Questions for the New Year

Key Points

- 2015 was volatile, but ended with virtually no gain (or loss) for stocks. Wall Street analysts’ forecasts for 2016 are relatively muted, but the start of the year has been anything but. However, we caution against extrapolating the tough start to the rest of the year.

- 2016 begins with a bifurcated US economy and a Federal Reserve that is coming off of the first rate hike in a decade. How both of these issues evolve will likely heavily influence market performance.

- China has already had a volatile start to the year, and that seems likely to continue to be a story. But stabilization of the economy and manufacturing sector could help to stabilize both the Chinese and global markets.

Starting the year off with a bang

Happy New Year!? Few investors were sorry to see 2015 go, with its stomach-churning moves ultimately ending up with major indices close to where they started; but the start to 2016 has been decidedly worse. Multiple triple-digit down days on the Dow during the first week of trading likely unnerved investors. To that, we say, stay calm. The apparent catalysts for the selling—geopolitical and Chinese growth fears—haven’t greatly altered the overall picture to any great degree. Chinese economic data was in line with other releases noting that manufacturing is weakening, which is to be expected given their attempt to transition to a more services-oriented economy. Concerns about the continued devaluation of China’s currency as a signal of economic distress appear to be overdone. And the Middle East tension has had no impact on oil prices, while North Korea is economically nonexistent and even their one-time ally China condemned the move. But across asset classes, correlations have shot higher and greater global interconnectedness suggests ongoing bouts of volatility—extreme at times.

The S&P 500 Index closed 2015 down a scant 0.7%, but many stocks lost much more. The overall market was held up by good performance by a handful of extremely popular stock—a phenomenon known as narrowing breadth and often a troublesome sign for equities. No doubt, some of the selling seen to start the year can be attributed to some profit taking in some of those winners.

However, there is a glimmer of hope following the running to go nowhere action of 2015. Since 1970 there have been six “flat” years for the S&P 500 (-2% to +2%), and following those years, the Index returned between 11-34%, which if it holds true would be substantially better than most predictions on the Street. But geopolitical issues, some profit taking, and global growth concerns have contributed to a rough start. Despite this, we don’t believe the long-running bull market is ready to die just yet. As legendary investor John Templeton noted, “Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.” US equity markets seem a long way from euphoria, and much closer to skepticism. We anticipate further volatility and greater frequency of pullbacks; but barring an economic recession, we think a bear market will be avoided and that stock will ultimately break to the upside.

Economic questions

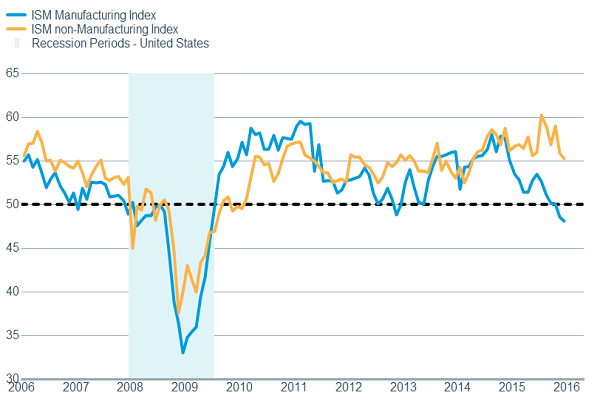

There are questions that have to be answered, however, before we can become more confident one way or the other. First, we have to ask whether the US economy will continue to be a bifurcated one, with manufacturing weakening while the service sector continues to grow, As the chart below shows, the two sectors of the economy typically don’t stay widely separated for very long.

It appears convergence should occur

Source: FactSet, Institute for Supply Management. As of 1/6/2016.

With the service sector making up roughly 88% of the U.S. economy according to HFE Research, the easy answer is that the manufacturing sector (the other 12%) will be dragged along. But the cautionary tale is that the manufacturing side of the economy in the past has been a leading indicator; so we do not have blinders on to the risk of a recession if services were to falter. But the consumer-oriented services sector does generally benefit from lower energy prices; while the hit to the energy sector would lessen if oil prices were to stabilize.

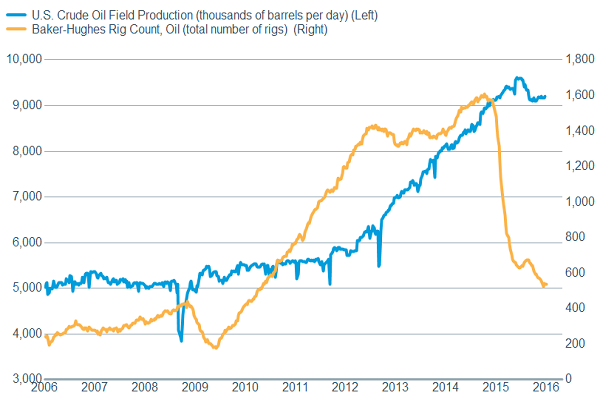

The rout in oil prices has forced energy companies into drastic decisions, including layoffs, dividend cuts, and capital expenditures being slashed. These actions should begin to have an impact on the severity of price declines as U.S. production is finally beginning to slow.

Oil companies’ reactions have been dramatic and are finally having an impact

Source: FactSet, U.S. Dept of Energy, Baker-Hughes, Inc. As of 1/5/2016.

We are not saying that oil prices are getting set to rebound—inventories are still elevated and production is still high, both here and globally—but we believe the rapid and dramatic declines are in the rearview mirror.

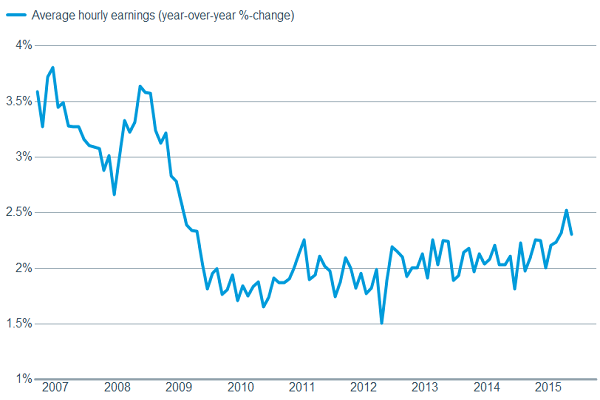

Oil developments lead us to the other major question that should impact the service economy—the American consumer. Lower oil prices have not had the positive impact on consumers that might have been expected given past tendencies, as consumers have saved and paid down debt rather than just spend on discretionary purchases. But we believe those energy savings will start to filter through to spending in an increasing manner. Mastercard reported that spending, ex-autos and gas, between Black Friday and Christmas Eve was up a robust 7.9%. Additionally, with the unemployment rate at 5.0% and another 292,000 jobs added in December, long stagnant wages are beginning to accelerate.

Wages showing signs of rising…finally!

Source: FactSet, U.S. Dept. of Labor. As of 1/5/2016.

Consumer incomes also have the tailwind of minimum wages being increased in many cities and states; while the November National Federation of Independent Businesses (NFIB) survey noted that a historically- strong 20% of respondents plan to raise compensation for their workers. We believe this combination could lead to upside surprises from consumer spending, helping to support the service side of the economy, and help offset the drag from the manufacturing sector.

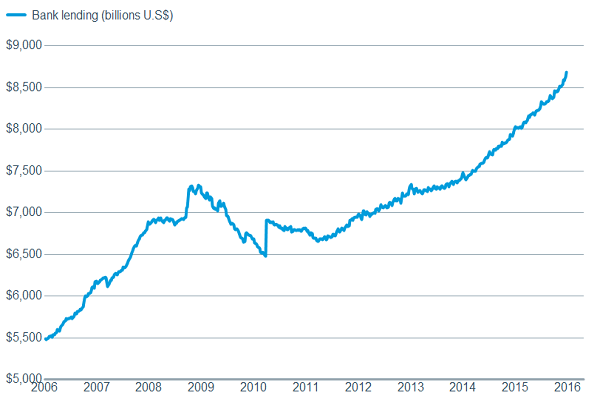

It’s not just the consumer that needs to come through; as business confidence and spending need to rise as well. Bank loans have moved higher, which is typically a good indicator, but it appears companies have been reluctant to spend those funds on capital improvements.

Positively—bank loans have moved higher

Source: FactSet, Federal Reserve. As of 1/5/2016.

Again according the NFIB, 25% of their respondents plan capital outlays in the next three-to-six months, below the long-term average of 29%. And The Wall Street Journal reports that S&P released information that capital expenditures for S&P 500 companies fell in the second and third quarters of 2015—the first consecutive quarterly falls since 2010. Part of the reason for lackluster business spending on capital may have been the robust merger and acquisition (M&A) market seen in 2015. According to Dealogic, 2015 saw a record high $4.7 trillion in deals announced; while 63 of them were valued at more than $10 billion, blowing away the previous high of 43 in 2006. While there are myriad reasons behind deals, ultimately the majority of them should result in capacity being reduced, expenses being pared, inefficiencies being reduced; and as a consequence, ultimately earnings enhanced.

Government help? Fed path?

It’s not all bad news in Washington. With the budget deal passed, there is some measure of certainty around fiscal policy, which should help corporate planners. In addition, the extension of several tax credits and beneficial depreciation rules should provide incentive for companies to act. Of course, reducing the corporate tax rate along with tax reform that resulted in a far simpler structure, in our opinion, would provide an exponentially greater benefit to businesses, but in a super-heated election year, that seems highly unlikely to occur.

Down the street, the shoe finally dropped and the Fed raised interest rates by a quarter point in December. Of course, hope that Fed uncertainty would dissipate was dashed by the immediate wondering of when the next action will occur and what the ultimate path will look like. For now we believe the Fed will be cautious and slow to raise rates, and with inflation low they presently have the option to do so. Historically, a slow tightening cycle was significantly more rewarding to equity investors than a cycle during which the Fed has to act more forcefully.

Will the global economy surprise in 2016?

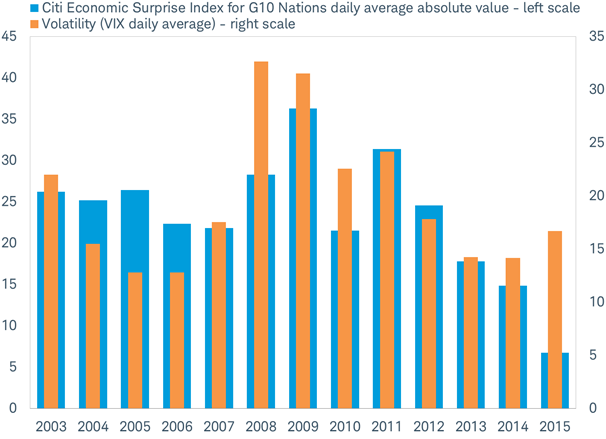

Global factors will also likely play into the Fed’s decisions this year. Last year was the lowest for economic surprises in over a decade, as economic data was relatively close to economists’ forecasts throughout the year. Economic data surprises may stay low in 2016 with no major countries likely to slip into recession and global gross domestic product (GDP) growth close to the long-term average of 3.5%.

While economic surprises were low in 2015, stock market volatility was not, as you can see in the chart below. Higher volatility in 2015 was driven by a range of fears including: Greece potentially leaving the Eurozone, geopolitical conflicts in Ukraine and Syria, the pace of China’s economic slowdown, the impact of the commodity price crash, among many others. But economic growth came in close to expectations despite these concerns.

Again in 2016, global stock markets are likely to be driven more by drama than data. For example, geopolitical concerns contributed to the drop in the first week of trading in 2016.

Economic surprises were low in 2015, but stock market volatility was not

Source: Charles Schwab, Factset and Bloomberg data as of 1/5/2016.

Will China make or break 2016?

Worries over China’s pace of growth and currency movements set the first day of trading in 2016 off on a negative note for stock markets around the world. The world had to absorb a drop in demand from China in 2015. But efforts to stabilize China’s ailing manufacturing sector put in place in the second half of the year appear to have born some fruit:

- The pace of China’s industrial output has moved back up to a 6.2% year-over-year growth rate, as of the latest reading from November per China’s National Bureau of Statistics.

- Industrial profits have mostly rebounded from a year-over-year loss of -9% in August to a loss of just -1% in November 2015.

- The Caixin China manufacturing purchasing managers’ index slipped in December, but remains well off of the September lows.

The efforts to boost manufacturing have included currency devaluation, interest rate cuts, reserve requirement cuts, tax cuts, and a slower pace of reform implementation.

The relative stabilization that may take place in China's manufacturing sector in 2016 could help global growth and boost confidence that a crash in China’s economy will not follow the crash in China’s mainland stock market seen in mid-2015, and resurrected in early-2016. Nevertheless, the uneven economic data points amidst an overall deceleration in growth for China are likely to contribute to volatility in 2016—as seen already in the year.

So what?

We continue to believe that U.S. and global stocks will continue to experience bouts of volatility and pullbacks; but a major bear market is likely to be avoided. Key determinants of the path stocks will take include central bank policy, inflation, currency volatility and earnings/valuation. We continue to reinforce the benefits of broad and global asset class diversification during a more difficult market environment.

(c) Charles Schwab