Core bond investors tend to have a strong “home bias.” But our research shows that global bonds have offered comparable historical returns and considerably lower volatility than local markets over the long term. In addition, a global approach offers protection when local rates climb.

Going global diversifies an investor’s interest-rate risk and provides other potential benefits too. Over long periods, countries’ economic cycles, business cycles, monetary cycles and yield curves have not been highly correlated.

As a result, countries’ sovereign-bond returns differ greatly year by year. As do opportunities. And risks. Sounds worrisome? Think again: your own country is part of this mix, and if you’ve got a home-centric portfolio, it’s riding troubled seas without the ballast of diversification.

A Bigger Pond

The most obvious benefit to going global comes from a much larger opportunity set. At the end of 2014, the Barclays US Aggregate Bond Index comprised nearly $18 trillion in outstanding debt and about 9,000 issues. Its global counterpart, the Barclays Global Aggregate, was made up of more than 16,000 issues worth roughly $43 trillion.

For the active manager, that’s a much bigger pond to fish in.

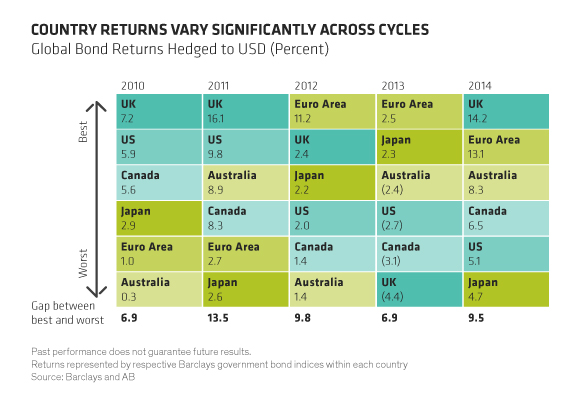

And the range of hedged returns among developed countries has been striking (Display 1). For example, in 2011, hedged sovereign UK bonds outperformed those of bottom performers Japan and the euro area by 13.5% and 13.4%, respectively. The next year, the euro area was a top performer, beating Australia by 9.8%.

In contrast, in most years, the return gap between the best- and worst-performing sectors of the US Aggregate is a couple of percentage points. Having a large gap between country returns provides a lot more potential for an active manager to add value.

A Potential Risk Reducer

And there are more advantages to globalizing the core bond portfolio. We found that, in the 25 years ending December 31, 2014, the Barclays Global Aggregate, hedged to US dollars, captured 95% of the average quarterly returns posted by the Barclays US Aggregate when the latter index was in positive territory, but only 67% of its average quarterly loss.

That’s a meaningful skew. It means that investors who globalized preserved significantly more capital than those who remained US bound.

We also looked at this from the perspective of risk mitigation: during extreme down months for US Treasuries and, separately, stocks, what happened to the correlation between those asset classes and global bonds?

We found that during those periods, not only was the diversification benefit better for global bonds, but the correlationsshrank and the diversification benefit increased—in some cases dramatically. In other words, investors got more risk mitigation from being global when they needed it most.

In the case of stocks, for example, between 1987 and 2014, the correlation of US bonds to the S&P 500 during extreme down months for US Treasuries was –0.13, compared to –0.30 for hedged global bonds.

Global as Core Bond

Adding global is not just a tactical strategy for periods of market drama. Global bonds can meet investors’ core objective by serving as a low-volatility anchor to windward.

But not just any global fixed-income portfolio can serve this function. What’s the secret? Hedging out currency risk (the whys and wherefores will be the topic of our next post).

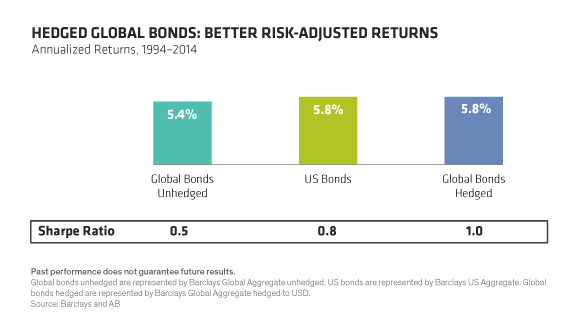

The return of a hedged global bond portfolio has historically matched that of a US-only portfolio, but with—perhaps surprisingly—lower volatility. The risk-adjusted return, or Sharpe ratio (Display 2)—tells the full picture. Over the past 20 years, hedged global bonds have delivered a Sharpe ratio of 1.0, compared with US bonds at 0.8.

In short, hedged global bonds are a better way to meet the core bond objective. And with US rates heading higher soon, now is a good time to make the move.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.