Will Dipping Data Lead To Dramatic Drop?

Key Points

-

US stocks have been relatively resilient in the face of some disappointing economic data. We believe the longer-term bull market remains intact but the risks of a near-term correction seem elevated to us.

-

Despite the softer data, the Federal Reserve seems on track to raise rates at some point this year. Regardless of the starting point, we think they’ll be cautious and slow in raising rates as long as inflation remains subdued.

-

The European Central Bank (ECB) started its version of quantitative easing (QE) although inflation expectations may be too optimistic. But weakening currencies in countries such as China and Japan, as well as the Eurozone, appears to be helping their economies.

Stocks are trading just below all-time highs despite some large down days recently and some weaker economic signals, and we believe the “secular” bull market is intact. Much of the weaker data recently appears tied to severe weather in the east, the port shutdown in the west, and sharply lower energy prices that have caused some dislocations in the manufacturing sector. These shorter-term factors are also behind the sharp reduction in corporate earnings estimates, which actually may help to support stocks due to lowered expectations. For details, see Liz Ann’s article Trampled Under Foot: Earnings Estimates Crushed, But Not Stocks. But the weakness in some economic indicators and earnings is not likely due to heightened recession risk given still-strong leading indicators.

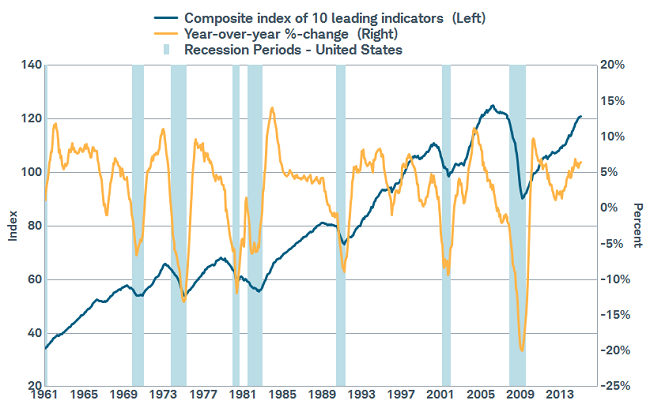

LEI not indicating a recession

Source: FactSet, U.S. Conference Board. As of Mar. 9, 2015.

That doesn’t mean that the all-clear signal has been given for stocks, highlighted by the recent pick-up in volatility. There are some signs that an elusive correction could occur this year, although trying to time such an event is not recommended; while it would likely represent a buying opportunity within a longer-term bull market. Valuations, which aren’t a great market timing tool, are above long-term median levels; but not yet at historic extremes. A better short-term indicator is often investor sentiment, which is showing fairly elevated optimism at this point—notably by individual investors and investment newsletter writers. However, recent volatility is beginning to temper some of that enthusiasm, which would be welcomed.

Softer data—temporary in nature?

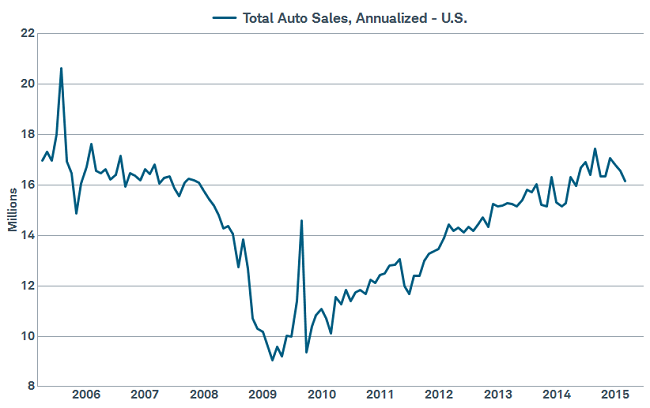

US economic data, relative to expectations, has hit a few soft patches recently. Weaker regional manufacturing surveys were followed up by the Institute for Supply Management’s (ISM) Manufacturing Index falling to 52.9 from 53.5—still in territory indicating expansion but weaker; while the new orders component also fell to 52.5. However, comments in the survey indicated that much of the weakening was due to the west coast dock slowdown, which is now being worked through and should be back on track toward the end of the second quarter. We also saw factory orders fall by 0.2%, and auto sales were also somewhat disappointing after showing strength toward the end of last year.

Auto sales slightly weaker

Source: Bloomberg. As of Mar. 9, 2015.

Housing improvement has also stalled with housing starts, building permits and existing home sales all falling in the most recent readings; while applications for new mortgages have been somewhat weaker than expected. Finally, initial jobless claims were above the key 300,000 level in a couple of recent weeks, although they moved back below that level last week. Weather has been a culprit to much of the recent weakness in the US economy.

The service side of the economy looks better with the ISM Non-Manufacturing Index rising to 56.9 from 56.7, the employment component ticking up to 56.4 from 51.6, and the new orders component dipping slightly to a still robust 56.7. Additionally, the job market continues to improve sharply with the US companies adding 295,000 jobs in February, while the unemployment rate fell to 5.5%.

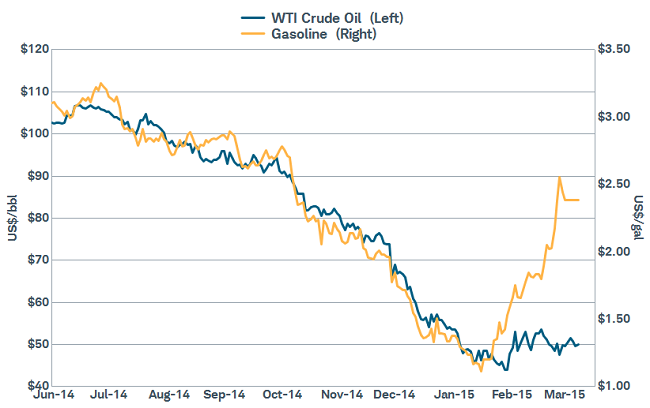

The strength in the labor market may be finally be translating to higher wages—good for the consumer, but a possible weight on corporate profit margins. Unit labor costs rose a surprisingly strong 4.1% in the fourth quarter of 2014, and more companies are mentioning wage pressures as they look ahead. Consumers also continue to receive a tailwind from lower energy costs—although gasoline has moved higher recently as oil appears to be in a bottoming process.

Oil appears to be bottoming but gasoline prices have rebounded some

Source: FactSet, Dow Jones & Co. As of Mar. 9, 2015.

Federal Reserve maintains plans—for now

The Federal Reserve has also attributed much of the recent weakness to temporary factors and continues to indicate the first rate hike will come later this year. But it’s important to note that data could change both the expected start point and the path and speed of rates from that point. Continued or extended weakness could push the first rate hike toward the latter part of 2015 or even into next year. But should wage pressure, combined with a rebound in energy prices, lead to rising inflation expectations, the Fed may need to act sooner or more forcefully than currently expected. Regardless, more volatility seems to be in the cards as we move closer to an initial hike.

Inflated inflation expectation

Highlighting monetary policy divergences, the ECB kicked off QE recently in an effort to battle the increasing threat of deflation in Europe as prices continue to decline. But expectations for the stimulus program, intended to end no sooner than September 2016, may need to be tempered, especially as they relate to inflation.

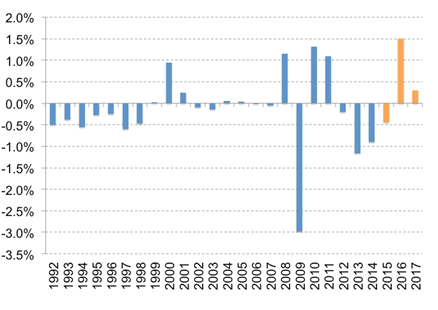

As a result of its stimulus, the ECB expects inflation to reach 1.5% in 2016 from 0% in 2015. The rise of 1.5 percentage points would be the largest ever increase in annual inflation in the Eurozone in at least 25 years. This expectation even eclipses the rise from 0.3% to 1.6% in 2009-2010, when the inflation rebound was fueled by Brent crude oil rising to around $80 after starting the year at $45.

Europe expecting biggest ever rebound in inflation next year

Percentage point change in annual pace of Consumer Price Index in Europe with ECB forecast*

*ECB forecast denoted in orange Source: Charles Schwab, Bloomberg data 3/8/15.

Since the program was announced on January 22, European stocks have welcomed the QE program with a gain of 9% in euro terms (1% in dollar terms). And if the ECB needs to step up its bond buying program as inflation tracks below its optimistic target in the year ahead, investors may have more to cheer.

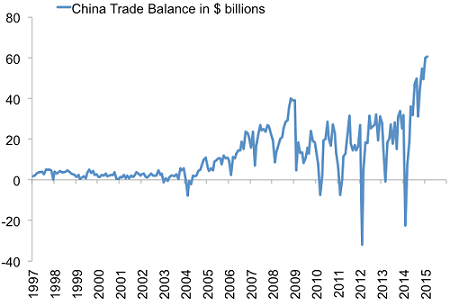

Trade data may be showing early impact of currency moves

China’s currency has been depreciating against the dollar in recent months after a long period of appreciation that began in July of 2005. Currency depreciation is another lever, like rate cuts, that Chinese policy makers are using to help stabilize growth. China’s trade surplus rose to the highest level on record as exports grew steadily in the first two months of the year, on stronger global demand, while imports fell in part due to lower commodity prices.

China’s trade surplus hits new all time high

Source: Bloomberg data, 3/8/2015.

Japan’s merchandise export volume is up more than 11% over the past year, the fastest pace since 2010’s rebound from the global recession of 2008-09. Also, the latest data for exports from the Eurozone is from December; but the seasonally-adjusted data reflect a rise in the pace of growth to 5% from flat over much of the past two years. Together this data suggests that the currency declines seen in a number of countries are paying off in terms of boosting exports and contributing to economic growth.

So what?

US stocks have been resilient, although there has been an uptick in volatility. Economic data has shown some softening, but we believe it is temporary in nature. However, the risk of a correction is elevated in our view and investors should be prepared for such a possibility by having a diversified portfolio and keeping a close eye on rebalancing opportunities after pullbacks. Meanwhile, investors should also look overseas for global diversification opportunities as monetary policy easing should help to bolster asset values.

(c) Charles Schwab