Key Points

-

Stocks are again near record highs after a dismal January, echoing 2014. But while we remain secular bulls, the risks to a correction and increased volatility appear elevated.

-

The Federal Reserve remains data dependent and is debating dropping the “patient” language that would signal a rate hike could come at any time. More importantly, we believe any rate hike “campaign” will be gradual and could end at a lower level than most are imagining at the present time.

-

Europe’s economy appears to be stabilizing but further market gains may be tough to come by. Meanwhile, Greece bought some time, but a sustainable resolution remains elusive.

“History does not repeat itself but it does rhyme,” Mark Twain.

One of our favorite quotes as it so often seems to apply to the stock market. Indeed, 2015’s initial stages are resembling those of last year, with a dismal January being followed by a march higher to new records for major indices. Other “rhyming” is happening as Europe is dealing with a debt crisis, Japan is pursuing easy monetary policy, and there is geopolitical unrest in Russia. But we don’t believe the playbook is the same this time around, and the ride could be a bit bumpy as we go throughout the year.

The rebound in stocks after January’s selling has pushed investor sentiment back to levels associated with excess optimism according to the Ned Davis Research Crowd Sentiment Poll; but not extremely so at this point in time, meaning we could certainly have some more upside in the near term. But we are more cautious in the intermediate term as the period leading up to an initial rate hike has been characterized by increased volatility. Therefore, we are advising tactical investors to have a more neutral sector stance, while all investors should make sure they are well diversified, taking profits from positions that may have had good runs resulting in outsized allocations.

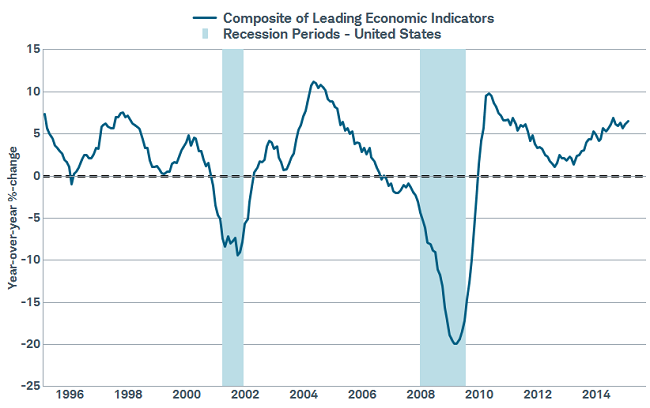

Economy still good—but not without challenges

The US economy is still showing decent growth, with The Conference Board’s Leading Economic Index rising again in January; although the Board did note concern over a “weak outlook for new orders in manufacturing.”

Economy looking solid

Source: FactSet, U.S. Dept. of Labor, Standard & Poor's. As of Feb. 20, 2015.

We also saw some weaker-than-expected regional manufacturing surveys in the form of the Empire Manufacturing State Index and the Philadelphia Federal Index—although both continued to show expansion. Additionally, industrial production rose by 0.2% in January, although capacity utilization was slightly disappointing, remaining just below the key 80.0 level at 79.4. This suggests a slight downshift in manufacturing activity, but still decent growth.

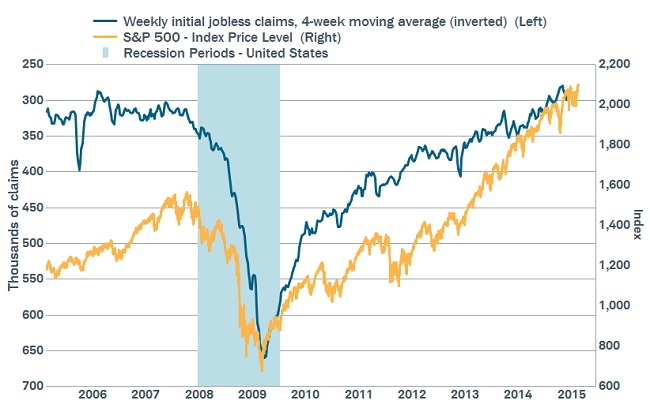

But we believe the consumer is poised to take over leadership within the US economy. The job market is strengthening, with jobless claims, a leading indicator, remaining well below the key 300,000 level on a four-week moving average basis.

Claims continuing to indicate strength

Source: FactSet, U.S. Dept. of Labor, Standard & Poor's. As of Feb. 20, 2015.

We are also starting to see glimmers of upward pressure on wages. After a 2.3% year-over-year increase in the fourth quarter Employment Cost Index (ECI), we also saw the National Association of Business Economics (NABE) Survey report growing expectations for rising wages and salaries, with 51% of respondents expecting increases for the first three months of 2015. Additionally, Walmart, the world’s largest retailer with over two million employees, announced it was raising wages for its lower-wage workers. And the fall in energy prices has put more money in consumers’ pockets, which we believe will eventually filter through to higher consumer spending.

Port problems

One fly in the ointment is the recently resolved labor dispute at West Coast ports, which has resulted in dozens of ships facing long delays in getting goods offloaded. According to Reuters, the affected ports handle roughly half of all US maritime trade and more than 70% of imports from Asia (Reuters, February 18, 2015). The dispute dragged on for months and it was beginning to impact the US economy. Retailers are warning of lower inventories and potential higher costs due to more costly alternative shipping options. We don’t believe this issue will have a major lasting impact on the US economy, but it could dent first quarter gross domestic product (GDP) growth.

A mixed bag for the Fed

The effect of the port dispute is one more thing for the Fed to consider as it moves closer to raising interest rates. There seems to be a growing contingent within the Fed that would favor removing the “patient” language from its statement, theoretically freeing it up to raise interest rates as it sees fit. But what is unique at this stage is that potentially tighter monetary policy is not in reaction to higher inflation. In fact, with oil much lower and a stronger dollar, the near-term threat of inflation seems to be lessening. However, employment is the Fed’s other mandate and most associated metrics are indeed signally the Fed should move. In addition, the Fed would like to “normalize” monetary policy after the emergency measures taken during the great recession.

We think investors should focus less on the timing of the first rate hike and more on the likely path of additional rate hikes. At this point, we believe it will be a very gradual process, giving the economy time to react. It appears the stopping point of any rate hike series will be lower than seen historically, as deflationary impulses across the globe seem to be relatively entrenched.

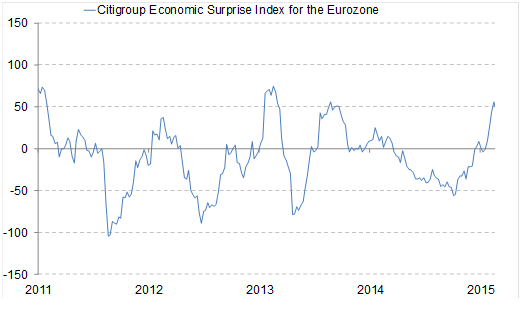

Europe Surprises

Much like the first two months of 2014, European stocks have outperformed U.S. stocks by about 3 percentage points, measured by the STOXX Europe 600 and the S&P 500 indexes. Economic data in the Eurozone has been surprising economists’ estimates and lifting the Citigroup Economic Surprise Index. This index rises as data exceeds economists’ expectations and falls when it misses those expectations. The surprise index for Europe is back to the highs of around 50 seen several times in recent years. That has helped to lift European stocks this year, even in dollar terms. However, if the index is once again peaking at the current level Europe’s stock market rally may be due for a pause.

Europe’s string of surprisingly solid economic data may be ending

Source: Bloomberg data as of 1/23/2015.

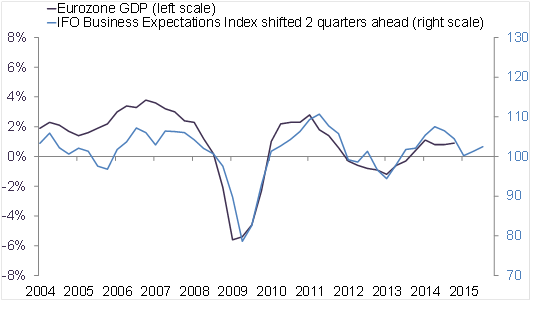

Eurozone GDP for the fourth quarter of last year came in at +0.9% year-over-year after +0.8% in the third quarter. While the pace of economic expansion was unevenly distributed among Europe’s economies, the overall picture is one of stabilization.

Looking ahead, leading indicators of growth in Europe have been pointing to further stabilization of economic growth. As you can see in the chart below, the widely-watched IFO survey of business expectations in the Eurozone has rebounded. The IFO Business Expectations index aligns with annualized economic growth of around 1% in coming quarters as the European Central Bank (ECB) gets set to engage in the program of bond purchases announced on January 22; and the easing of geopolitical risk if the Ukraine ceasefire and Greece bailout deals hold up.

Forward looking indicator pointing to stabilization of growth in Europe

Source: Bloomberg data as of 2/24/2015.

Since the January ECB meeting, inflation expectations and the euro exchange rate have remained relatively unchanged against the U.S. dollar. The STOXX Europe 600 index rose by 6% since the announcement of the bond buying program on January 22. We expect more details to emerge at the March 5 ECB meeting as to how the Eurozone’s 19 different central banks will conduct those purchases. While these details may not have much overall market impact, the ECB will also release its updated projections for growth and inflation which may provide insight into how the ECB may respond to incoming economic data as it compares to its outlook. It is likely the ECB will again downwardly revise its outlook for the 2015 inflation rate, which continues to fall; but also an inflation forecast for 2017 that shows an expectation for inflation to be back near the ECB’s target of 2%. If inflation fails to track toward its forecasts, an extended or more aggressive bond buying program could emerge.

Greece gets a deal

After months of uncertainty, we may get months more. The temporary deal agreed to this week extends Greece’s current bailout program for just four months. This means Greece gets the funding it needs for a while longer. But the deal requires reforms proposed by Greece to be detailed by the end of April (this week’s proposal included principles rather than numbers) and agreed upon by the European Union (EU), the International Monetary Fund (IMF), and the ECB. Greece’s new government was elected in part to oppose these types of reforms and unwind those that had previously been put in place. If the Greek government cannot agree to these reforms by the end of April, it may bring renewed conflict with Greece’s creditors.

So what?

Stocks have recovered their January losses and have continued to move higher. While economic growth remains solid and we remain secular bulls, investors should be prepared for increased volatility and the potential for a near-term correction. Also, European stocks may be due for at least a pause and we suggest looking to add exposure to emerging market positions if needed. Staying well diversified and keeping an eye on rebalancing is the recommended strategy.

(c) Charles Schwab