Key Points

- The stock market has made very little progress this year but also has showed some remarkable resilience in the face of pending US rate hikes and the back-up in bond yields. This stalemate could continue for some time, with volatility expected to rise heading toward the first rate hike.

- The US job market is a bright spot economically, helping bolster the case for rate hikes. However, soft data elsewhere suggests the US economy continues to struggle to grow above trend.

- Monetary stimulus measures appear to be helping boost European inflation, which we believe should set the stage for better European equity performance in the coming months.

A tug of war.

Little progress made on the equity front

Source: FactSet, Standard & Poor's. As of June 10, 2015.

That’s the best description we have for the above chart. The bears gain a little, than the bulls battle back, and vice versa, with some decent sized daily moves, but no real movement off that middle ground. With a maximum year-to-date gain of less than 3.5% on a closing basis so far this year—and a maximum decline of less than -3.25%; according to Bespoke Investment Group (BIG), there has never been a year when the S&P 500 has hovered this close to the unchanged level on year-to-date basis so far into the year (110 trading days). There are only three other years (1952, 1993 and 2004) when the index wasn’t up or down more than 5% at some point in the year by early June. In all three of those years, the market gained between 4% and 10% for the remainder of the year. For the top 10 narrow-range years, the index averaged a 4.9% gain, with positive returns 90% of the time.

For those that have watched epic tug-of-war matches, the question is which side gets pulled into the mud pit first? Given the somewhat extended valuations, numerous risk factors such as the Greek debt situation and geopolitical issues, and the extended period since the last official correction (April-October, 2011) in equities, we believe correction risk is still present in the near-term, but believe such a move would be healthy and set up for the bulls to reestablish their dominance. Also, investors waiting to invest for such an event have missed much of the upside, so we don’t recommend attempting to market time—stay diversified and consider some protection strategies if you’re nervous about the possibility of a sharp pullback.

The international picture continues to have a large impact on the United States, with the German bund again being at the center of attention, along with the ongoing debt drama in Greece.

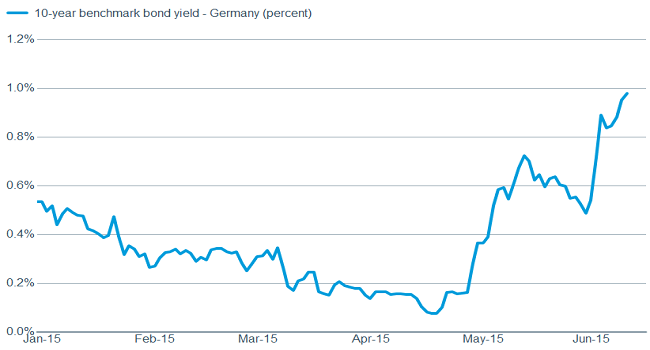

Bund volatility continues

Source: FactSet, Bundesbank. As of June 10, 2015.

After the most recent meeting of the European Central Bank (ECB), President Mario Draghi warned markets to expect more volatility in the bond markets, and he’s certainly been accurate to this point. And here’s one of the core issues causing the tug of war, as higher rates are cheered by some as meaning the threat of deflation has passed and that economies are growing; while others are concerned that higher rates may hinder activity that is already sluggish at best, while also making valuations in equity markets less attractive. We continue to believe that the upside to rates is relatively limited over the course of this year, with dovish central bank policies continuing and economic activity still tepid, but slightly higher rates are nothing to fear and should be welcomed by most investors as it helps to signal a potential return to more ordinary economic and monetary conditions.

Economy perking up…kind of

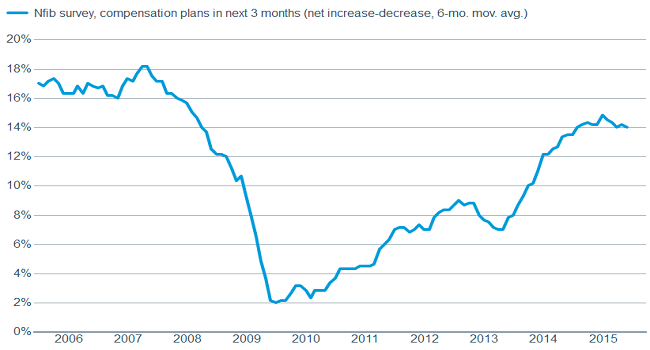

US economic activity has rebounded a bit in the second quarter and we expect that to continue. The job market continues to be a highlight, with jobless claims running near historic lows, the Bureau of Labor Statistics reporting another 280,000 jobs were added in May, while the unemployment rate ticked higher to 5.5% as the labor participation rate rose. This continued tightening of the job market also appears to be putting some mild upward pressure on wages, with average hourly earnings (AHE) posting a 2.3% year-over-year gain-up from 2.2% in April and 2.1% in March, which should help to bolster the American consumer. At the same time, other measures of wage pressures—including the Employment Cost Index (ECI) and the “plans to raise compensation” component of the latest survey out of the National Federation of Independent Business (NFIB)—are showing even sharper accelerations.

Upward bias for wages growing

Source: FactSet, National Association of Independent Business (NFIB). As of June 10, 2015.

But the consumer remains a bit of an enigma, not yet returning to their free spending ways seen before the Great Recession. But there is a light; with May’s retail sales coming in at a healthy (and expected) 1.2% growth rate; while April’s reading was revised up. But the savings rate continues to rise, and personal debt as a percentage of personal income continues to fall, so deleveraging continues. It’s too soon to say that consumer attitudes have changed permanently, but there does appear to be an extended period of caution by consumers which could lead to still-subpar economic growth over the coming quarters.

That said, the housing market is showing signs of strength again, with new home sales up 6.8% in April, while housing starts rose to their highest level since November 2007; and mortgage applications surging as well. These data points are supportive of our view that a Fed inching toward rate hikes (and rising longer-term rates) could be the trigger to move potential home-buyers off the fence as they anticipate higher rates down the road. Additionally, vehicle sales rose to a 17.8 million saar (seasonally adjusted annual rate), the highest since July 2005 according to the Wall Street Journal.

Doves and hawks

The tug of war also continues in the Federal Reserve, with a sizable number of Federal Open Market Committee (FOMC) members wanting to raise interest rates sooner rather than later, while some believe it should hold off until at least the beginning of next year. The International Monetary Fund (IMF) and World Bank also felt the need to chime in, by urging the Fed to wait until the first half of 2016 to embark on rate hikes. You can place us firmly in the sooner-rather-than-later camp of raising rates; likely in September. We believe it would help return the investing world to a more normal environment and aid savers—especially those nearing retirement, who have had to venture out the risk spectrum for yield. But initiation won’t likely mean a stair-step series of hikes is in store—the Fed has telegraphed it will be very cautious and data dependent in an effort not to short circuit the economic expansion. History shows the stock market performed much better when the Fed was hiking rates slowly vs. more quickly. At this point, the Fed wants to normalize monetary policy, not tighten so the economy will slow as is typically the reason for hiking rates.

Europe on the upswing

Europe’s economy has benefitted this year from a broad array of stimulus in the form of near-zero interest rates; a bond buying program, also referred to as quantitative easing (QE); a weak euro currency; and lower oil prices combined with rising bank lending and rising stock prices. This week, Eurostat released the internal make-up of first quarter gross domestic product (GDP) in Europe which revealed solid consumer spending growth (up +0.5% for the quarter, or an annualized +2%) along with a welcome increase in business spending (a rise of +0.8% for the first quarter, or an annualized +3.2%). Business spending has steadily improved; from +0.4%, +0.1%, and -0.5% over the prior three quarters, respectively.

The better growth trend seems to be sustained in the second quarter with Eurozone retail sales rising +0.7% in April from the prior month, the best pace since April 2011. Also, German industrial production and factory orders rose during April, according to data from the Bundesbank; while merchandise exports rose to a record high during the same month, per the German Statistics Office.

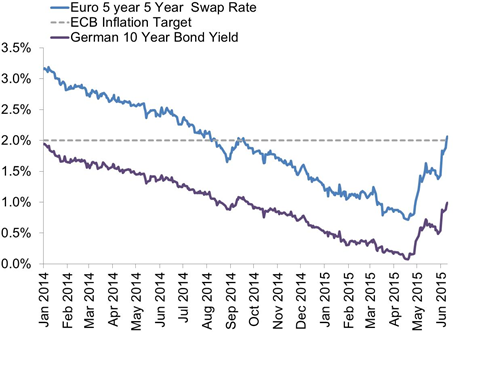

The improvement in European economic data is helping to push bond yields and inflation expectations higher. In fact, just this week inflation expectations moved back above the 2% target level of the European Central Bank (ECB). This measure, known as the 5-year/5-year swap rate, was mentioned in a speech by ECB president Mario Draghi as “the metric that we usually use for defining medium term inflation” when it dropped below 2% last August. The rebound to 2% is encouraging as a sign of better long-term growth prospects and that deflation is likely to be avoided.

Rebounding outlook for growth and inflation in Europe

Source: Charles Schwab, Bloomberg data as of 6/10/2015.

Bond yields have moved sharply higher from very depressed levels. For example, the German 10-year bund yield has moved this year from a low of 0.07% on April 20 to over 1.0% this week. This has caused some jitters in the stock market with yield-sensitive stocks in the utilities and telecommunications services sectors leading the European stock indexes lower by 3% over the past month. Periods of rising bond yields in recent years have more typically coincided with a rise in stocks as the benefit of higher longer-term interest rates for financials combines with the lift to cyclical sectors from improving growth prospects tend to outweigh the impact of higher yields on defensive sectors. Despite the market volatility stemming from rapid moves in rates, we expect the improving outlook to support stocks in Europe.

So what?

The current stalemate in the US market could continue for some time, with bouts of volatility and pullbacks expected as the market anticipates the initial rate hike. Be prepared by staying diversified and consider buying protection, but we would view such an event as the pause that refreshes and help set up the next sustainable bull run. Investors should also look overseas as the aggressive stimulus measures being taken by the ECB appear to be beneficially impacting the economy, and may help equities perform better in the coming months.

(c) Charles Schwab