Key Points

- Stocks continue to trade in a remarkably narrow range, showing both resiliency and hesitation. The threat of a near-term pullback is elevated, but we believe this stalemate will ultimately be resolved on the upside.

- The second half US economic acceleration is tepid, but slow and steady gives flexibility to the Fed and provides a path for stocks to move higher responsibly

- China's move to devalue its currency may not mean what you think.

The pace of your average tortoise may be too quick to describe the move in US stocks to this point in the year. The trading range has been the narrowest in history through July; with the glass half-full camp noting the resiliency of the market in the face of some intense headwinds, including the recent volatility as a result of China’s currency devaluation. We believe the US stock market impact from China’s moves will be relatively mild and short-lived. Central banks around the world—including the European Central Bank (ECB) and the Bank of Japan (BoJ); along with the People’s Bank of China (PBoC)—continue to pump liquidity into the global economy, which should continue to support risk assets. However, the glass half-empty camp would note elevated valuations, flat corporate earnings, weak market breadth, and the fact that investors still aren’t embracing this bull market as evidenced by the $75 billion pulled out of equity mutual funds through the end of July according to Evercore ISI Research.

That skepticism, combined with the slow but steady economic growth we’ve seen—which should be bolstered by lower commodity prices—suggests the stalemate is not indicative of an end to the secular bull market. Past bear markets typically haven’t occurred without being in close proximity to a recession, of which there are no signs at present. However, we are in a weak seasonal phase for the market based on history; and the initial rate hike by the Federal Reserve is looming. Volatility is to be expected and we remain neutral on US stocks, which means investors should take no additional risk above their appropriate long-term US equity allocation.

Slow and Steady Wins the Race?

The consensus has been for a pick-up in US economic growth from the nearly flat performance of the first quarter; but so far the rebound has been tepid. But the old adage “be careful what you wish for” seems apropos as a faster rate of growth would likely have caused interest rates to move higher, and the Fed to move more quickly and forcefully. The indication from the Fed that the pace of rate hikes will be slow and methodical could allow stock market valuations to improve through time rather than price. And as we’ve noted in the past, historically, slow tightening cycles have been quite a bit more rewarding to the stock market than fast cycles. However, the Fed will be moving rates off the zero bound—where they’ve been for six-and-a-half years—so only the very naïve would assume the market can sail smoothly through those uncharted waters.

The Fed is unique among global central banks as it operates with a dual mandate—inflation and employment. The unemployment rate has fallen to 5.3%, where it remained in the latest labor report, with 215,000 jobs being added in July. Wages, however, remain relatively stagnant, with average hourly earnings (AHE) rising only 0.2%, after a flat reading in June; although the workweek did expand slightly, putting a little more upward pressure on wages. Additionally, the Employment Cost Index (ECI) for the second quarter was up an anemic 0.2%—the weakest reading on record, which began in 1982. We don’t want to read too much into this number as other indicators, such as Fed surveys and minimum wage increases, indicate wages are on the verge of moving higher.

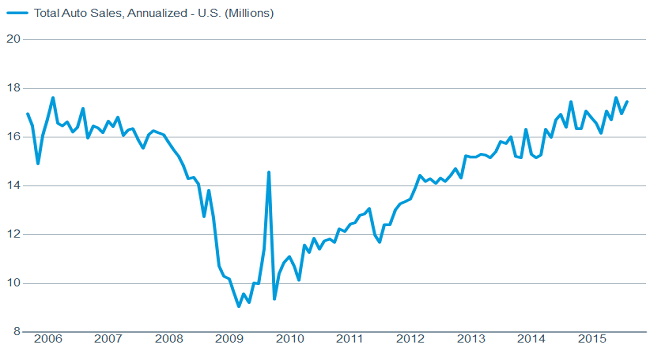

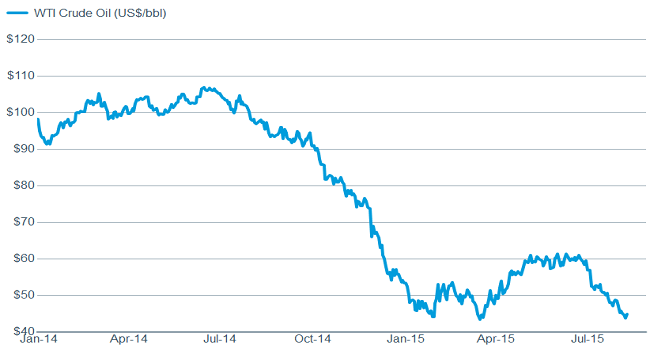

US manufacturing continues to grow, with both the Institute for Supply Management (ISM) and Markit surveys remaining in expansion territory in July. The larger services portion of the economy has accelerated even more sharply, with the ISM non-manufacturing index moving to its best level since 2005. Also encouraging for the future, the orders component of both ISM surveys moved nicely higher. The solid sentiment among manufacturers is encouraging in the face of a commodities collapse that has seen companies in the energy and materials spaces announce plans to decrease spending on new equipment. Helping offset that, however, is the auto industry, which continues to expand, indicating growing confidence among consumers. Lower oil prices have prompted greater purchases of typically-less fuel efficient, but more profitable trucks and other vehicles.

Auto sales are rising

Source: Bloomberg. As of Aug. 11, 2015.

Likely helped by lower oil prices

Source: FactSet, Dow Jones & Co. As of Aug. 11, 2015.

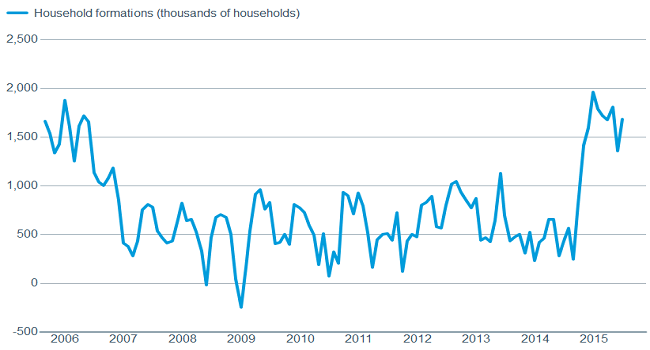

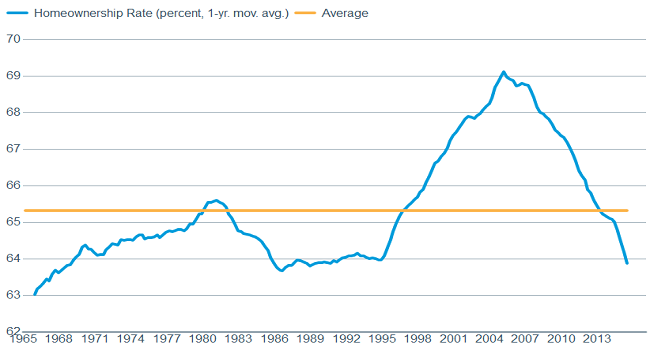

While retail sales data has been relatively tepid, and the recent personal spending report showed little growth, stronger vehicle sales, along with an improving housing market, lead us to believe the consumer is actually doing relatively well. But the post-debt supercycle era has ushered in a more frugal consumer, who is more prudent about savings, paying down debt and spending. A bright spot in the US economy remains housing, which should bolster the economy further. The recent surge in household formations and the US homeownership rate likely having overshot on the downside, suggest many of the excesses from the height of the housing boom have corrected.

An increase in household formations is a good sign for housing

Source: Bloomberg. As of Aug. 11, 2015.

While the homeownership rate seems to have overcorrected

Source: FactSet, U.S. Census Bureau. As of Aug. 11, 2015.

The Fed embraces the tortoise, while regulatory burdens are a bipartisan issue

The combination of a slowly improving economy—with both housing and job growth healthy, and little to no inflationary pressure—is a scenario that has allowed Fed Chair Janet Yellen to communicate a desire to lift rates at some point this year. Although there remains a contingent of Fed members that are less anxious to raise rates, the consensus is that it’s time to move off the zero bound and stop treating the economic patient like it’s still in the emergency room. September still seems like the probable jumping off point; although expectations thereof did diminish at least temporarily when China announced its new currency policy (more on that later in this report).

In Washington DC, in a unique twist, both sides of the aisle seem to agree that the regulatory environment is overly burdensome, weighing down the US economy, and contributing to the low productivity rate. The Obama Administration says it aims to reduce regulatory burdens for small business, and recently urged states to review their complicated web of mismatched regulations—a mission Republicans have had for some time. Any movement on this front would be beneficial to small businesses—the lifeblood of the US economy, especially as it relates to job creation.

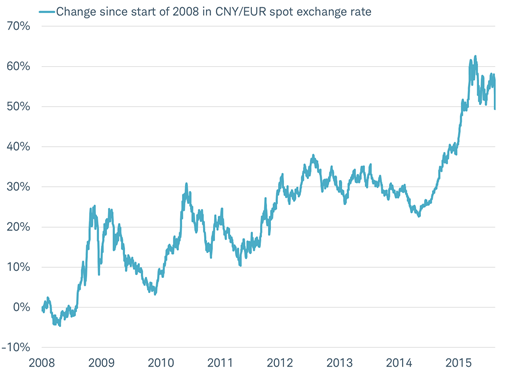

China’s currency slide follows a long rise

During a typically slow summer vacation time for investors, China surprised markets with an initial move to lower the exchange rate of the renminbi (or yuan) to the dollar by just under 2%. Most importantly, the PBoC also announced that the exchange rate would be fixed each day based on the prior day’s market price, supply and demand, and the movement of major world currencies. While some may see the moves as an escalation of a global “currency war,” Chinese policymakers have three primary motivations that supersede driving the currency down purely for export gain.

First, China’s original decision to have the renminbi pegged to the dollar has meant that over the past year the Chinese currency has soared relative to the euro and the yen, the currencies of key trading partners. Since the start of June 2014, when the dollar began its sharp rise against other major currencies, the renminbi has been the world’s strongest currency—outpacing the rise in other gainers such as the US dollar and the Swiss franc. The rate hike(s) by the Federal Reserve likely to take place later this year may lift the US dollar further; and the renminbi, if there had been no change in policy. Rather than escalating a currency war, China’s move to weaken the renminbi simply helps stabilize the currency after a strong gain of around 60% over the past seven years.

China’s currency has generally risen strongly against those of its trading partners

Source: Charles Schwab, data as of 8/13/2015.

Second, a more flexible and market-oriented exchange rate is a response to the recent report from the International Monetary Fund (IMF) describing the criteria necessary for the renminbi to join the US dollar, euro, pound, and yen in the IMF’s special drawing rights (SDR) basket. The SDR is an elite group of currencies used to value reserve assets and China would like its currency included. The renminbi met the IMF requirements in terms of international trade, but it did not meet the criteria of being a freely usable currency, according to the IMF report. The IMF also noted a more market-oriented exchange rate would aid implementation if the renminbi were included in the basket. This week’s shift in exchange rate policy to a more market-oriented approach is another step toward China’s goal of a reserve currency.

Third, a rising currency has helped to push down prices; and China is now facing deflation risks, with inflation in a range of 0.8-1.6% this year. While inflation erodes the value of debt over time, deflation does the opposite, and China has seen rapid debt growth in recent years. A weaker currency can help generate inflation by making imported goods more expensive in local currency.

These are three important reasons China has made changes to its currency policy, and have little to do with a “currency war.” We view the moves as generally positive for Chinese economic growth. However, a sharp drop in China’s currency could actually work against stabilizing growth in China. China’s economy is in transition from export-oriented manufacturing to domestic consumer spending…but the transition is not smooth. The rise in the exchange rate in recent years benefitted consumers who saw imports get less expensive; while hurting export manufacturers who suffered with higher prices. A concern with currency movements is that there is no win/win strategy. China’s currency moves may signal that the slowdown in manufacturing has been too rapid and a rebalancing is in order at the expense of consumer spending. The mix of data on manufacturing, compared with the service sector and consumer spending, will offer some indication on further currency moves or policy shifts.

So what?

The narrow trading range for US stocks continues, but there are some concerning signs such as seasonality and technical issues that make us a bit more cautious in the near term. We don’t think the bull market is in danger of ending, but there could certainly be a pullback and we don’t believe investors need to be in a great hurry to put money to work. In the immediate aftermath, China’s move on its currency rattled markets, but we don’t think it’s the start of a currency war, and hope that this is part of a herky-jerky path to freer markets.

(c) Charles Schwab