Clear Sailingor Choppy Seas?

Key Points

- Upward momentum has paused and a pullback is overdue, but the longer-term trend is still likely higher.

- The Federal Reserve remains accommodative, but with QE ending and the first rate hike in the market's sights, volatility is likely to rise.

- Outside the United States, Europe is flirting with another recession and deflation, Japan is trying to pull itself out if its long-standing malaise, and Chinese growth is slowing. Emerging markets look attractive.

Risks are present: violence in the Middle East, Russian sanctions, weak Chinese growth, Europe’s struggles, U.S. midterm elections, and uncertainty around Fed policy

We have been in the "secular" bull market camp since 2009; but even the strongest secular bull markets have experienced corrections. However, a more protracted bear market or even severe correction is not likely in the cards given very low risk of a recession coming in the near-to-medium term.

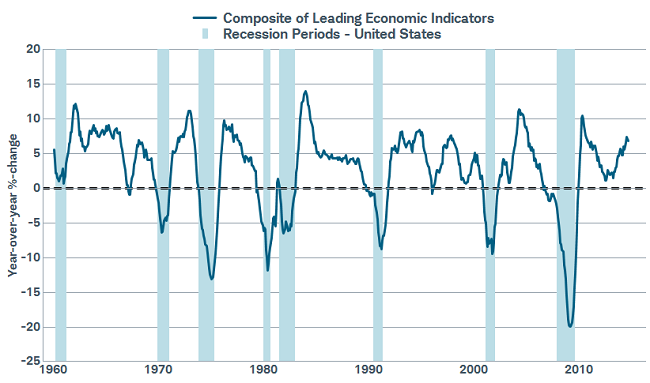

Recession doesn’t appear to be imminent

Source: FactSet, U.S. Conference Board. As of Sep. 22, 2014.

A correction, however, is possible. Geopolitical tensions, some measures of stretched sentiment, weakening market breadth, Fed tightening on the horizon, and midterm election risk could represent catalysts. But we echo the sentiment of Peter Lynch, manager of the Fidelity Magellan Fund during its heyday, when he said, "Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves" (BusinessWeek, September 2014). A Schwab study using Standard and Poor’s data shows that between 1994-2013, missing the top ten up days by trying to time the market would have resulted in a reduction from a 9.2% annualized return to 5.5%. We remain bullish longer term and suggest that clients who remain under-exposed to equities use dollar-cost averaging to add to equity allocations.

Economic Goldilocks?

Our optimism stems largely from the current economic landscape of trend growth and low inflation, typically a healthy backdrop for equities. Helping to keep inflation low has been falling commodity prices courtesy of weak global growth and a strengthening US dollar. (read more on the dollar in Liz Ann's article "Million Dollar Question: Is the Dollar's Strength Bullish?")

Falling commodity prices fuel tame inflation, bolster consumer

Source: FactSet, Commodity Research Bureau. As of Sep. 22, 2014.

Lower commodity prices, especially on the energy front, is a powerful support for the consumer-centric U.S. economy. Retail sales rose 0.6% in August, while ex-autos and gas, they were up 0.5%, while previous months were revised higher. Additionally, consumer confidence continues to improve, with the Conference Board’s index jumping to 92.4 in August, the highest reading since October 2007. And in spite of a weaker August employment report (likely to be revised higher), most leading indicators of the job market have improved markedly—notably continuing jobless claims, which are at their lowest level since 2007.

The housing recovery remains uneven. The National Association of Homebuilders’ (NAHB) Survey rose to its highest level since 2005, indicating increasing optimism, and linked to the improvement in the labor market. Unfortunately, the positive momentum was partly offset by weak housing starts and building permits in August; following robust readings in July. Increased confidence, loosening lending standards, and a tight rental market in many areas of the country, could foster an improving housing market, which could further bolster the consumer.

U.S. corporations have been carrying much of the economic load and third quarter earnings season is upon us. A factor on which to keep an eye is whether the larger multi-national companies are yet feeling the brunt of the stronger U.S. dollar. Fortunately, capital spending plans are improving according to both the National Association of Independent Business (NFIB) and the Institute for Supply Management (ISM); while notable strength remains among the regional PMI indices; supporting our theme of a US manufacturing and energy renaissance.

Yellen gets her way

Despite clearly improving economic data and helped by still-low inflation, the Federal Reserve opted to leave in "considerable time" language in its statement, but Yellen went to great pains during her recent press conference to reiterate that this should not be considered calendar-based guidance and that the Fed will make decisions based on the economic data (read more at "Fed Keeps “Considerable Time” … But Ups Rate Expectations Through 2017").

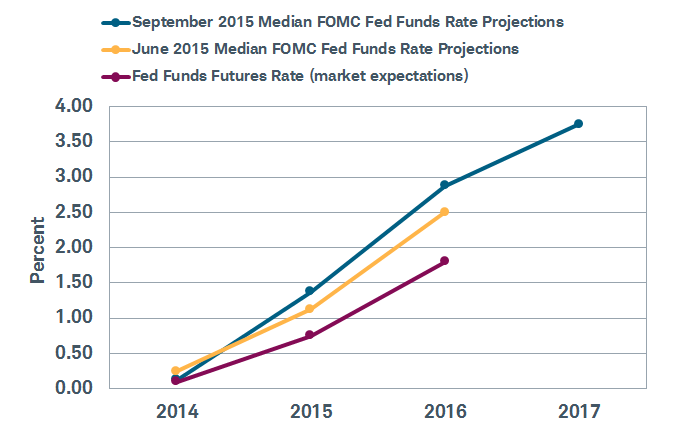

A recent report by the San Francisco Fed highlighted that the market seems to be underestimating the timing and pace of rate hikes, which could cause some additional volatility. You can see below the difference between the market’s expectations and the Fed’s now-upped expectations for the path of the fed funds rate.

Market expectations for the Fed are mismatched

Source: Federal Reserve, FactSet. As of Sept. 22, 2014.

It’s tough to set expectations exactly right when you’re dependent on unknown data, but we do believe rate hikes will commence in the first half of 2015, after quantitative easing ends in October. One note, stocks, and particularly cyclically-oriented sectors, tend to do quite well in the six months leading up to the start of a rate hike cycle (see Schwab Sector Views for more).

Moving on to D.C., Congress is back in session; but don’t blink or you’ll miss it, as they again vacate the premises to campaign for the upcoming midterm elections. The fight is likely to be bruising, and some additional market volatility could occur, as is typically the case in advance of midterm elections.

The Global Picture

If your head is spinning, it’s not your fault. The world’s major economies have taken different paths and are headed in different directions as the third quarter comes to a close.

- The United States’ leadership has been reinforced by the sluggishness in most other major economies that is helping keep inflation, oil prices, and interest rates low.

- China’s solid start to the quarter deteriorated quickly. The most dramatic example was the 6.9% growth in industrial production in August, the worst reading since the financial crisis of five years ago.

- Japan’s economy suffered from the aftermath of the April tax hike. However, the economy showed some improvement during the quarter as the impact of the tax hikes began to fade and the aggressive economic stimulus supplied by the Bank of Japan was increasingly felt.

- Europe remains stuck in a negative spiral on the brink of the third recession in six years and is dangerously close to deflation with the year-over-year pace of inflation coming in at just 0.4% in August.

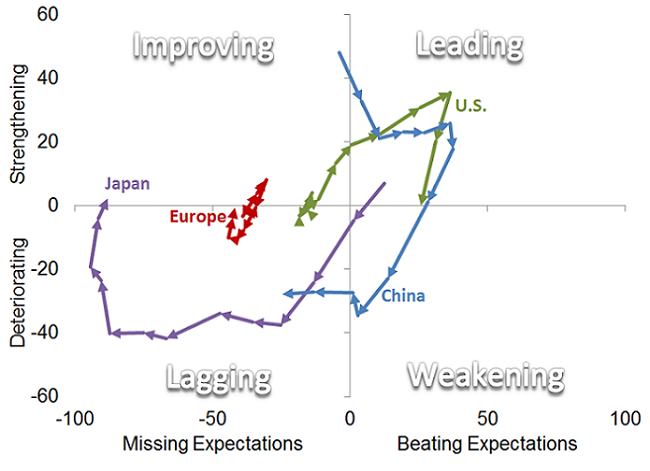

Markets tend to respond to how actual data compare to expectations, rather than whether that data is strong or weak in an absolute sense. For example, even a weak data point may inspire a lift to stocks if it was better than generally expected. The chart below depicts how actual data has been faring relative to expectations over the past three months and in what direction the data is trending relative to those expectations for the world’s major economies.

Major economies on different paths

Source: Charles Schwab, Bloomberg data

* 13 week paths of Citigroup Economic Surprise Indexes by Country/Region plotted by three week moving average (horizontal axis) and three week change in moving average (vertical axis)

So what do the data and expectations say now about where these economies are headed and what it means to stock market performance?

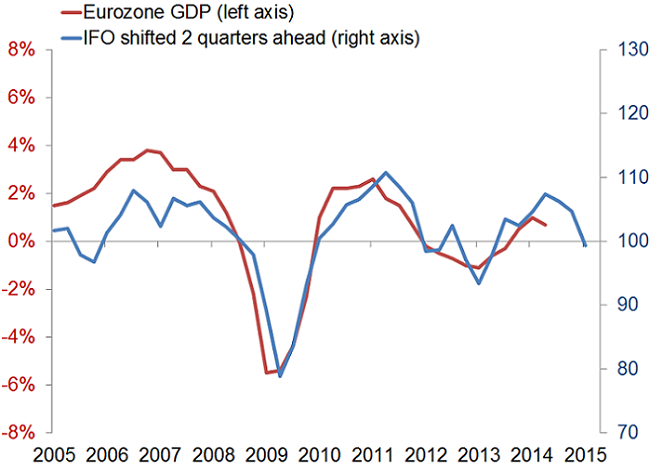

Unfortunately for Europe, leading indicators like the IFO and ZEW business surveys continue to point to further economic weakness not yet reflected in expectations. The expectations components of these surveys are some of the most reliable forward-looking indicators for Eurozone economic growth. The IFO and ZEW both slid in September despite the surprise stimulus announcement by the European Central Bank. The IFO tends to lead the year-over-year change in GDP by two quarters and is pointing to a stall in GDP growth in the quarters ahead relative to the Bloomberg-tracked consensus of economists’ estimates that expect growth to accelerate. The potential for more disappointing data may continue to weigh on European stocks after a third quarter loss of about 5% through September 23 on the Euro STOXX 50 Index.

Leading indicators point to further weakness in Europe

Source: Charles Schwab, Bloomberg data

* IFO Germany Business Expectations Survey (right axis) and Year-over-Year Eurozone GDP (left axis)

Japan’s economy has been showing signs of improvement relative to expectations, lifting the Nikkei Stock Average by 5% in yen terms during the month through September 23. But the efforts to drive down the value of the yen in order to aid export growth has left the stock market flat measured in U.S. dollars. The economic data may continue to improve given the fading impact from the tax hike, while increasing political support for corporate tax cuts, a further push by the government pension fund into stocks, and an ongoing slide in the value of the yen may combine with aggressive bond buying from the Bank of Japan to create the most stock market favorable policy mix of any major nation.

China’s weak economic data for August sparked an emerging market stock sell off. However, the first of the September data points, the preliminary HSBC Purchasing Managers Index rose from the August reading and came in better than expected. Also, the leading sub-indexes for new orders and new export orders rose, suggesting the rebound may be durable. Rather than further deterioration this may be a sign that the weaker economic data points may begin to stabilize and join the stronger data seen in employment and exports. This would be welcome news for Chinese and Emerging Market stocks.

Read more international commentary at www.schwab.com/oninternational.

So what?

We are at a tenuous point in the market seasonally speaking and a pullback is quite possible. We don’t recommend trying to time a potential correction, however, as that is virtually impossible and exposes investors to missed upside opportunities waiting on the sidelines. Elsewhere, the international picture looks a little shaky, but diversification is important and we do favor emerging markets within an international portfolio.

© Charles Schwab