Key Points

- US equities have rallied sharply over the past month, inspired by soothing comments and actions from global central banks and signs that global growth is picking up. But with US corporate earnings negative in the third quarter and the manufacturing sector still sluggish at best, investors shouldn’t become complacent.

- Modest growth remains the story in the United States, with job growth and the services side of the economy healthy, but the manufacturing and energy sectors are taking it on the chin. The Federal Reserve has a December rate hike firmly on the table, while the US government came to a budget deal, taking some uncertainty out of the market.

- Global economic growth appears to be picking up and we believe there is an upside potential for European stocks in particular.

Investors’ “blankie”

Many readers either have a child or were a child who had some sort of comforting item they clung to—a teddy bear, a blanket, a pacifier, etc. Perhaps central banks are providing that comfort for markets. Over the past month we’ve seen the European Central Bank (ECB) announce it will likely expand its quantitative easing (QE) campaign in December; China reduce interest rates; and the Fed respond to a poor investor reaction to its September reading by removing concerns about global growth from the October statement. The result was a month that saw the major US indices gain over 8%, bringing them firmly back into the tight rate which characterized the year until the correction began in August.

Aside from the Fed, the fundamentals remain mixed for the US market. Third quarter earnings season is winding down, and while it’s yet again modestly better than expected, earnings are down for the second quarter in a row. According to First Call, coming into reporting season, earnings for the S&P 500 were expected to fall 4.2%, but estimates are now for a 2.8% decline. There were, however, pockets of strength—and outside of commodity-related industries there is not much concern about demand or the potential for a global recession. Looking ahead to 2016, analysts have lowered expectations—albeit to a still-positive 8.6% growth rate over 2015.

Murky economic picture

Although job growth remains healthy, wage growth has been anemic, which has provided cover for the Fed, although the most recent jobs report showed an uptick as average hourly earnings rose 2.5% year-over-year, which was the strongest reading since July 2009. Payrolls increased by 271,000 in October, with the unemployment rate ticking lower to 5.0%. At the same time, the more leading indicator of initial unemployment claims continues to hover near historic lows. Despite the strong October number, investors should note that as the employment market tightens it becomes more difficult to fill open positions. In fact, the second most-frequent response small businesses are giving when asked—by the National Federation of Independent Business (NFIB) in their monthly survey—what is their “single biggest problem” is “quality of labor.”

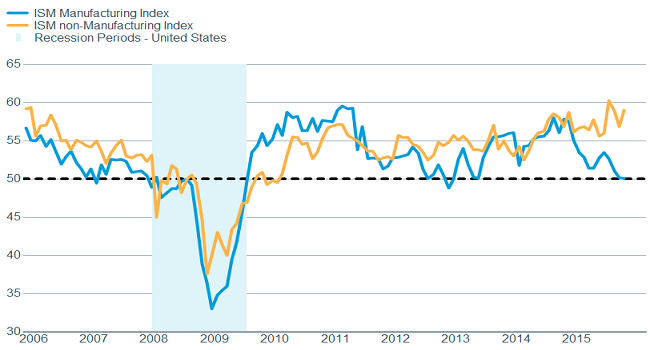

Unique in this economic cycle has been the wide divergence between the manufacturing and services sides of the US economy, illustrated nicely by the Institute of Supply Management’s (ISM) surveys.

Manufacturing and services still diverging

Source: FactSet, Institute for Supply Management. As of Nov. 4, 2015.

The question is will the manufacturing side drag the service side down, or will the strength in services drag manufacturing out of stagnation. Right now, we are betting on the latter, as services account for roughly 88% of the US economy, while the forces negatively impacting manufacturing have eased somewhat. The pace at which the US dollar has been strengthening has eased, and oil price declines have moderated. Strength in services was seen in the extremely robust October Non-Manufacturing ISM survey, which showed an overall index reading of 59.1, and a new order component booming at 62.0. Even within the weaker manufacturing ISM reading, its new order component also jumped. The new order components of the ISMs are leading in nature and bode well for potential future improvement.

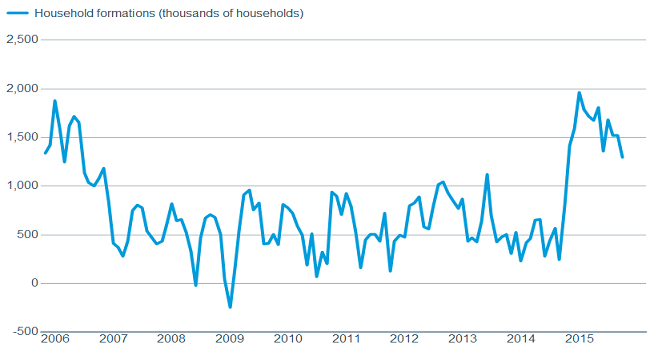

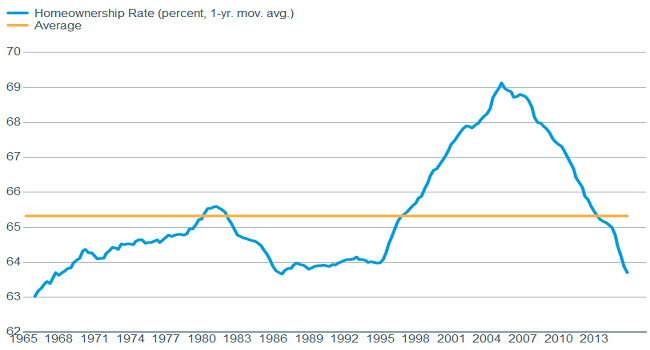

Housing data is another mixed bag. New home sales fell 11.5% in September, while pending home sales fell 2.3%; but longer-term trends are still healthy. The combination of still-low mortgage rates, a near 45-year low in the US homeownership rate , and an eight-year high in household formations, lead us to believe the September was a blip in a still-strengthening housing market.

Household formation supports stronger housing market

Source: Bloomberg. As of Nov. 4, 2015.

Homeownership should rise to meet long-term average

Source: FactSet, U.S. Census Bureau. As of Nov. 4, 2015.

So where does this amalgamation of data and information leave us. We think the pieces are still in place for what we’re calling the hippo market, characterized by plodding gains, with bouts of volatility. We are, however, entering a traditionally positive seasonal time for the market, so the historical bias is higher and the risk of a “melt-up” to end the year persists. That said, the strength in October might have “borrowed” some of the typical year-end gains.

Congress gets its act together and leaves stage open for Fed

Eliminating a prior pressure point on the market, Congress and the President came to a two-year budget agreement and also suspended the debt ceiling for the same time period. While there will still be fights about the details through the appropriation process, eliminating a major uncertainty was a welcome development.

Also welcomed by investors was the slightly hawkish tilt by the Fed noted in the statement accompanying the October Federal Open Market Committee (FOMC) meeting. Removed was the language referring to global growth concerns, and added was a more explicit reference to “the next meeting.” Although the Fed’s bias appears to be toward raising rates, and October’s payroll report boosted those odds even higher, the data over the next month will seal the fate of rates, but may bring some additional volatility with it.

October data encouraging

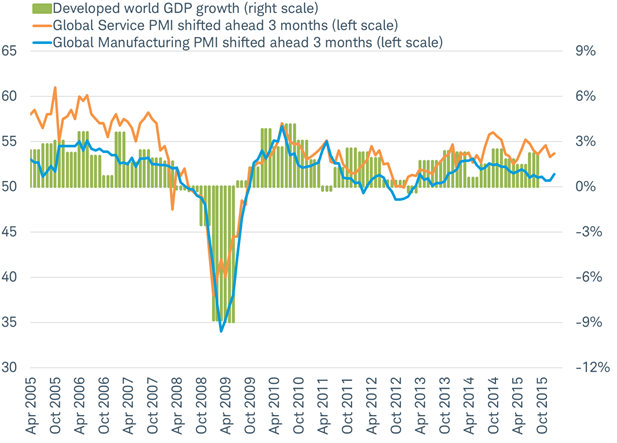

The US stock market rally and the Fed’s removal of specific concerns over global growth is at least partially a result of an international fourth quarter that seems to be off to a solid start. Fears that the global slump in manufacturing would drag down the much larger global services sector proved to be unfounded in October. The widely-watched global manufacturing purchasing managers index (PMI) rose from 50.7 in September to 51.4 in October—rising toward the level of the resilient global service sector PMI which rose from 53.3 to 53.7. The global manufacturing index was lifted by broad-based gains in Europe, Japan, and the United Kingdom.

The PMI suggests the world economy continues to grow at a steady pace. The PMI has tended to be a reasonably good indicator of future gross domestic product (GDP) growth. A further lift in the manufacturing index and continued solid service index readings would suggest stronger global growth may be on tap as we enter 2016; consistent with the International Monetary Fund (IMF) forecast for GDP in developed economies to accelerate from 2.0% in 2015 to 2.2% in 2016.

PMIs suggest world GDP continues to grow at a steady pace

Developed world GDP growth is the quarter over quarter annualized GDP for G7 countries as reported by the OECD.

Source: Charles Schwab, Organization for Economic Cooperation and Development, Bloomberg data as of 11/4/2015.

The PMIs for October reinforce our view that global growth is holding up better than market participants seemed to fear a month ago. In Europe, the composite PMI that includes both services and manufacturing increased to 53.9 from 53.6 in September, well above the 50-point mark that divides growth from recession. Historically, a Eurozone PMI composite reading of 53.9 is associated with annualized GDP growth of 2%, which is double the average pace of growth in that region during the past five years. In our view, this is a further sign that the Eurozone recovery remains on track. The increasing expectations for the ECB to step up the pace of QE program asset purchases is tied to weaker inflation readings, not weaker economic growth. The combination of solid growth, and the potential for greater central bank stimulus, is likely to result in a bullish combination for European stocks.

So What?

The sharp market gains seen over the last month are unlikely to persist at the same pace, and investors should be prepared for more volatility. Uncertainty about interest rates will persist, but the US economy continues to chug along at a decent, although not robust, pace. Similarly, global growth seems to be perking up, and helping to stymie predictions of an impending global recession. There are still pressures on global growth, but we believe the upside surprise potential in Europe should benefit stocks in that region. Investors who need to add to international exposure should look to do so consistent with their asset allocation goals.

(c) Charles Schwab