Hedging or Cross Hedging? It Makes a Difference

We recently wrote that currency hedging is critical for core bond investors. But not all hedging is created equal. Cross hedging is not the same strategy. Even though it can look deceptively similar, it will not deliver the same results to the investor’s “volatility” bottom line.

Hedging is all about reducing risk, even eliminating it. Cross hedging is about shifting risk. But in cross hedging, the investor remains exposed to currency risk. Indeed, if historical currency correlations break down, the investor may find that he or she has a higher risk profile than before taking on the cross hedge.

Behind Door Number One: The Direct Hedge

Assume you are a US dollar–based investor who wants to buy a South Korean bond. This will give you exposure not only to the Korean bond market, but also to the South Korean won. Let’s further assume that as a stability-seeking investor you don’t want that currency risk.

One option is to fully hedge the currency with a direct hedge. In that case, when you buy the bond, you can simultaneously sell short the South Korean won in a currency forward contract to offset the currency risk. This has the effect of fully eliminating the currency’s associated volatility.

Behind Door Number Two: The Cross Hedge

A second option is to cross hedge. In one common form of cross hedging, you would sell short a different currency, effectively but imperfectly shifting your currency risk. In our example, when you buy your South Korean bond and the won with which you pay for the transaction, you decide to sell short Japanese yen as a cross hedge.

But the question is: Does this second type of hedge actually reduce risk, which is your objective?

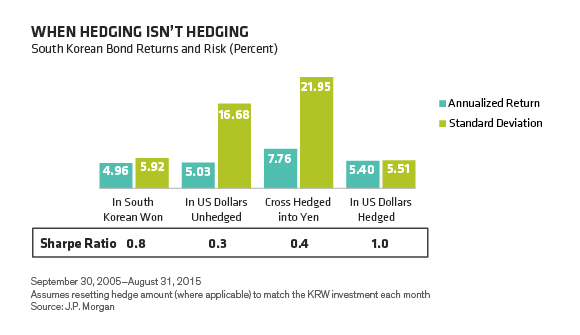

As shown in the Display below, although returns were indeed higher for cross hedging over the past 10 years, the volatility profile of the two strategies was hugely different. In terms of returns, the direct hedge performed similarly to the local Korean bond market. However, the cross hedge didn’t function like a hedge at all, behaving instead in an even more volatile fashion than the security that was not hedged in any way.

The risk-adjusted return, or Sharpe ratio, tells the whole story: a US dollar–hedged investor in the above scenario had a Sharpe ratio of 1.0, while the cross-hedged investor had a Sharpe ratio of just 0.4.

That kind of volatility runs counter to your objective of reducing currency risk.

We think that if an investor is looking to manage volatility—and especially if an investor thinks of their bond portfolio as a source of stability—direct hedging is the right approach.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.