Schwab Market Perspective: Bulls, Bears…and Hippos?

Key Points

- Earnings season has been decidedly mixed, with the recent strength in the US dollar taking a lot of the blame. The stock market has held up fairly well; and we continue to believe the bull market isn’t dead, but it’s in a more mature phase which will be marked by volatility and pullbacks.

- The US economic picture has become partially cloudy. The manufacturing sector remains weak—but representing only 12% of the US economy, it’s dwarfed by the much healthier services sector, covering 88%. Uncertainty continues regarding an initial rate hike by the Federal Reserve (Fed), but odds of a 2015 launch continue to fall.

- The Chinese economy appears to have avoided a hard landing and may actually be on an upward trajectory. Given the size and scope of China, more stable growth should benefit economies (and confidence) around the world.

The hippopotamus market

When trying to describe our view of the market, we realized that bullish and bearish were quite limiting and could cause confusion. Bullish, for example, could mean anything from skyrocketing markets to very modest gains—one word, very different environments. So, we are introducing a new animal descriptor that should more accurately describe our view of the stock market—the hippo. While not initially obvious, we think this is the perfect descriptor, and who doesn’t love hippos? They are extremely large animals that generally move in a forward direction at a very modest pace, but with occasional outbursts of volatility (hippos are the deadliest large animal in Africa—impress your kids with that fact tonight). This describes where we stand on the market right now—neutral with a slight upward bias, but with a nod toward the increased volatility we continue to expect.

We are entering a period that has traditionally been favorable for stocks on a seasonal basis (exiting the “sell in May and go away” six-month period); although the action this year has significantly bucked the traditional strength seen in the third year of the presidential cycle. We are also in the midst of earnings season, with the resilience of the market in the face of lackluster earnings reports being encouraging. Much of the blame for some of the weaker results has been focused on the recent strength in the US dollar as well as weak energy and commodity prices. But these latter concerns have also caused other areas of the economy to benefit, and post better earnings, such as the airline group. And with both energy prices and the dollar recently staging reversals, future quarters should be less negatively impacted, allowing investors to focus on overall demand, which remains fairly healthy.

Dollar stabilization should help corporate results

Source: FactSet, Intercontinental Exchange. As of Oct. 19, 2015.

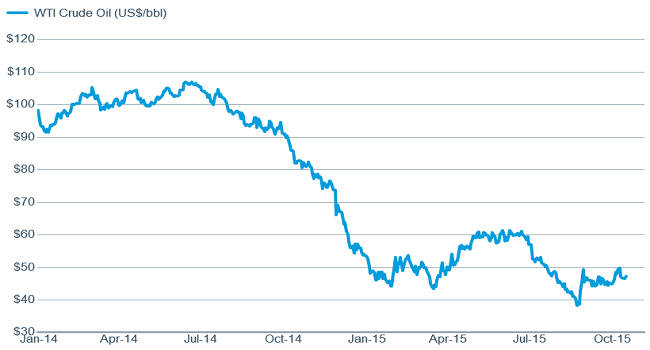

While flatter oil prices could contribute to better investor outlooks

Source: FactSet, Dow Jones & Co. As of Oct. 19, 2015.

Complicated economic outlook

The ability of companies to improve their earnings and revenues depends of course on the outlook for the economy. As noted, manufacturing has weakened notably, although not showing signs of escalating. Recent releases of regional manufacturing surveys, such as Empire (NY) and Philadelphia, have bounced a bit but remained in negative territory. Retail sales were also disappointing in September, with sales excluding autos and gas flat month-over-month. That said, real (inflation-adjusted) retail sales quarter-over-quarter were up 4.2%;, while nominal sales have increased at a 4.5% annual rate during the 2009-2015 expansion, exactly the same rate as during the 2001-2007 expansion. As such, fears of a dormant consumer may be overdone.

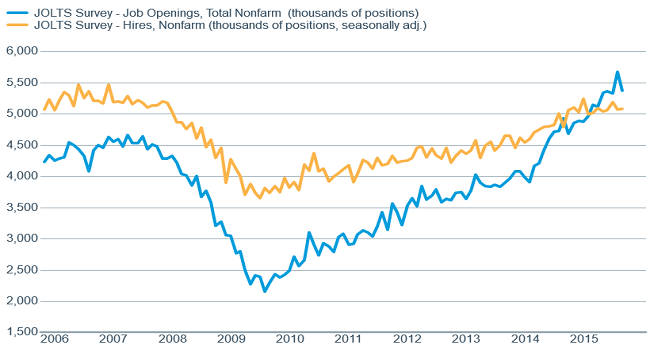

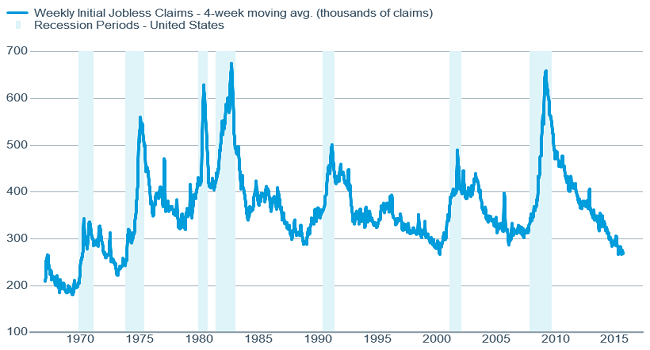

The lack of broad-based wage gains continues to confound however. Stories abound of industries, such as trucking, construction, pilots, air traffic control, etc., which can’t find qualified workers. The Job Opening and Labor Turnover Survey (JOLTS) indicates a tightening labor market, with job openings just off their cycle high and continuing to outpace the number of hires. Additionally, although a weaker-than-expected September jobs report raised concerns over the state of the labor market, the more forward-looking initial jobless claim reading recently hit the lowest level since 1973, with its four-week moving average at a 43-year low.

Job openings indicate a tightening labor market

Source: FactSet, U.S. Dept. of Labor. As of Oct. 19, 2015.

Forward looking jobless claims are at historic lows

Source: FactSet, U.S. Dept. of Labor. As of Oct. 19, 2015.

In another recent release, the National Federation of Independent Business (NFIB) notes that “quality of labor” is now the second-most frequent response to its question about companies’ “single most important problem.” It’s a concern which recently overtook “poor sales” which held the top spot from 2009-2013, but has been in a declining trend (“taxes” holds the top spot presently).

This all suggests wages should start to move higher, and that the relatively weak September jobs report should prove to be more of an outlier than the beginning of a deteriorating trend. That said, job gains should moderate over time, which is natural at this stage in the cycle. As unemployment falls from its current low 5.1% level, it becomes harder for companies to find available workers, so the pace of hiring will likely slow.

The Fed has backed itself into a corner

The mixed economic outlook had complicated the Fed’s decision about rates. At this point, futures contracts are indicating virtually no chance of a rate hike next week, while the chances for a December hike have decreased to roughly one in three. Although employment conditions—one of the Fed’s dual mandates—is signaling it’s time for liftoff, its inflation mandate is sending a more benign message. The latest core Producer Price Index (PPI) fell 0.3% month-over-month, although the core Consumer Price Index (CPI) did gain 0.2%, a bit more than expected. And core CPI is now 1.9% year-over-year—close to the Fed’s 2% target, but biased up by shelter costs. The Fed’s preferred Personal Consumption Expenditures (PCE) measure of inflation is more subdued.

Several Fed speakers have expressed their opinion that hikes should be off the table until well into 2016. That isn’t the view of all Fed officials, however, and that public disagreement has contributed to the ongoing uncertainly over the Fed and the likelihood of increased volatility in the stock market. But investors aren’t the only ones getting a bit frustrated with the Fed, as the Wall Street Journal reported that several central banks of other countries are urging the Fed to get on with it, hike rates, and end the uncertainty.

Unfortunately the Fed seems to have backed itself into a corner of sorts. For those with kids, do you talk about an upcoming shot for months ahead of time, explaining how it could hurt and that there may be other consequences, or do you just show up at the doctor and nonchalantly have the shot administered? We guarantee the way to avoid much drama and lingering uncertainty is the second.

It’s that time again, as Congress takes the debt ceiling debate down to the wire. We aren’t concerned about any long-lasting dire consequences, but investor nervousness could make for some shaky days in the market in the near term, while the contention over the ceiling doesn’t bode particularly well for the budget fight that faces a December 11 "deadline."

Has China landed?

In a different kind of disagreement, economists continue to debate whether China’s economy will have a so-called “hard” or “soft” landing—the difference between a sharp drop and a modest slowdown. But they may have failed to notice that China’s growth may have already landed.

China’s third quarter year-over-year gross domestic product (GDP) growth of 6.9% was the slowest since the financial crisis, prompting headlines of doom and gloom. However, China’s growth has picked up on a sequential basis. China’s third quarter measured on an annualized quarter-over-quarter basis, which is how we measure US GDP, was up 7.4%. That is the same pace as the second quarter and well above the 5.3% in the first quarter.

China's annualized third quarter GDP growth was near the five year average

Source: Charles Schwab, Bloomberg data as of 10/20/2015.

Why is China’s growth trajectory so important? China is the second largest economy in the world with the world’s largest middle class and acts as both a major source of demand and financing for other countries. A hard landing for China could mean weaker exports for other major countries and a race to devalue currencies as global trade contracts, and would increase the risk of a global recession. Fortunately, growth does not appear to be plunging despite the slower year-over-year GDP growth.

China’s GDP report, which is released less than three weeks after the end of the quarter, is suspect in its accuracy. That said, we don’t think any of the alternatives to the official data tell a dramatically different story. Other broad measures of growth in the economy such as the year-over-year growth of:

- 5.4% in tax revenue,

- 5.7% in industrial production,

- 5.8% in road freight traffic,

- 6.2% in service sector electricity use,

- 7.7% in disposable income per capita,

- 8.2% in floor space of new home sales,

- 10.9% in retail sales,

- 13.1% in the money supply, and

- 15.4% in total loan growth

all suggest that the official GDP growth rate isn’t greatly overstated, per data from Bloomberg.

Comments from companies are also important to gauging growth. Earth-moving equipment maker Caterpillar highlighted weak Chinese demand. On the other hand, apparel company Nike reported strong demand from China with sales up 30% year-over-year in the third quarter, up from 18% in the previous quarter. Which of these companies do we believe when it comes to China’s growth? Both of them, since slower government construction spending (which accounts for 9% of the Chinese economy) has weakened demand for construction equipment; while consumer spending (which accounts for nearly 40% of the Chinese economy) is a main driver of economic growth, per the Chinese National Statistics Bureau. It is not inconsistent to see weak construction equipment demand along with strong consumer spending, resulting in a balance of stable growth.

Economic stimulus applied to the Chinese economy in the third quarter included lower interest rates, a small devaluation in the yuan, along with tax incentives for car and home buyers. Stronger loan growth and acceleration in growth in the services sector lays the foundation for stable growth in the coming quarters. However, stabilization in growth can have a dark side if it ends up being driven by borrowing that is too rapid. It could undo reforms put in place in the past year or two to curb debt growth, which had soared from 125% of GDP to 200% from the end of 2008 through 2014. We will continue to watch these developments closely, but expect better global growth in 2016. For more insight see Global Economy to be Stronger in 2016.

What?

The large, lumbering hippo who can show surprising bursts of volatility accurately describes our view of the US and global stock markets at the present time, suggesting patience is necessary. Earnings season has been mixed-to-weak thus far, but stocks have held up relatively well, indicating optimism for the future. But until we have some clarity on Fed policy and the possible government shutdown, bouts of volatility are likely. China’s economy appears to be bouncing back at least modestly, which potentially bodes well for the global economy, and higher-risk asset classes.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

The S&P 500 Composite Index is a market capitalization-weighted index of 500 of the most widely-held U.S. companies in the industrial, transportation, utility, and financial sectors.

The IntercontinentalExchange (ICE) U.S. Dollar Index is an index of the of the United States dollar relative to a basket of foreign currencies, and is a weighted geometric mean of the dollar’s compared to the Euro (EUR), Japanese yen (JPY), Pound sterling (GBP), Canadian dollar (CAD), Swedish krona (SEK) and Swiss franc (CHF) relative to March 1973.

The Empire Manufacturing State Index is a regional, seasonally-adjusted index published by the Federal Reserve Bank of New York distributed to roughly 175 manufacturing executives and asks questions intended to gauge business conditions for New York manufacturers.

The Philadelphia Federal Index is an index that is published by the Philadelphia Federal Reserve Bank and is constructed from a survey of participants who voluntarily answer questions regarding the direction of change in their overall business activities. The survey is a measure of regional manufacturing growth.

The Job Openings and Labor Turnover Survey (JOLTS) ,conducted by the Bureau of Labor Statistics of the U.S. Department of Labor, involves the monthly collection, processing, and dissemination of job openings and labor turnover data. The data, collected from sampled establishments on a voluntary basis, include employment, job openings, hires, quits, layoffs and discharges, and other separations.

The Producer Price Index (PPI) is an index that measures the average change in selling prices received by domestic producers of goods and services.

The Consumer Price Index (CPI) is an index that measures the weighted average of prices of a basket of consumer goods and services, weighted according to their importance.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(1015-6592)