Key Points

- Stocks have recovered the losses seen recently and seem to be lining up for another sustained move higher, although investor complacency could be a risk.

- Quantitative easing is now in the past, at least in the United States, but the Fed remains quite accommodative. Midterm elections are over, and the winner historically has been investors.

- A decline in oil is not universally positive, but the reasons are likely more a function of increased supply and the strength in the US dollar; and less a function of weaker demand.

Midterm elections are over and we get a reprieve from negative political ads for the time being. According to Strategas Research Partners, since 1962, stock market performance following a correction during a midterm year, such as we just experienced, has been quite good. Subsequent 12-month returns have ranged from 12% on the low end to 58% on the high end, with the average coming in at just over 32%.

History doesn’t always repeat itself, but it can be a guide to the future. Although tailwinds are ample, there are some headwinds; including tighter Fed policy, inflation/deflation risks, eurozone economic woes, weak wage growth, and the aforementioned investor complacency.

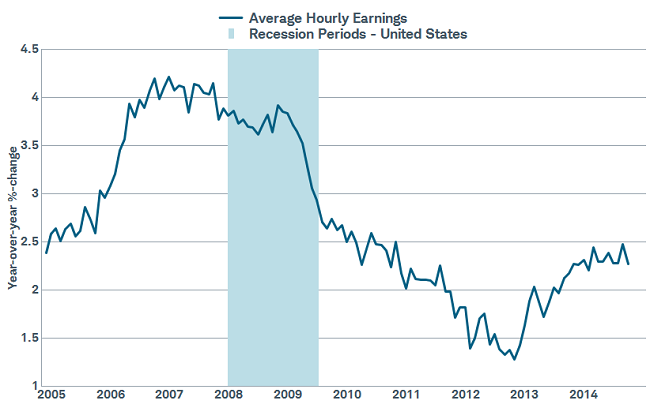

Fundamental support for US stocks continues to look solid in our view. Employment is improving, with the Department of Labor reporting another 214,000 jobs were added in October, while the unemployment rate fell to 5.8%. We believe we are getting to the point where wages should begin to accelerate a bit, which has been a largely missing ingredient from the current recovery.

Earnings are improving…slowly

Source: FactSet, U.S. Dept. of Labor. As of Nov. 3, 2014.

The recent US gross domestic product (GDP) report eased some fears of a foreign-led US slowdown as annualized real growth came in above expectations at 3.5% for the third quarter. Also encouraging and supporting our capex theme, fixed business investment rose 5.5% and spending on equipment and software was up a solid 7.2%. Capex has now grown at a faster pace than GDP growth for five consecutive quarters.

The manufacturing renaissance remains in force as the Institute for Supply Management’s (ISM) Manufacturing Index rose to a surprisingly strong 59.0 in October from 56.6, while the new orders component surged to 65.8 from 60.0. The service side also showed continued strength as the ISM Non-Manufacturing Index posted a 57.1 reading, down from 58.6 but still quite solid.

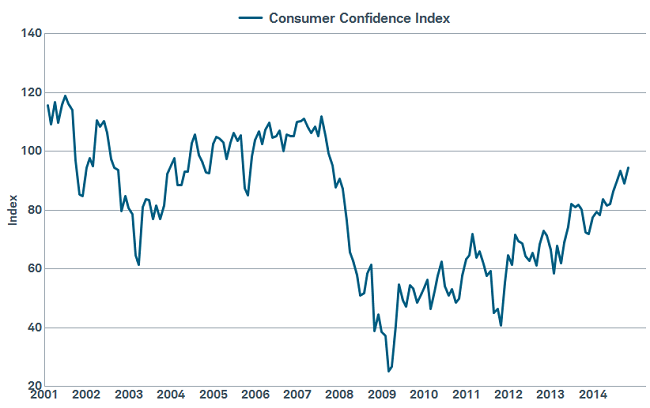

Also, third quarter earnings season and forward-looking outlooks have been surprisingly good, which helped the market recover October’s losses. US GDP is still consumer-dominated, and there are hopeful signs for the holiday shopping season and beyond. Oil and gasoline prices have fallen, and although according to ISI Research there isn’t much correlation historically between consumer spending and oil prices, this time could be different as discussed below. Additionally, consumer confidence according to the Conference Board reached its highest level since before the great recession at 94.5, up from an average of 73.2 in 2013 and 67.1 in 2012.

Consumer confidence is rising

Source: FactSet, Conference Board. As of Nov. 3, 2014.

Done!

As mentioned, the midterm elections are now complete, which in the past has been a victory for investors in and of itself. From a near-term policy perspective, there are signs that corporate tax reform could rise to the top of the priority list, which would support US competitiveness globally. Regulatory reform would likely be a market-positive as well.

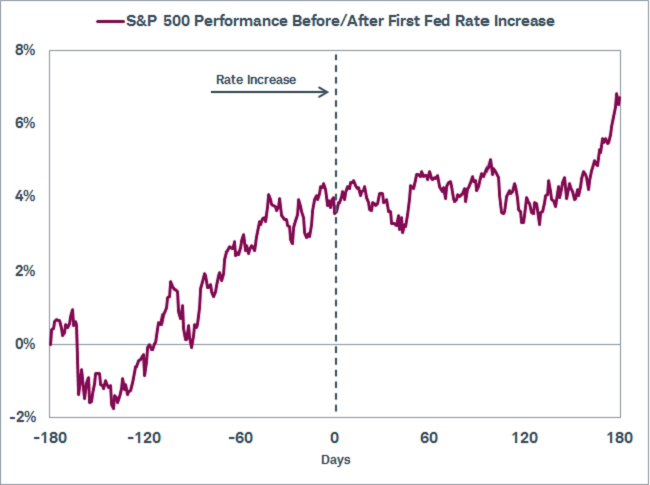

The other finale of note was the end of quantitative easing (QE) The Fed will continue to reinvest the proceeds of maturing securities on its balance sheet—while rate hikes are not imminent—so the market is not yet faced with much tighter monetary policy. With QE over, attention will now shift to when the first interest rate hike will occur. Investors should take the Fed to its word about the timing being data- not calendar-dependent. On that note, the Fed did upgrade its view of employment conditions, and noted it believes the recent dip in inflation is only a temporary phenomenon. The stock market has traditionally been a bit volatile but positive in the months leading up to the first rate hike.

Stocks have done well leading to a rate hike

Based on fed tightening cycles since 1962. Discount rate used prior to 1984. Fed Funds rate used since 1984. Source: Birinyi Associates, Inc.

Gaining from oil’s decline

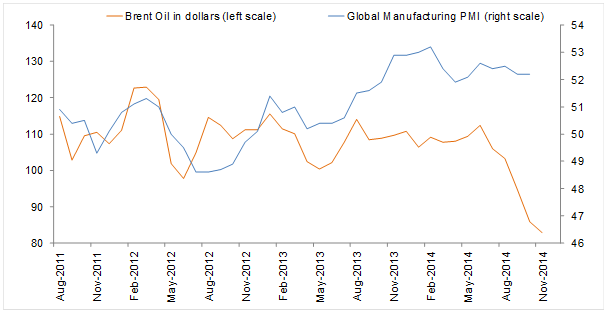

As mentioned, oil prices have plunged over the past five months. What has driven the decline is critical to assessing what it means for the global economy and markets. Fortunately, it doesn’t appear that weak global demand is the main culprit behind the drop in oil prices, although it’s been a factor World oil demand hit an all-time high in June of this year and although it has experienced a seasonal dip in demand since then, the latest world oil demand data from the U.S. Department of Energy shows demand is in line with the year ago level when Brent oil was around $110. In fact, the Global Purchasing Managers Index (PMI), a timely and reliable measure of worldwide economic activity, shows that while oil and economic activity usually go hand in hand, the recent drop is unlikely to be a sign that the global economy is hitting a wall.

Don't Blame Demand for Oil's Drop

Source: Charles Schwab & Co. Inc., Bloomberg data as of 11/4/2014

Instead, the rapid price drop in oil is likely to act as a boost to economic growth. With the amount spent on oil amounting to 4% of world GDP, the global price decline from around $110 in recent years to $80 is about a 27% decline, or more than 1% of world GDP. While this doesn’t translate directly into a 1% boost to global growth, since the windfall to consumers is a cost to producers, in the short term it can have a sizable effect. Producers are unlikely to make major cuts to their expenditures in the short-term, while consumers have consistently proven to spend most of what they save at the pump.

The potential boost to global growth from lower oil prices is a needed shot in the arm for global economies that have been accustomed to central bank stimulus to boost growth, especially Europe and Japan. From a country perspective, major energy exporting nations such as Kuwait, Saudi Arabia, Qatar, Iraq, Russia and Venezuela have the most to lose, while net energy consumers—accounting for most developed and emerging market countries—have the most to gain from oil’s fall.

So what?

The pullback seen in October is now just a memory and stock indexes are again pushing into record territory. Seasonality and the election cycle are lining up with still solid earnings growth and an expanding economy to help support further gains. Complacency is a risk but we continue to believe the trend in US stocks is higher.

© Charles Schwab