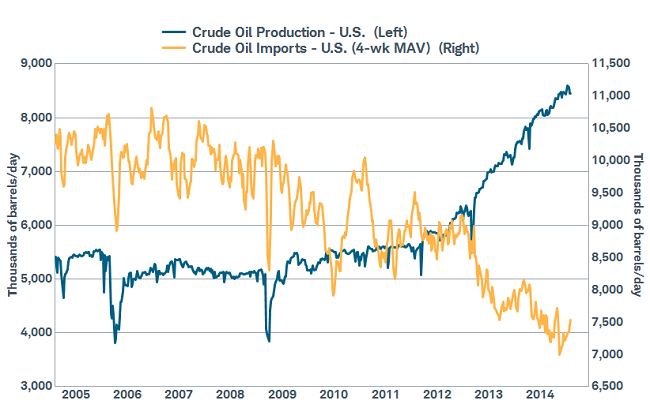

The labor market also continues to heal, with over 200,000 jobs being added for six straight months; and jobless claims continuing to move lower and dipping below the 300,000 mark on a four-week moving average basis that indicates a rapidly improving job market. Housing remains lackluster but affordability is still in a good range and a Fed survey showed banks’ willingness to lend for residential mortgages spiked to its highest reading since the early 1990’s (thanks to ISI Research for pointing this out). This leads us to believe that the housing market could get a bit of a rebound in the second half of the year, which should help consumer confidence. And lastly, the energy outlook in the United States is quite encouraging for future growth and US manufacturing competitiveness globally. Especially with the Russian and Iraqi uncertainty, it is particularly heartening to know that the United States is less dependent on foreign sources of energy than it has been in quite some time.

Energy supply/demand relationship in the United States continues to improve

Source: FactSet, U. S. Dept. of Energy. As of Aug. 8, 2014.

Departed, but not forgotten!

Politicians and policy makers may have left town for the summer break, but that doesn’t mean they’ve been forgotten. Despite continued assurance from Chairwoman Yellen that rate hikes are still a long way off, investors and some Fed members are starting to believe the moment of truth could come sooner. This uncertainty after a long period of exceptionally loose policy was bound to cause an increase in volatility, which could persist. Traditionally though, the beginning of rate hike cycles have been quite good for stocks as it has meant a solid economy and a still relatively easy Fed. It’s not until policy is perceived as tight that the market tends to suffer, and we still seem to be quite a ways from that.

We’re going to be in for an interesting couple of months after politicians return following Labor Day and gear up for the midterm elections in November. There is widespread support for fundamental tax reform—especially at the corporate level—and a reduced regulatory burden; but that’s unlikely for the remainder of the year. Large financial institutions have been noting more recently that the regulatory burden is getting quite onerous and impacting the level of risk they can take to the potential detriment of overall economy. In short, the campaign volume is likely to ratchet up in the coming weeks and months, but action of any sort seems quite unlikely.

European stocks: we’re downgrading

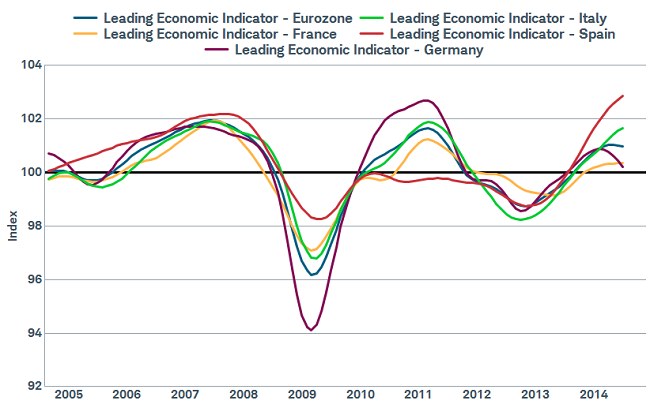

We’ve been positive on European stocks since the European Central Bank’s (ECB) head Mario Draghi’s “do whatever it takes” moment two years ago. Since then, leading economic indicators have generally risen—until recently. While the leading indicator of the euro zone as a whole has yet to decline, we are worried it could be pulled down by Germany, where a continued slowdown is indicated.

Indications euro zone economy slipping

Source: FactSet, OECD. As of Aug. 12, 2014.

Germany’s weakness is significant, because it is nearly 30% of the euro zone economy, and the weakness in German exports is of particular concern. German business confidence about future conditions in the Ifo Business Climate Index fell from 108.2 in February to 103.4 in July, which could restrain investment and hiring and further weaken economic activity. While a weak start to the year could be attributed to one-off reasons such as a harsh winter in the United States, geopolitical issues could create a lingering uncertainty.

Russia may matter more to Germany, and therefore the euro zone, than investors believe. While Russia represents only 3% of German exports, 47% of the firms surveyed in the July Ifo Business Climate Index said they have ties with Russia and 20% of those had already been negatively impacted by mid-July. Subsequently, the late-July sectoral sanctions could sustain an uncertain environment, because loopholes for Russia don’t yet create incentive for it to de-escalate. The Russia/Ukraine unrest could cut 0.1% to 0.2% from German gross domestic product (GDP) growth for several successive quarters according to BCA Research – meaningful given that second quarter GDP already dipped into contraction territory at -0.2%.

Positive offsets include a decline in the euro, which could boost competitiveness of exports. Additionally, the ECB’s quarterly bank lending survey in July showed the strongest demand for corporate loans in three years and banks reporting easing lending standards for the first time in seven years. However, given the downside risks to economic growth, demand for lending could slip again.

The ECB is likely to remain easy, but we believe it will wait to measure the effects of the quarterly Targeted Long-Term Refinancing Operations (TLTRO), which starts September 18, before making outright bond purchases, or quantitative easing (QE). Unless there was a significant downside threat to growth or inflation, we don’t believe the ECB would pursue QE in 2014, as near-term implementation is hampered by the small size of the asset-based securities (ABS) market, regulatory changes needed to increase ABS market liquidity, and the early stage of the design process. Elsewhere, September 18 is also the date for Scotland’s poll to consider splitting from the United Kingdom, but we believe a vote for full independence is a low probability.

We believe it is prudent to be cautious on European stocks for now. Despite the drop in stock prices, we believe it’s too soon to aggressively buy given lingering uncertainties and downward pressure on the euro zone economy and earnings estimates. Meanwhile, valuations are fair, but not cheap. Although European stocks could bounce on hopes of de-escalation in Ukraine, we prefer to wait for signs of an economic rebound before becoming constructive again.

Is China’s economy improving or not?

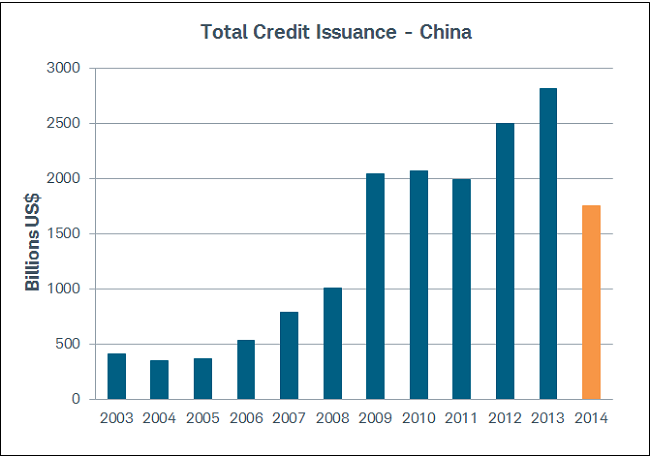

Behind the improvement in China’s GDP to 7.5% in the second quarter were some potentially unsustainable factors in our opinion; including a 40% month-over-month surge in total credit in June and a jump in central government fiscal spending, amid a property market slowdown that is still in the early stages.

Full year credit strong despite July’s drop

Source: Bloomberg. * Year-to-date data as of Jul. 31, 2014.

A sharp reversal in July has investors scratching their heads, as total credit fell a surprising 86% month-over-month to 273 billion yuan from 1.975 billion yuan, and non-bank channels subtracted from the money supply. Additional slowdowns were visible in industrial production at 9.0% in the month of July from 9.2% in June; retail sales of 12.2% in July versus 12.4% in June; and fixed asset investment of 17.0% for the first seven months, down from 17.3% through June.

Should investors be concerned? We would caution against extrapolating, as one month does not make a trend. Seasonal factors played a part, with deposits and loans typically rising in June then falling in July; and July was a reversal from two strong prior months, where on a three-month basis through July, total credit in 2014 rose 20% from 2013.

We believe China’s economy is on a long gradual path to slower growth as it transitions away from dependence on debt-fueled construction. There are likely to be bumps along the way as the government moves toward market-based mechanisms for driving the economy.

The specifics of reform implementation are still being worked out, illustrated by the credit system. The ballooning of the shadow banking system in recent years was an outgrowth of a system dominated by state-owned banks that lend primarily to state-owned enterprises. However, the unregulated and opaque nature of the shadow banking system created risks as well. By cracking down on shadow banking, the government may have forced lending to even more hidden means, reduced the layers of intermediation that could have inflated prior shadow lending figures, and made banks more risk adverse. Using more targeted forms of monetary stimulus—such as limited reserve requirement ratio (RRR) cuts, a new lending tool in the Pledged Supplementary Loan (PSL), and other means of trying to reduce financing costs in the real economy—will take time. Statements by the People’s Bank of China (PBoC) indicate that credit in August got off to a good start and that it expects stable credit growth in the future.

We believe there is more upside to Chinese stocks and that they will outperform the broad emerging market universe. After shunning Chinese stocks for over three years, there remain many bears and we believe an economic crash is unlikely. China’s economy is likely to benefit over the longer-term from reforms, although we would like to see more action on household registration (hukou) reforms, balancing local government budgets, and rural land rights.

Read more international commentary at www.schwab.com/oninternational.

So what?

Bouts of volatility are likely to persist as geopolitical concerns rise and fall; while focus on the Federal Reserve moves to when rates will rise. But improving economic data, decent valuations, and still-easy monetary policy make us believe the current U.S. bull market still has further to run. Conversely, we are downgrading our view on European equities modestly due to uncertainty surrounding Russian sanctions and some disappointing economic data. We remain optimistic on Chinese equities, although we want to see reforms continue, and after sharp recent gains a pause could be in the offing.

Important Disclosures

The Labor Report is a monthly report compiling a set of surveys in an attempt to monitor the labor market. The Employment Situation Report, released by the Bureau of Labor Statistics, by the U.S. Department of Labor, consists of:

- The unemployment rate - the number of unemployed workers expressed as a percentage of the labor force.

- Non-farm payroll employment - the number of employees working in U.S. business or government. This includes either full-time or part-time employees.

- Average workweek - the average number of hours per week worked in the non-farm sector.

- Average hourly earnings - the average basic hourly rate for major industries.

Initial Jobless Claims is a measure of the number of jobless claims filed by individuals seeking to receive state jobless benefits reported on a weekly basis.

China's Total Social Financing is an economic barometer that sums up total fundraising by Chinese non-state entities, including individuals and non-financial corporates.

Gross Domestic Product (GDP) is a quarterly report released by the U.S. Bureau of Economic Analysis that is an aggregate measure of total economic production for a country, representing the market value of all goods and services produced by the economy during the period measured, including personal consumption, government purchases, private inventories, paid-in construction costs and the foreign trade balance (exports are added, imports are subtracted).

The China Shanghai Stock Exchange (SSE) Property Index is a sub-set of the Composite Index that tracks the daily price performance of a group of property developer companies listed on the Shanghai Stock Exchange.

Ned Davis Research (NDR) Daily Trading Sentiment Composite® shows perspective on a composite sentiment indicator designed to highlight short- to intermediate-term swings in investor psychology.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Institute for Supply Management (ISM) Non-manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms by the Institute of Supply Management. The ISM Non-manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The S&P 500 Composite Index is a market capitalization-weighted index of 500 of the most widely-held U.S. companies in the industrial, transportation, utility, and financial sectors.

The Chicago Board of Exchange (CBOE) Volatility Index (VIX) is an index which provides a general indication on the expected level of implied volatility in the US market over the next 30 days.

Leading Economic Index (Indicators) is an index that is a composite average of leading indicators and is designed to signal peaks and troughs in the business cycle.

The Ifo Business Climate Survey is a monthly survey of economic conditions in Germany, and is based on the responses from approximately 7,000 firms in manufacturing, construction, wholesale and retail.

Indexes are unmanaged, do not incur fees or expenses and cannot be invested in directly.

Past performance is no guarantee of future results.

Investing in sectors may involve a greater degree of risk than investments with broader diversification.

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0814-5404)