Key Points

- With earnings season largely complete, and the Fed not meeting again until June, markets seems to be in a wait-and-see mode. Sentiment is relatively neutral and earnings weren’t as bad as initially feared, providing some potential optimism

- First quarter real gross domestic product (GDP) was weaker than expected but the Fed continues to point to transitory factors. While a June hike seems unlikely, an expected rebound in data should help support a September lift-off.

- European elections should shed light on the future of upstart political parties largely founded on shaking things up. Meanwhile, money growth should be more of the focus for investors and that could bode well for European markets.

The US stock market appears to have entered a bit of a wait-and-see mode. Stocks have treaded water during this earnings season, while investors have stayed relatively cautious; pulling more money out of equity funds and directing them toward bond funds. Valuation concerns abound, as well as a continued hangover from the great recession in 2008 and the well-publicized “flash crash.” This is despite stocks continuing to hit record highs, with even the NASDAQ surpassing highs not seen since the peak of the tech bubble in 2000.

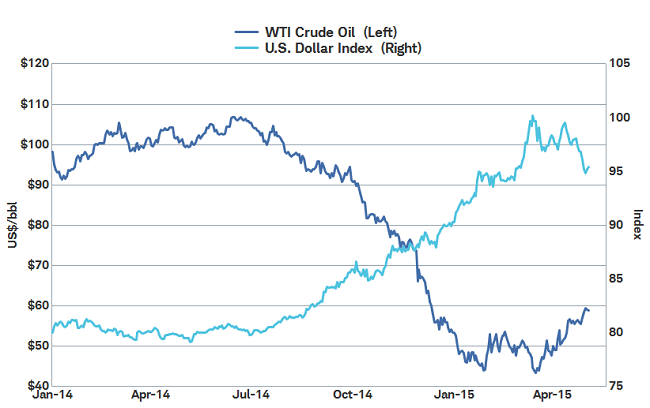

For now, a market that continues to grind higher with elevated day-to-day volatility is the most likely near-term course. As we expected, first quarter earnings season has been better than expected. According to Evercore ISI Research, coming into the season, expectations were for year-over-year earnings to decline 5.6%, while as of May 5 those expectations had been raised to a gain of 1.7%. Much of the weakness was attributable to the energy sector as well as the impact of the stronger dollar on multinational firms’ currency translations. Oil has staged a significant rebound, while the gains in the dollar have stalled, which should allow for better results as we move through the second quarter. Current expectations are for second quarter earnings to fall 4.3% year-over-year, which, given recent history, should prove to be too low—setting up for potential upside surprises in the July reporting period.

Dollar has stabilized and oil likely bottomed in March

Source: FactSet, Dow Jones & Co., InterContinental Exchange. As of May 4, 2015.

History supports rebound theory

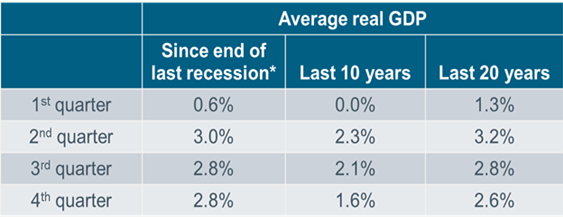

The first reading of economic growth in the first quarter came in quite a bit softer than expected at an annualized growth rate of 0.2%. Severe weather, the west coast port shutdown, and the demise of capital spending in the energy sector all contributed to the weak reading. But it’s certainly not without precedent, as there’s been a pattern of first quarter weakness. As you can see in the table below, during this recovery—as well as the past 10 and 20 years, first quarter growth has been consistently very weak; only to rebound in subsequent quarters.

*3Q09-1Q15. Real GDP based on annualized Q/Q % change. Source: Bureau of Economic Analysis. Past performance is no guarantee of future performance.

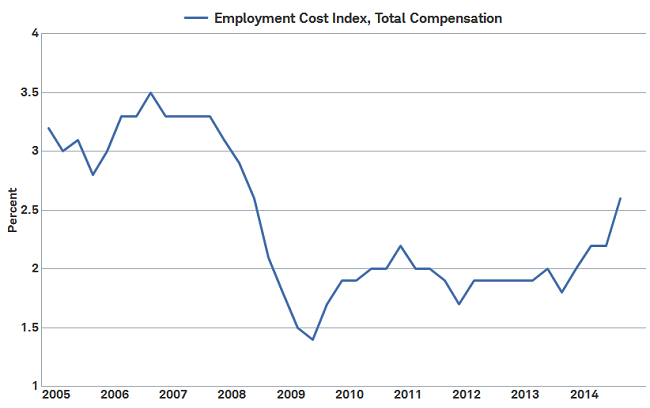

There are indeed glimmers of hope regarding a second quarter rebound. Primarily, the labor market has continued to improve. Jobless claims recently fell to a 15-year low, while the April jobs report showed that 223,000 jobs were added—in line with expectations—but the prior month’s gains were revised sharply lower. The unemployment rate fell to 5.4%, which was also in line with expectations, and now at the lowest level since May 2008. According to the Bureau of Labor Statistics average Hourly Earnings (AHE) edged up 0.1% for the month—up 2.2% from a year ago—while the workweek was unchanged. Another well-watched (and arguably better) indicator of wages—the Employment Cost Index (ECI)—moved 0.7% higher in the first quarter and was up 2.6% year-over-year. Private wages did even better, rising 2.8% year-over-year, which was up from 1.7% one year ago—moving in the right direction and seeming to gain momentum. All of this data suggest we may finally be seeing some traction in wage growth.

Wages finally starting to rise…

Source: FactSet, U.S. Dept. of Labor. As of May 4, 2015.

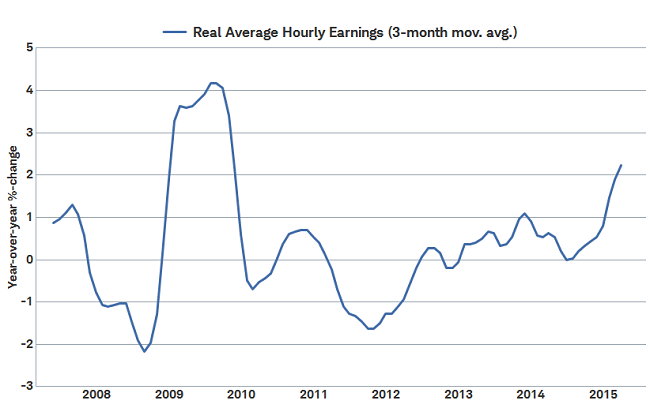

By various measures

Source: Bloomberg. As of May 4, 2015.

Other data has been mixed. The service side of the economy continues to look relatively good as the Markit Services PMI Index fell to 57.4 but remained well into territory depicting expansion. However, the manufacturing side is more uncertain as the Markit Manufacturing PMI also remained in expansion territory, but was much closer to the dividing line at 54.1. Further, mixed messages are coming from the regional surveys, with the Dallas Fed Manufacturing Index remaining well into negative territory at -16.0, while the Chicago PMI rose to 52.3. We expect manufacturing to improve with the slowing in gains in the dollar and recovery in oil prices, but doubts remain.

Fed holds again—future wide open

The April meeting of the Federal Open Market Committee (FOMC) gave us no surprises, but it has now removed all time-related guidance. The FOMC believes that much of the first quarter weakness was transitory, and the economy will rebound in coming months, helping support a rate hike at some point this year. We believe September looks like the most likely time for an initial hike at this point, but that could certainly change. A reminder to investors that equity volatility typically heats up as we grow closer to a rate hike, so be prepared!

May elections gauge Europe’s political fragmentation

Across Europe new political parties have been on the rise. The May 7 general election in the United Kingdom and the May 24 regional elections in Spain make May a key month for mapping this growing political fragmentation and rejection of a unified Europe.

Should the new parties win sizable representation and further fragment the political landscape, policy in European countries may become less predictable, as it has in Greece. Despite the potential for market volatility, the outcome is unlikely to be anywhere near as destabilizing to the stock market in these countries as what has taken place with Greece's deliberations with its creditors. For example, unlike Greece, Spain has successfully exited its bailout program, and is helping (along with Ireland) to lead the entire Eurozone to better growth in 2015.

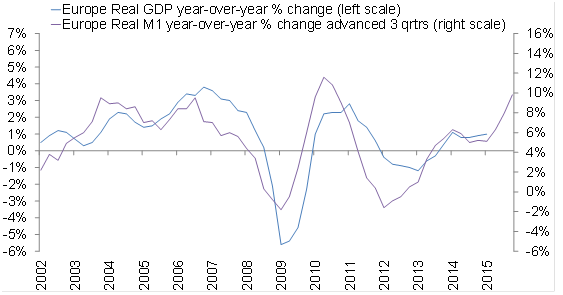

Europe’s growth may follow the money higher

Historically, changes in Europe’s money supply have been a good leading indicator of economic growth. Changes in the inflation-adjusted money supply measured by M1 (which includes coins, currency, and cash held in checking accounts) have led the change in GDP by about three quarters, as you can see in the chart below.

Money growth is what matters

Source: Charles Schwab, Bloomberg data as of 5/5/2015.

The sharp rise in the real money supply is pointing to stronger economic growth in Europe in the quarters ahead. Economists have started to revise their Eurozone GDP estimates for 2015 higher. In the two months since the start of February, the Bloomberg-tracked economists’ consensus estimate for Eurozone GDP in 2015 has risen from 1.1% to 1.4%. The increasingly aggressive actions by the European Central Bank (ECB) that have led to more rapid money supply growth may continue to lift growth estimates, supporting the stock market.

So what?

Patience can be tough, especially in investing, but that is what is needed at the present time. While a sharp upward move in equities seems unlikely, and the risk of pullbacks is elevated; a grind higher is not something most investors should miss out on. Economic data and the Fed will continue to be in the spotlight, and we expect improvement that will lead to both a Fed rate hike and increased equity volatility—so be prepared. Across the pond, political uncertainty exists, but money supply should be the main focus, which could bode well for the possibility of future European equity gains.

(c) Charles Schwab