Sticking with Equities when Volatility Strikes

Does recent market turbulence increase the chances of higher volatility in the months ahead? Our research says yes. But don’t ditch an allocation to equities—instead think about how to stay invested while reducing risk.

Equity investors have had a rough ride since midsummer. Anxiety about the slowdown in China triggered a sharp decline in equities during August. But uncertainty had been brewing for a while: concerns over the Fed’s looming interest-rate hike have lingered, and the market turbulence surrounding the potential for a Greek exit of the euro occurred only in July.

Back with a Vengeance

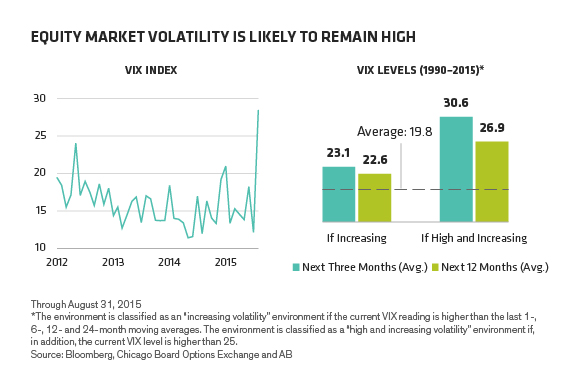

Now, volatility is back with a vengeance. The VIX Index, an index of expected US market volatility, spiked 135% from 12.12 in July to 28.43 in August (Display 1, left). That’s a record monthly increase, and puts the VIX at a level higher than it was in almost 90% of the months since 1988.

Is this is a bad omen? Probably. Volatility tends to be sticky. The VIX has averaged just under 20% since 1990. When volatility rises, it tends to auger modestly above-average volatility over the next three and 12 months (Display 1, right). However, when the VIX was both high and rising—like it was in August—future volatility levels were much higher during the subsequent months.

Volatility Doesn’t Predict Market Direction

This means that we’re more likely to see volatility persist this time. However, higher volatility doesn’t necessarily mean that the market will trade down. It’s very difficult to predict market direction. But that doesn’t stop many from trying to time the key inflection points.

When turmoil strikes, the natural instinct for many investors is to sell equities. We think that would be a mistake. Selling during a turbulent period will often lock in losses. And then where do you go? Today, it’s hard to find asset classes that offer a compelling long-term return potential. Our capital markets engine expects global equities to deliver an annualized return of 6.1% over the next 10 years, much lower than the 10.3% delivered over the last 30 years. Still, it’s much higher than our expected return—2.3%—from investment-grade bonds.

Shock Absorbers for Turbulent Times

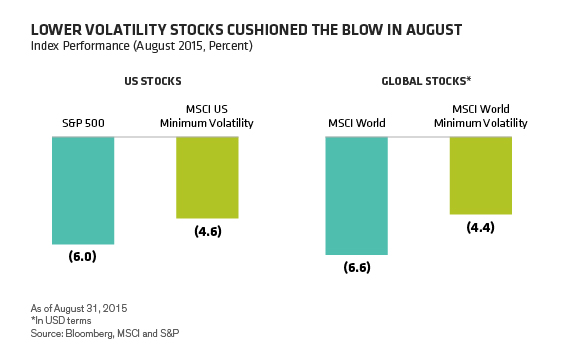

Instead of cutting exposure to equities, consider a portfolio that has built-in shock absorbers. One example would be equities with lower volatility characteristics. In fact, both global and US lower volatility equities stood up to the test in August, declining much less sharply than the broader market indices (Display 2). In the US, minimum volatility stocks fell 146 basis points less than the S&P 500 Index in August. In other words, they softened the blow of a nasty market environment by 25%. Less than a year ago, we saw similar results during a spike in market volatility in October.

This protection is important. It can allow investors to feel more comfortable staying in equities during tougher times. By losing less when markets fall, portfolios can recoup their losses faster when a stock recovery gathers momentum. And our research shows that active focusing on lower volatility stocks with higher quality characteristics in an active portfolio is a good strategy for navigating volatility, including during periods of rising interest rates.

Volatility is probably here to stay for a while. But even in a more turbulent environment, we believe that abandoning equities will set investors up for disappointing results that will make it harder to meet financial goals. Lower volatility stocks can help investors stick with equities for the long term, while reducing the pain along the way when markets get ugly.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.