Get Ready for the End of the Summer Slumber

Key Points

- Stocks have largely moved sideways over the past month with muted volatility and depressed volume. In our view, action is likely to heat up, with the threat of a near-term pullback within an ongoing bull market.

- U.S. economic data has perked up, but we need to see consistently better data to confirm a sustainable lift in growth beyond the third quarter. The Federal Reserve is indicating a desire to raise rates, but Friday’s slightly weaker-than-expected jobs report suggests a September hike is less likely.

- Attitudinal measures of investor sentiment—which is generally a contrarian indicator—have moved back into optimistic territory; however behavioral measures—like fund flows—show a still-skeptical individual investor class.

Back at it

You may have been lulled to sleep by the market action (or inaction) over the past month; but likely thrilled if you were able to take an uninterrupted vacation. The S&P 500 is largely flat through the month of August and volatility has been historically low; while trading volume has been depressed (read more in Liz Ann’s article All Summer Long). That appears to be about to end as traders, investors and policymakers return to work and investors should be prepared. Complacency can be dangerous if investors allow their emotions to take control of their portfolio allocations during an uptick in volatility. With investor optimism reaching elevated levels according to a recent NDR Crowd Sentiment Poll, a near-term pullback is possible. We would view such an event as an opportunity to add to positions as needed, and likely a beneficial dip within the context of longer-term bull market. It does appear that the heavy outflows out of equity mutual funds and exchange-traded funds (ETFs) are slowing. ISI Evercore Research reported that outflows over the past year have totaled $115 billion—high, but down from the highest levels we saw earlier this year of $160 billion—an improving trend that could provide support for stocks.

Economic data perks up

The U.S. economy should support a continuing upward stock market trend. Although the second quarter real gross domestic product (GDP) number was quite weak, much of that was held down by a reduction in inventories, which should help growth this quarter as inventories are rebuilt. According to ISI Evercore, over the past five years real inventory accumulation has slowed by $127 billion. The last five times there was significant slowing in inventory accumulation real GDP growth rose by an average of 4.3% in the following year. We aren’t predicting a surge to that level of growth, but a replenishment of inventories could provide a tailwind to near-term growth.

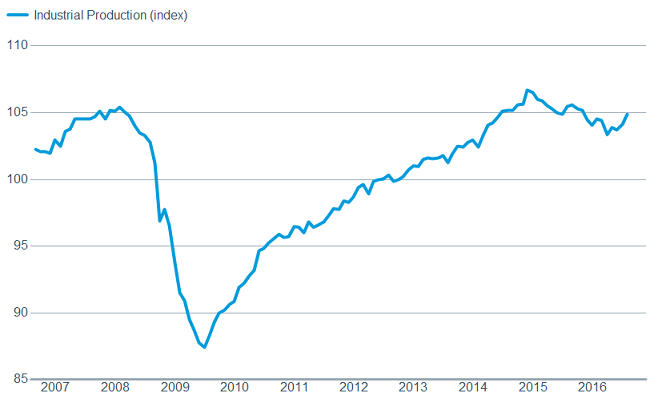

In the meantime, we have seen some signs that manufacturing may be breaking out of its malaise. The hit from the drop in oil-related investments may be coming to an end as the price of oil has stabilized (for now) in the $40-50 dollar range; while the rig count has turned back up.

Stabilizing oil prices could help manufacturing

Source: FactSet, Dow Jones & Co. As of Aug. 25, 2016.

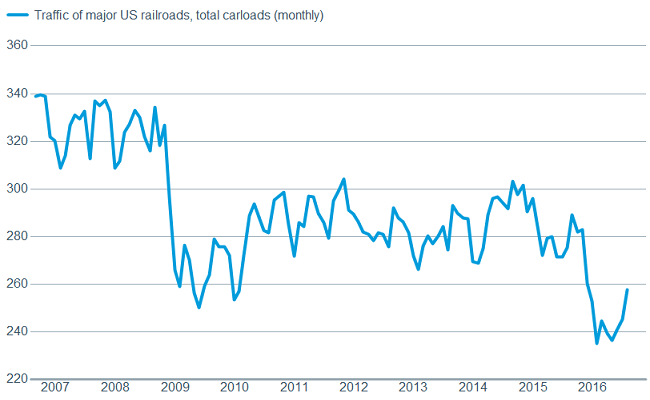

Additionally, the U.S. dollar, in contrast to many predictions following the Brexit vote, continues to trade below its 2015 highs, which has made U.S. goods more attractive to foreign buyers. However, the dollar has rallied a bit recently, so the tailwind may be limited. Railcar loading have also picked up a bit, the latest durable goods orders report was quite a bit better than expectations, and housing data continues to be encouraging.

A decline in the dollar

Source: FactSet, Intercontinental Exchange. As of Aug. 25, 2016.

And a pickup in railcar loadings

Source: FactSet, Association of American Railroads. As of Aug. 25, 2016.

Could mean a continued upturn in manufacturing

Source: FactSet, Federal Reserve. As of Aug. 25, 2016.

The continued improvement in housing illustrates the healthier U.S. consumer and could start to help certain areas of the manufacturing sector. Existing home sales actually fell 3.2% in July, which seems to contradict the idea of an improving housing market; but the National Association of Realtors, which puts out the number, made sure to note the weakness wasn’t due to lack of demand, but rather a dearth of supply. In contrast, new home sales jumped 12.4% and moved to their highest level since October 2007.

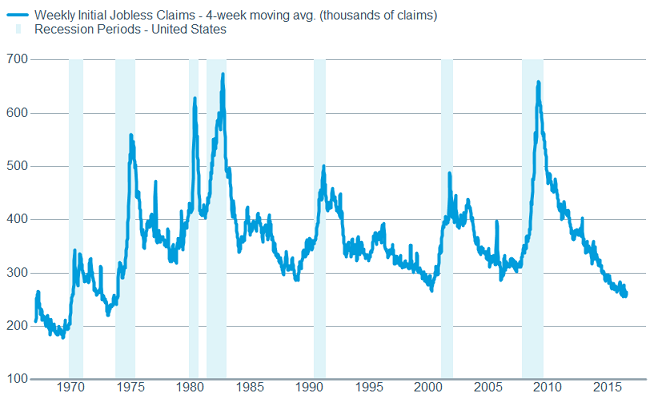

A healthy U.S. consumer is vital to growth, and along with housing we continue to see signs of an improving picture in the labor market. The unemployment rate is a low 4.9% as 151,000 jobs were added in August according to the Department of Labor—slightly weaker than expected but still solid, and the forward-looking jobless claims number continues to trend near historically low levels. A tighter job market should continue to help pressure wages higher, which we’ve started to see, helping to increase the amount of disposable income available to consumers.

Jobless claims indicate continuing healthy job market

Source: FactSet, U.S. Dept. of Labor. As of Aug. 25, 2016.

Fed focus continues

One thing that didn’t take a hiatus in August was the incessant dissection of every utterance from a Federal Reserve member. For those hoping for clarity, we surmise they were sorely disappointed. Various members offered conflicting views, and in one case the same member seemed to offer differing opinions in the same week about whether another rate hike is forthcoming. It may say something that there’s so much handwringing over a potential 25 basis point increase. If the U.S. economy can’t handle a 0.50% fed funds rate, we may be in more trouble than we think. Regardless, Fed Chairwoman Janet Yellen did sound a bit more hawkish in her comments from Jackson Hole, but Vice-Chairman Fischer seemed to steal the show when he mentioned the possibility of two rate hikes this year. We believe the momentum for at least one hike seems to be gaining ground.

Are investors about to start buying stocks again?

We are sympathetic to the Fed, however, as consistently predicting what markets and economies will do is hard, if not impossible. Predicting investor behavior, on the other hand, can be surprisingly simple. Without the aid of advice, investors often tend to chase returns. Decades of behavioral research suggest investors sell one investment to buy another that has performed better in the hope that the outperformance will continue.

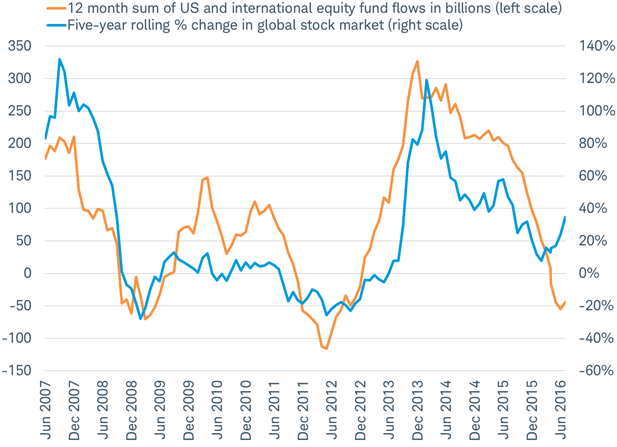

Although this behavior is very common, exactly which timeframe of returns investors chase is less discussed. Do investors chase returns over a month? A year? Actually, it appears that the rolling five-year return has most closely mirrored investors’ buying and selling of equity mutual funds and ETFs, as you can see in the chart below.

Chasing returns: investors buying and selling tends to correlate to five-year returns

Source: Charles Schwab, Investment Company Institute, Bloomberg. Data as of 8/31/2016.

The five-year rolling return for the global stock market has been weakening in recent years, measured by the MSCI AC World Index. In fact, even as recently as the end of January 2016, the five-year return was only 8%, a less than 2% annualized return—hardly enough to compensate investors for the volatility they experienced. In step with the weakening performance, investors have been decreasing their net buying of equities in recent years and turned to net selling in recent months in order to buy bond funds, according to data from the Investment Company Institute (ICI).

The trend now appears to be changing. In the past few months, the five-year return has rebounded back into the double digits—reflecting not only a strong recent trend in the stock market, but also the dropping out of the summer 2011 declines, when the U.S. debt ceiling debacle triggered a brief bear market. The global stock market’s total return over the past five years rose to 35% as of the end of August 2016 as measured by the MSCI AC World Index. If stocks maintain their current level through year-end, the five-year rolling return would maintain those gains and even rise a little further to 40%.

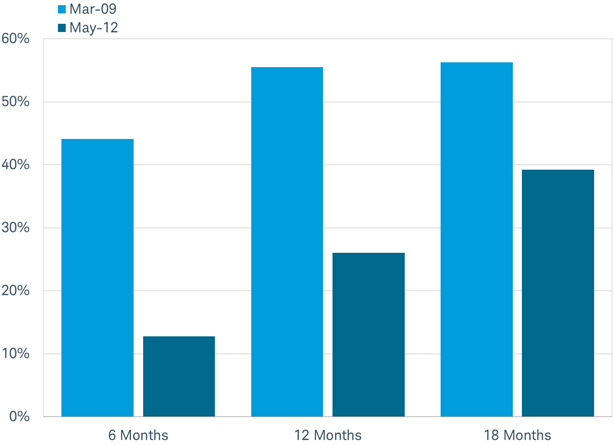

The rebound in performance could mean investors may start buying stocks again. A second wind for the rally, fueled by individual investors’ buying, may be just what the stock market needs following years of corporate buying through share buybacks and cash acquisitions. The last two times the trend of investor selling turned around—in March 2009 and May 2012—global stocks delivered strong double-digit gains over the next 6-18 months, as you can see in the chart below.

Strong total returns for global stocks in periods following turnarounds in investor selling

Returns based on MSCI AC World Index. Past performance is no guarantee of future results.

Source: Charles Schwab, Bloomberg data as of 8/31/2016.

While this may sound like an opportunity to ride a wave of buying, it doesn’t mean smooth sailing for global stock markets. At the start of those two prior periods, stocks were coming off a global bear market; but as of the end of August 2016 stocks tracked by the MSCI AC World Index are near all-time highs. Also, in the near-term, September and October have a reputation for stock market volatility and there are plenty of catalysts to consider. They include: potential surprises in economic data; outcomes of the Federal Reserve and Bank of Japan central bank meetings; political polling ahead of the Italian constitutional referendum, and of course the U.S. presidential election; as well as the third quarter earnings pre-announcement and reporting season. Rather than jumping in and out of global stock markets to chase returns, investors would be wise to remain committed to their long-term equity asset allocations.

So what?

Volatility is likely to pick up and investors should consider using volatility to tactically rebalance around longer-term strategic allocations. We believe a near-term pullback is possible but that the longer-term bull market is intact. Individual investors are showing signs of returning to the stock market and investor behavior analysis suggests that may continue to aid a continued upward trend.

© Charles Schwab