Schwab Market Perspective: Neutral Does Not Mean Boring

Key Points

- The sharp downward move by stocks to start the year has abated, but volatility is likely to persist. We believe the bulls will ultimately win the tug-of-war, but risks are elevated.

- The roller coaster ride in stocks is reflected in the mixed readings among recent economic releases. This, combined with signs some inflation has re-emerged, complicates the Fed’s upcoming decisions on rates and adds to uncertainty.

- Global stocks have joined in on the wild ride, with some comforting words from China aiding the rebound; but the upcoming European Central Bank decision could ignite further volatility.

Neutral, but not boring!

There are two ways to get to a neutral color: 1) just pick the boring beige that we’re all familiar with, or 2) mix a bunch of wild colors together and end up with an altogether bland sort of color—vastly different inputs but relatively the same result. Recently, stocks have resembled the latter scenario as stock indexes have moved out of correction territory but have remained quite volatile, with triple-digit Dow moves more common than not. This illustrates why we continue to recommend that investors have a neutral allocation toward equities in their portfolio. Uncertainty remains elevated and trying to chase, or even interpret, every move in the stock market seems to us to be a losing game.

Our view is akin to dating vs. marrying. A lot of the action recently has been from folks that are simply “dating” stocks—no long-term commitment, trying different things out, never settling on a set path—exciting at times but ultimately mostly exhausting and unsatisfying. We suggest investors take an approach more like marriage—a long-term, stable commitment, sticking with the plan through ups and downs, knowing there will be good times and bad, but hopefully ultimately fulfilling in the long term.

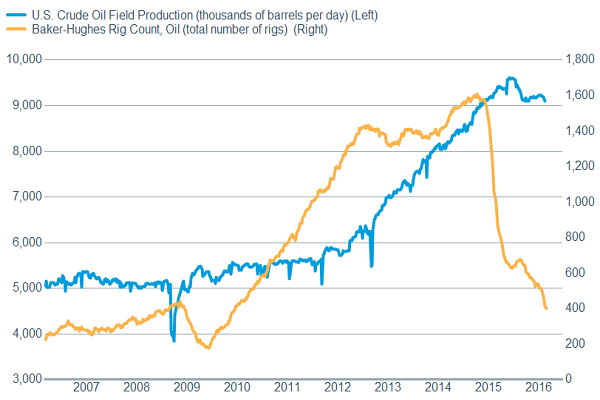

Stocks continue to be heavily influenced by oil, and not in the traditional way. When oil has risen, so have stocks. So, the price of oil having stabilized and moving higher has helped stocks to do the same. If a near-term bottom for oil is in, it’s likely to continue to bode well for stocks. U.S. production has declined recently, finally responding to the drop in rig count.

US oil production responding to drop in rig count

Source: FactSet, U.S. Dept of Energy, Baker-Hughes, Inc. As of Mar. 1, 2016.

And pressure is building on overseas producers such as Russia, Iran, Saudi Arabia, etc. as they are running into budget problems due to the crash in oil prices. No agreement to cut production has been reached at this point, but they are at least talking to each other about different potential actions to try to boost the price of oil. Remember the basic rule of economics—the cure for low prices is low prices, as it eventually cuts supply and increases demand. And don’t forget that historically a reduction in the price of oil has been a boost to the economy with about a year lag. We believe we will see that boost to a greater extent as we go through the year.

Domestic economic picture muddled, and concerning

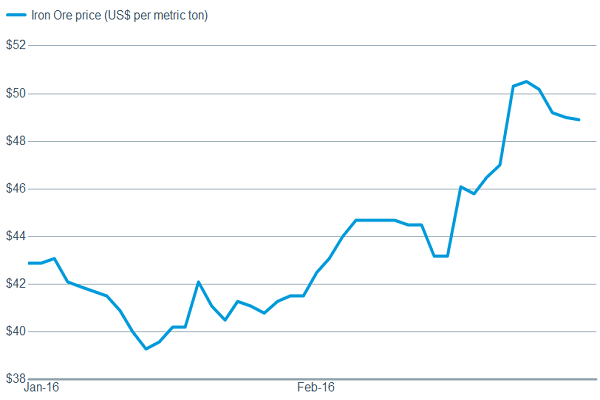

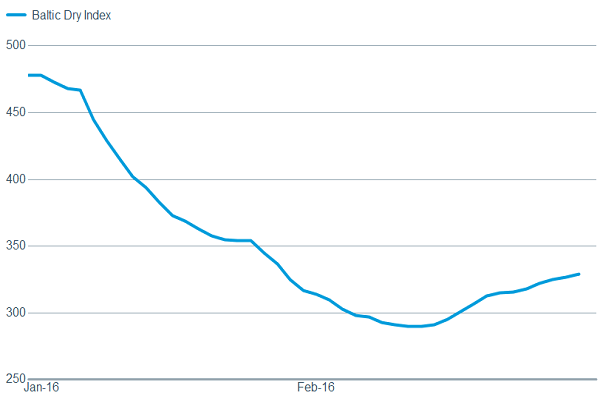

But oil isn’t the only factor impacting stocks. Investors are also trying to get a handle on domestic economic growth vs. the risk of a recession. We remain in the no recession camp, but the data remains mixed. For example, existing home sales rose 0.4% month-over-month, while new home sales (which are a much smaller portion of the market) fell 9.2%. The manufacturing vs. service picture is mixed as well, with manufacturing remaining relatively weak, but improving on some metrics. Both the latest Empire and Philadelphia regional surveys moved higher; although remaining in negative territory. And the national Institute of Supply Management’s (ISM) Manufacturing Index posted a surprising rise to 49.5 from 48.5; while the forward-looking new orders component stayed at a decent 51.5. Additionally, we’ve seen bounces in iron ore prices, the Baltic Dry Index (measuring global shipping price trends), and the general commodities complex—providing some evidence that the downward trend in manufacturing may be ending.

Inflection point for manufacturing?

Source: FactSet, Commodity Research Bureau. As of Mar. 1, 2016. China import Iron Ore Fines 62% FE spot.

Source: FactSet, Commodity Research Bureau. As of Mar. 1, 2016.

Source: FactSet, Baltic Exchange. As of Mar. 1, 2016.

Supporting the more optimistic view, we received a nice surprise from the durable goods report, which followed a solid industrial production gain of 0.9%. Orders for non-defense capital goods ex-aircraft, considered a proxy for business spending, rose a robust 3.9% month-over-month, while the previous month’s decline was revised slightly higher.

But the much larger service side of the economy is becoming more murky. Markit’s Flash US Services PMI fell below the 50 mark that delineates contraction and expansion; however Markit noted that much of the weakness was attributed to the massive snowstorm in the northeast. The ISM Non-Manufacturing (Services) Index remains in territory depicting expansion, although it ticked very slightly lower to 53.4 from 53.5; with a similar story for the orders component, which is leading, and remains in expansionary territory at 55.5.

Finally, the labor market continues to look quite solid. Initial unemployment claims—a leading economic indicator—show no signs of increasing; while the February jobs report showed that 242,000 jobs were added in February while the unemployment rate was 4.9%. The tight labor market means that future gains may be more muted, as there are fewer folks to hire, while also pressuring wages higher.

Feds’s job getting harder

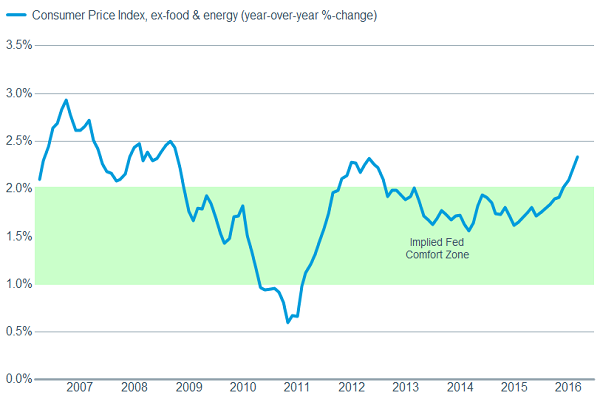

This conglomeration of striking colors mixing into a neutral picture puts the Fed in a bit of a pickle. The Federal Open Market Committee (FOMC) is still biased toward normalizing monetary policy, but the uncertainty in the U.S. economy, combined with volatility in financial markets and foreign central banks easing, means rates will likely not be increased at the March meeting. But the market may be underestimating the chances of further hikes this year, especially given the latest uptick in inflation. The Consumer Price Index (CPI) reading, ex-food and energy (the “core” rate), posted a surprising 2.2% gain year-over-year—not robust but the highest since June 2012. And the Fed’s “preferred” measure of inflation—Personal Consumption Expenditures (PCE)—has also ticked higher, with the core rate at 1.7%. Remember, the Fed’s target rate for inflation is 2.0%.

Prices starting to move higher?

Source: FactSet, U.S. Dept. of Labor. As of Mar. 1, 2016.

Sustaining the turnaround

The roller coaster ride isn’t only contained to the United States, as although February marked the fourth consecutive month of losses for global stocks, the MSCI All Country World Index (ACWI) has recovered more than 7% since this year’s low point of February 11. The 30% rebound in oil prices may have also improved global investor sentiment about the outlook for growth and corporate earnings. Fears abated further on some clarification from Chinese policymakers on their intentions, and indications that global central banks are revising their policies to sustain growth while limiting the negative impact on banks.

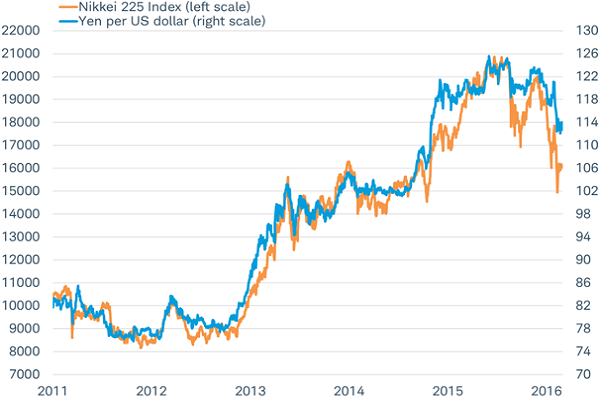

After months of confusion among market participants, Chinese leaders clarified their policy stance at the G20 meetings in Shanghai last week. Most importantly, senior policymakers emphasized stability in growth and the currency; easing fears of recession and devaluation. While stability in China benefits global growth, the country with the most to gain may be Japan. Policymakers in Japan have been struggling to keep its currency from strengthening and deflation from reemerging. As you can see in the chart below, Japan’s stock market has been tracking the strength in the yen (a strengthening yen means a falling blue line in the chart since fewer yen per dollar means a stronger yen). A relatively stable, rather than rapidly depreciating, Chinese currency may be a relief to Japanese policymakers and free the Bank of Japan (BoJ) from further negative interest rate policy moves. It may also help the yen to halt its rise and sustain the rally in the Nikkei.

Japan’s stock market may benefit from a reversal in the yen

Source: Charles Schwab, Factset data as of 3/1/2016.

In Europe, economic activity has expanded for 32 straight months, measured by the Eurozone composite purchasing managers’ index (PMI). Yet, growth momentum appears to have faded in the first quarter of 2016 from the prior quarter when it reached the strongest level in over four years. The fading growth momentum has prompted stock market participants to consider what actions the European Central Bank (ECB) may take at its next meeting to support growth.

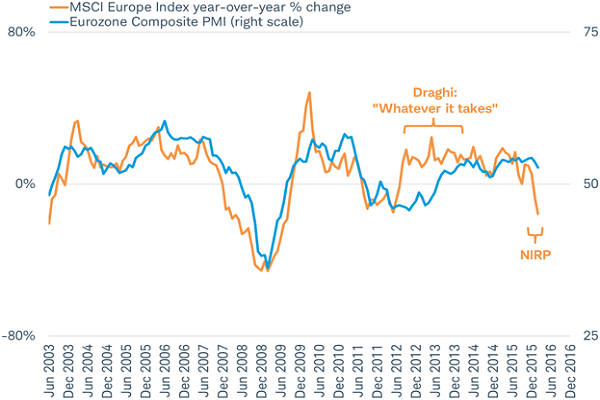

The performance of Europe’s stock market typically tracks economic activity reflected in the Eurozone composite PMI; but stocks jumped above the trend in the economy after ECB president Mario Draghi made his “whatever it takes” pledge to preserve the euro in mid-2012, as you can see in the chart below. More recently, the ECB cut a key policy rate to -0.3% on December 3, 2015 as part of its negative interest rate policy (NIRP). This had the opposite effect relative to the “whatever it takes” pledge and weighed on stocks; particularly those in the financial sector, as stocks decoupled from the economic trend. For more insight see: Negative Interest Rate Policy Adds Up To Less than Zero for Investors.

ECB’s negative interest rate policy may be weighing on stocks rather than stimulating growth

Source: Charles Schwab, Bloomberg data as of 3/1/2016.

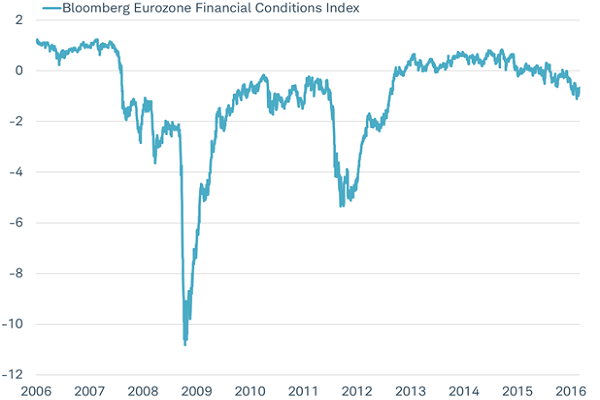

The December 2015 ECB meeting helped to worsen the Bloomberg Eurozone Financial Conditions index, as you can see in the chart below. While financial conditions in Europe remain far from the crisis levels of 2008-09, or even 2012-13, we will be watching the influence the ECB is having on financial conditions closely in the coming weeks for indications on where stocks in Europe may be headed.

ECB must avoid worsening financial conditions in the Eurozone

Source: Charles Schwab, Bloomberg data as of 3/1/2016.

The next ECB meeting on March 10 comes nearly a month after European stocks bottomed on February 11. From that low point through March 1, the MSCI Europe Index has rebounded 12%. After leading to the downside for much of this year, the financial sector has helped lead the way, along with the beaten down energy and materials sectors. The ECB needs to avoid actions that may undermine the financial sector to help sustain the stock market rally. For the upcoming March 10 meeting, investors may want to watch for several key developments that could help determine the direction for Europe’s stock market:

- A cut to the key rate on banks’ deposits at the ECB to -0.4% is priced into futures markets, but a bigger cut may be viewed negatively by investors since it may raise banks’ costs.

- An introduction of a tiered system to shield some of banks’ deposits from the cost of negative interest rates would likely be viewed as a positive by the stock market.

- Any expansion of the ECB’s quantitative easing (QE) asset purchase program from the current monthly pace of 60 billion euros may be welcomed by market participants.

So what?

Economic uncertainty has contributed to heightened volatility across U.S. and global asset classes. We remain optimistic that the United States is not headed into a recession, which should keep the correction from becoming a bear market. We continue to recommend a neutral allocation to U.S. equities and acknowledge that risks are elevated but urge investors to remain disciplined around their investment plan . The neutral rating holds true for international equities, too, as we’ve seen rebounds in major global markets in the past few week, but volatility is likely to persist.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The Empire Manufacturing State Index is a regional, seasonally-adjusted index published by the Federal Reserve Bank of New York distributed to roughly 175 manufacturing executives and asks questions intended to gauge business conditions for New York manufacturers.

The Philadelphia Federal Index is an index that is published by the Philadelphia Federal Reserve Bank and is constructed from a survey of participants who voluntarily answer questions regarding the direction of change in their overall business activities. The survey is a measure of regional manufacturing growth.

The Institute for Supply Management (ISM) ManufacturingIndex is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Baltic Dry Index is shipping and trade index created by the London-based Baltic Exchange that measures changes in the cost to transport raw materials such as metals, grains and fossil fuels by sea.

The CRB BLS Spot Market Price Index tracks 22 commodities presumed to be among the first influenced by changes in economic conditions

Markit’s Flash US Services PMI is an early estimate of the Services Purchasing Managers' Index (PMI) for a country, designed to provide an accurate advance indication of the final Services PMI data.

The Institute for Supply Management (ISM) Non-manufacturingIndex is an index based on surveys of more than 400 non-manufacturing firms by the Institute of Supply Management. The ISM Non-manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Consumer Price Index (CPI) is an index that measures the weighted average of prices of a basket of consumer goods and services, weighted according to their importance.

The core PCE Price Index is personal consumption expenditures (PCE) prices excluding food and energy prices. The core PCE price index measures the prices paid by consumers for goods and services without the volatility caused by movements in food and energy prices to reveal underlying inflation trends.

MSCI ACWI (All Country World Index) is A market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world. The MSCI ACWI is maintained by Morgan Stanley Capital International, and is comprised of stocks from both developed and emerging markets.

The Japan Nikkei 225 Index is a price-weighted index comprised of Japan's top 225 blue-chip companies on the Tokyo Stock Exchange.

The Markit Eurozone PMI Composite Index tracks business trends across both the manufacturing and service sectors, based on data collected from a representative panel of over 5,000 companies (60 percent from the manufacturing sector and 40 percent from the services sector). The index tracks variables such as sales, new orders, employment, inventories and prices.

The MSCI Europe Index captures large and mid cap representation across 15 Developed countries in Europe. With 448 constituents, the index covers approximately 85% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

The Bloomberg Eurozone Financial Conditions Index is an overall guage of the health of the financial and credit markets.

The Job Openings and Labor Turnover Survey (JOLTS), conducted by the Bureau of Labor Statistics of the U.S. Department of Labor, involves the monthly collection, processing, and dissemination of job openings and labor turnover data. The data, collected from sampled establishments on a voluntary basis, include employment, job openings, hires, quits, layoffs and discharges, and other separations.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0316-DBM5)