Key Points

-

US stocks ended the first quarter roughly flat, which could end up being positive. Stocks can correct through time or price, with the former allowing earnings to catch up to prices. It may be stomach churning, but a continuation of "a running to stand still" environment is certainly possible.

-

The Federal Reserve remains fairly dovish, but rate-hike uncertainty is a factor restraining the market. US economic growth has disappointed since January, but is likely to rebound in subsequent quarters.

-

Europe’s economy—especially in manufacturing—appears to be improving; while in Japan, recent soft data should be temporary and stocks could see further gains.

That was a lot of work for nothing! US stocks ended the first quarter within shouting distance of where they started. Fed uncertainty, dollar strength, soft economic data, oil volatility, and earnings concerns all contributed to a lot of volatility but little headway. Unfortunately, the current quarter appears is looking much the same so far, with the possibility of a correction still lurking.

But positively, a modestly overvalued market can be corrected through either price or time. At this point, time seems to be the method in force. With prices staying roughly in place, earnings have a chance to recover, resulting in more attractive valuations. Unfortunately, the outlook for the first quarter earnings season is not particularly encouraging, with negative growth expected. And as Liz Ann notes in her recent article “Running to Stand Still: Wild Swings Taking Market Nowhere”, according to BCA Research, there have been three non-recessionary periods since the 1970’s when quarter-over-quarter profit growth has been negative, such as what is expected in this years’ first and second quarters. Soon after these occurrences, the market experienced corrections, which were ultimately short-circuited by Federal Reserve easing—not a likely option this time around. Investors are currently looking closely at earnings reports, which have started for the season, to determine if the weights on earnings are more temporary in nature, or potentially more serious. We lean toward the former but also believe that gains in stocks will be harder to come by in the coming months. Companies also appear to be looking for ways to boost growth as, according to the World Financial Digest, global merger and acquisition (M&A) activity is off to its best start since 2007—before the financial crisis. There will be pockets of outperformance—some of which will be driven by M&A activity—but broad-based above-average gains seem to us to be unlikely.

Economic rebound?

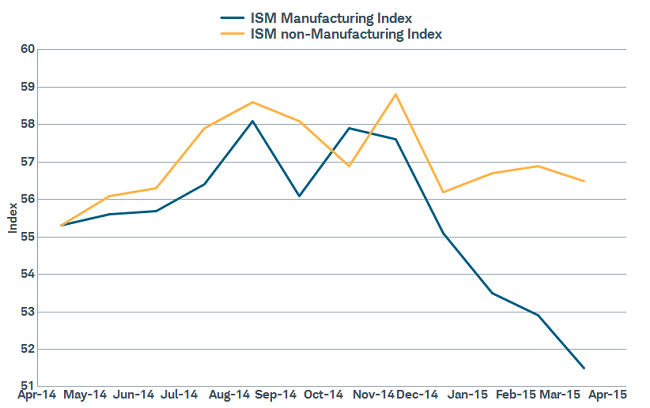

Soft US economic data has marked the first few months of this year, but a rebound is likely in the near future. Cold weather and the west coast port shutdown are being blamed for much of the weakness, but we need to see renewed upward movement over the next couple of months. The March Institute for Supply Management (ISM) Manufacturing Index fell to 51.5 from 52.9, still in territory depicting expansion, but the lowest reading since May of last year. Also concerning was another fall in the new orders component, dropping to 51.8; and employment, which is right on the expansion/contraction line with a reading of 50.0. However, lending credence to the weather and port arguments, the service side of the economy continues to show good strength, with the ISM Non-Manufacturing Index ticking only slightly lower to a still-strong 56.5, while both new orders and employment rose.

Temporary divergence?

Source: FactSet, Institute for Supply Management. As of Apr. 3, 2015.

Additional manufacturing weakness was seen in the durable goods report, which showed a decline in nondefense capital goods ex-aircraft of 1.4%, while the previous month was also revised lower, The data can be volatile at times, but a couple of negative core readings in a row at least warrants a yellow flag. Certainly, the strength in the dollar has been a headwind for US export-oriented manufacturing in this global environment, but dollar gains have slowed, which should help manufacturers find their footing.

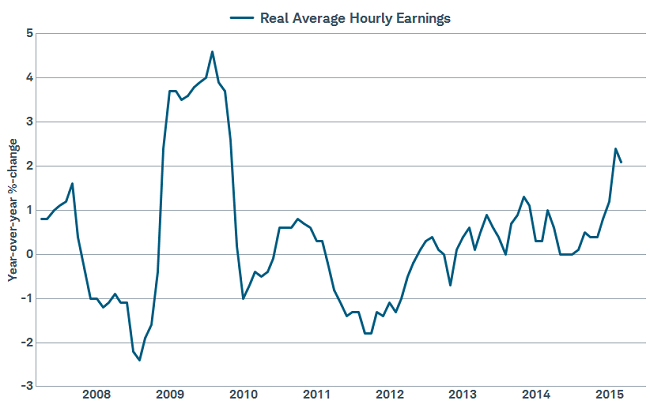

There are positives as well, which lead us to believe economic strength will resurface, potentially helping stocks move higher in the second half of the year. Although the March jobs report was disappointing with only 126,000 jobs added—and the unemployment rate stayed at 5.5%—average hourly earnings ticked higher and the more forward-looking initial jobless claims number remains quite well below the key 300,000 level. There have also been multiple stories of large companies raising their minimum wages, providing hope that long-stagnant wages may be finally on the way up.

Declining unemployment should help to pressure wages higher.

Source: Bloomberg. As of Apr. 3, 2015.

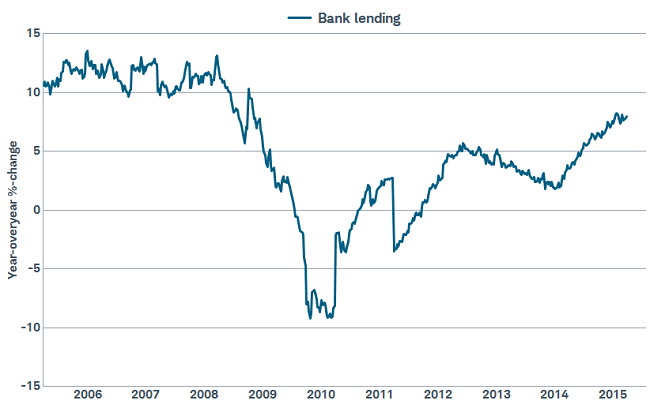

Housing has also been soft recently, but we believe it will be an economic bright spot as the year progresses. Mortgage rates have come down recently, while job growth has improved. In turn, purchase applications have surged according to the Mortgage Bankers Association, a strong leading indicator for further strength in housing. In addition, according to ISI Research, bank loans have increased 7.7% year-over-year, which indicates growing confidence by both banks and borrowers. And after a string of disappointing data, pending home sales for February posted a 3.1% gain.

Bank loans are on the rise

Source: FactSet, Federal Reserve. As of Apr. 3, 2015.

Fed focus set to continue

Uncertainty surrounding the timing of the first rate hike by the Federal Reserve will likely continue to contribute to market volatility. Comments by various Federal Open Market Committee (FOMC) members suggest continued dovishness by the Fed, which should help to support risk assets; but the looming rate hike remains in investors’ minds, potentially dampening their desire to move out the risk spectrum.

It seems unlikely that we’ll get a boost from Washington, as the closer we move toward the 2016 election, the less likely long-hoped for tax reform occurs. Gridlock in Washington tends to be positive for the markets, but there seems likely to be at least some disappointment that more progress wasn’t made on an issue that seemed to be one where bipartisan agreement could be found.

Europe’s economic rebound continues

Unlike US manufacturing, the Eurozone manufacturing purchasing managers index (PMI) posted a strong gain in March, making it four months of improvement. In addition, the UK PMI also posted a gain, continuing its rise since September 2014. These readings are consistent with improving economic growth. On balance, economic data in Europe continues to exceed economists’ expectations. According to the Bloomberg consensus of economists, second quarter real gross domestic product (GDP) in the Eurozone is expected to be 1.3%, the fastest pace since the third quarter of 2011.

Japan’s recent slump seen as temporary

In contrast to the rebound in Eurozone economic data, Japan has seen a slump in the latest data reports. February readings on manufacturing and exports reflect a slowdown perhaps tied to the late Chinese New Year and the port traffic delays on the US west coast. We expect this data to rebound when reported for March.

Japan has spent four of the past seven years in recession, and spent the last two years implementing aggressive policies to spur growth. Therefore, hopes for a rebound in the latest soft data are greater that they have been in many years. Japan began the year on solid footing, growing at an annualized 1.5% real rate in the fourth quarter; as it emerged from two quarters of recession following the government's sales tax hike last April. Growth momentum must return quickly for stocks to sustain and build on the 14% year-to-date rise for Japan’s Nikkei 225 Index.

The latest monetary policy meeting by the Bank of Japan (BoJ) comes exactly two years after it began the world’s most aggressive quantitative easing (QE) program, by pumping enormous amounts of money into the economy with the intention of ending Japan’s deflationary mindset. And the BoJ is showing no signs of letting up. Inflation has cooled as oil prices have declined; but expectations for future inflation, as measured by the futures market, have not pulled back, suggesting market participants see the latest decline in inflation as temporary.

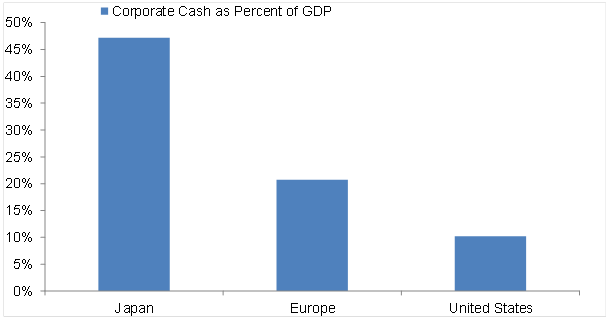

A key positive that may return momentum to growth is that businesses are beginning to spend their cash. Capital investment in Japan rose just 2.8% in 2014. But investment in plant and equipment, M&A activity, and hiring started to pick up in the first quarter; based on announcements from a variety of businesses, including automakers and electronics manufacturers. If Japanese companies start to spend again it could be a powerful driver of growth for the entire economy. Overall, Japanese non-financial companies hold 231 trillion yen in cash, or $1.9 trillion, according to data from the BoJ. That's more than the $1.7 trillion in cash and liquid assets that US non-financial firms have stashed away, according to the Federal Reserve, even though the American economy is nearly four times larger than Japan's. This is one of several reasons Japanese stocks could continue to rise.

Japanese companies have stashed a lot of cash

Source: Charles Schwab, Bloomberg data as of 4/6/2015.

So what?

Volatility will likely continue and more sideways action could be in store for the US equity market. We believe US economic data will start to rebound, helping push stocks higher in the second half of the year. The Fed remains in focus, but a rate hike is not likely until the latter half of 2015, which has helped slow the dollar’s upward momentum; potentially comforting the market and letting businesses better react. Better near-term opportunities may exist overseas as the Eurozone economy is improving and Japan seems poised to rebound from soft data. Get, or stay, diversified and consider international stocks for your portfolio according to your risk tolerance.

(c) Charles Schwab