Investors worried about locking up their capital for too long in private-credit investments may be missing the big picture: the higher-yielding cash flow they receive via private-credit distributions is, in fact, a form of liquidity.

The script isn’t new. Low yields have investors of all sizes in search of higher-returning investments. But core strategies that root much of a portfolio in stable, mostly investment-grade publicly issued securities just don’t cut it for many investors looking to enhance returns.

Potential-return enhancement is why core-plus strategies came into existence. Yet a persistent low-yield environment has some investors shifting portions of their capital into focused mandates that can invest in private credit.

Private-credit investments generally offer more yield in exchange for less liquidity. But what does less liquidity actually entail? Investors may be surprised by the answer.

CASH FLOW AS LIQUIDITY

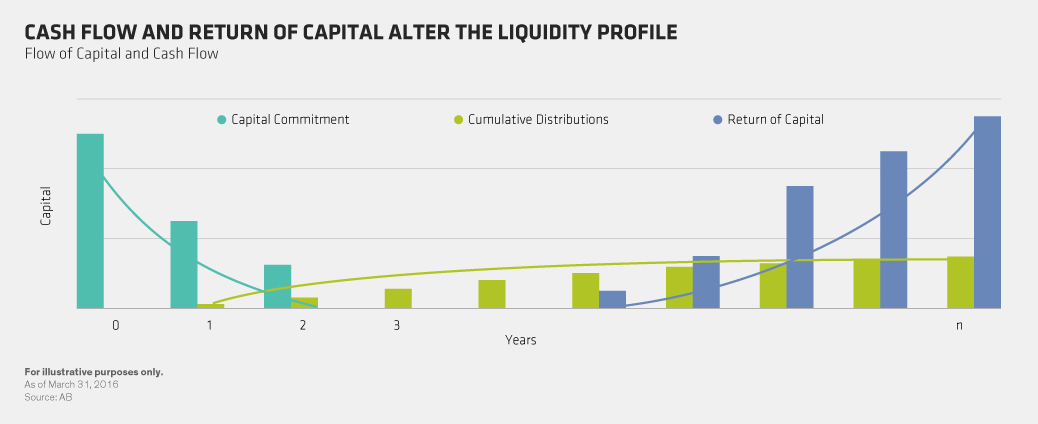

Investors who like the idea of having access to their capital at any given time may be deterred by the perceived illiquidity of private-credit strategies, which can include investments in commercial real estate debt, middle-market lending, residential mortgages and infrastructure debt (e.g., toll roads and bridges). While most private-credit investments are offered in fund form with a legal life of seven, eight or more years, depending on the strategy, when the cash flows are viewed in their various components, the liquidity profile is much more fluid and the weighted average life is much shorter.

Typically, private-credit strategies can invest in funds that consist of an initial investment period followed by a harvest period. Investors commit capital, which is drawn down and invested over an extended period of time. Meanwhile, interest income is often paid out quarterly, creating cash flow and liquidity for the private-credit investor.

Following the end of the investment period, as investments repay and prepay, principal is returned to investors well before the strategy’s end date. When drawdowns are combined with interest distributions and return of capital, the result is a much more fluid cash-flow investment.

Given the multiple factors in play, a weighted-average life calculation, as shown in the Display below, offers investors a better sense of the underlying liquidity of the strategy.

We believe that institutional investors with the capital and the time necessary for a private-credit strategy to unfold have a compelling investment option available in today’s market. Private credit offers the potential for higher yields, and when cash flow is factored in, the liquidity is actually “wetter” than expected.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.