Plot Twistor a Different Book?

Key Points

- Volatility skyrocketed and the long-awaited correction arrived, mostly. Although painful, corrections are normal and can be healthy.

- The Federal Reserve took pains to reassure investors of their commitment to policy accommodation. The Ebola scare should be short-lived and we are entering a period traditionally quite good for stocks.

- History shows that recent volatility is not unique and has not necessarily been something to fear in the past.

The stock market finally reached the tipping point, with major averages flirting with correction territory (10% loss or more), at least on an intraday basis. Fears of a renewed European recession morphed into concerns over the U.S. economic outlook. Fears over Ebola also added to the flight away from risky assets and into the perceived safety of U.S. Treasuries, as the 10-year yield briefly dropped below 2%.

Yet stocks quickly bounced and we believe the bull market is intact and investors who remain underexposed to equities relative to their plan should use further pullbacks to gradually add exposure. The time to buy has proven throughout history to be when investors most want to sell.

Corrections are normal in bull markets and we had gone without one for an extended period. Our belief that a more significant pullback was likely was highlighted in early September when we were seeing elevated optimism and/or complacency (and the extreme lack of bearishness); weak market breadth; and monetary policy uncertainty. In addition, we were entering the historically weak September/October period, especially in midterm election years. The market had also been wearing a Teflon coating as per geopolitical turmoil, which was unlikely to persist. Given the correction and heightened volatility that's ensued, Ned Davis Research reports that their Crowd Sentiment Poll has fallen to a level now indicating extreme pessimism—which typically bodes well for stocks in the coming months. And further on midterm election tendencies, every midterm election year going back to 1950 has featured a sizable pullback, followed by solid performance over the ensuing 12 months, according to Strategas Research Group. So what investors have to do is ask: has the story fundamentally changed as much as the volatility might suggest?

Same story…with a twist

To us, the secular bull market case hasn't changed; we're just in a mature phase. The U.S. economy continues to grow, the Federal Reserve remains accommodative, and global growth isn't falling off a cliff.

Recent U.S. economic news has been mixed. The Empire Manufacturing Index fell, but remains in the expansion zone; while retail sales fell 0.3% in September and ex-autos and gas dropped 0.1%.

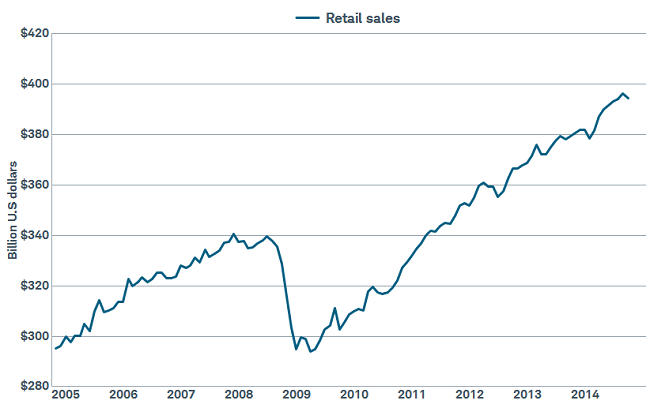

Blip in the consumer or something more?

Source: FactSet, US Census Bureau. As of Oct. 20, 2014.

The consumer is one area worth watching. If Ebola reports continue to come out, or events like in Canada, further spread fear, behavior could be impacted. But the significant decline in oil prices acts as a powerful "tax cut" for consumers. Also, according to ISI Research, retail sales have an 87% correlation with the performance of the S&P 500—so market action could continue to be a consumption-driver.

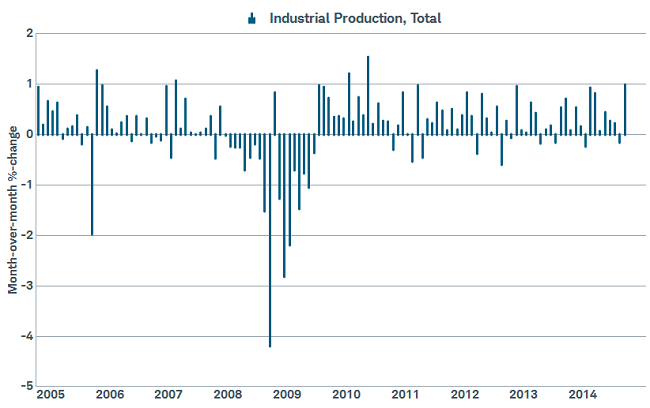

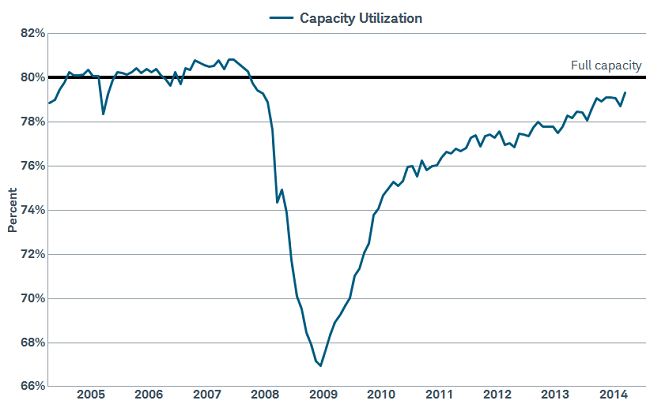

Other evidence suggests the U.S. economic expansion continues. Jobless claims, a leading indicator, recently hit their lowest level since 2000, while the Philadelphia Fed Index offset the Empire reading by posting a robust 20.7 reading. Additionally, industrial production posted a surprising 1.0% gain, while capacity utilization moved up to 79.3, close to the 80 level generally recognized as representing full capacity; and a level at which capital spending tends to be very robust.

Business confidence seems intact

Source: FactSet, Federal Reserve. As of Oct. 20, 2014.

Capacity may be close to full

Source: FactSet, Federal Reserve. As of Oct. 20, 2014.

Fed remains concerned

Declining inflation expectations, slow wage growth, and deflation fears in Europe could keep the Federal Reserve from considering an earlier first interest rate hike; while one voting member even suggested a fourth round of quantitative easing (QE4). We don't believe anything so drastic would be necessary, or beneficial, but it does help bolster the "don't fight the Fed" case for stocks.

The upcoming U.S. midterm election could add to some near-term volatility, but as pointed out, stocks have traditionally done quite well in the year following midterm elections, regardless of which side "wins." We've been asked quite a bit recently about the implications of a possible Republican take-over of the Senate; and we do believe corporate tax reform would likely move to the top of the priority list, which would be stock-market friendly.

Echoes of the Past

Many of the world's major stock markets experienced a 10-20% decline in recent weeks. The past five years have featured recurring themes that are again fostering a volatile investment environment. After a bit of a respite in 2013, these echoes of the past have been repeated in 2014 with a familiar combination:

- the Fed ending a stimulus program (QE3),

- uncertainty over the U.S. midterm elections,

- Eurozone and Japanese economic weakness,

- slowing growth in China, and

- geopolitical flare ups from the Middle-East to the Far East (Hong Kong).

Looking back, we can see just how similar the drivers of the 10-20% stock market declines in the world's major markets are to those of the past five years.

Major Market Moves and the Drivers

|

Event |

2010 |

2011 |

2012 |

2013 |

2014 |

|

10-20% stock market pullback in Europe (STOXX 600) |

X |

X |

X |

X |

X |

|

10-20% stock market pullback in Japan (NIKKEI 225) |

X |

X |

X |

X |

X |

|

10-20% stock market pullback in United States (S&P 500) |

X |

X |

X |

||

|

Fed ending stimulus program |

X |

X |

X |

|

X |

|

Washington-driven uncertainty |

X |

X |

X |

X |

X |

|

Europe recession/crisis |

X |

X |

X |

|

X |

|

Japan economic shock |

X |

|

X |

||

|

China slowdown |

X |

X |

X |

|

X |

|

Geopolitical risk flare up |

X |

X |

X |

X |

X |

Source: Charles Schwab, Bloomberg data as of 10/22/2014.

In 2010, the drivers that helped fuel the 10-20% declines included:

- The end of the Fed's QE1 stimulus program along with central bank rate hikes (Australia, Sweden, Norway and Brazil).

- Uncertainty in the United States around the impact of the Dodd-Frank legislation and the end of the homebuyer tax credit.

- Eurozone debt problems worsened and Greece needed a bailout.

- Japan's fourth Prime Minister in three years resigned as economic growth slowed and China's economy slowed from a first quarter growth rate of 11.9% to below 10% by the fourth quarter.

- The 2009 nuclear tests and sinking of a South Korean naval vessel by North Korea.

In 2011, drivers that helped fuel the 10-20% declines included:

- The end of the Fed's QE2 stimulus program along with central bank rate hikes (Eurozone, China, Philippines).

- The U.S. budget debacle and related downgrade of U.S. Treasuries.

- Eurozone debt problems worsened and Portugal needed a bailout.

- Japan suffered an earthquake and nuclear disaster that disrupted global supply chains and pulled Japan into a recession. China's economic growth slowed from 10.4% in 2010 to 9.3% in 2011.

- The "Arab Spring" uprisings in Northern Africa erupted, toppling governments and pushing up oil prices.

In 2012, drivers that helped fuel the 10-20% declines included:

- The coming end of the Fed's "Operation Twist" stimulus program pressured the markets before the Fed ended up extending it just before it was due to expire. Also, some central banks hiked rates (Poland, Denmark, Russia, Columbia).

- The U.S. presidential election led to some policy uncertainty along with the anticipation of the "fiscal cliff" at year-end.

- The Eurozone entered a recession and the region's debt problems came to a head as peripheral European bond yields soared requiring European Central Bank (ECB) intervention.

- Japan's economy contracted in the second half of the year and China's economic growth slowed from 9.3% in 2011 to 7.7% in 2012.

- The Syrian civil war escalated.

In 2013, markets in Europe and Japan experienced a 10-20% decline, but in the United States stocks suffered a smaller pullback perhaps because there were fewer of these recurring themes. However, 2013 was the exception, not the norm. And those themes are back in 2014, as is market volatility. These recurring stock market declines may have been easy to forget since they were reversed fairly quickly and, with the exception of 2011, the indexes all posted gains for each of the calendar years despite the intra-year 10-20% declines. As we look out to the remainder of the year and to 2015, the volatility is likely to continue—but so may the longer-term trend of gains despite the shorter-term ups and downs.

Read more international commentary at www.schwab.com/oninternational.

So what?

Volatility could continue but equity investors should keep the longer-term picture in mind, which we believe is positive. The U.S. economy is improving and monetary policy remains quite loose. The international picture is more concerning but diversification is important across asset classes. We currently favor emerging markets within a diversified international portfolio.

© Charles Schwab