Doubts about the underlying momentum of the U.S. economy surfaced in the past few weeks. There are soft spots in the economy, but these are not enough to shake the positive fundamentals in place.

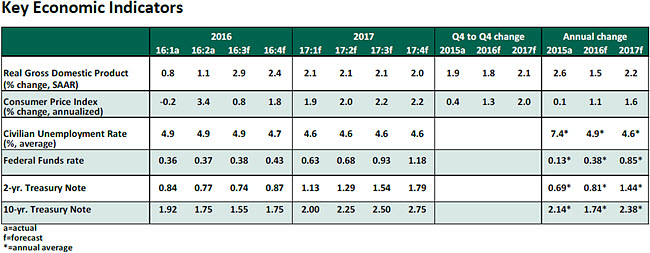

The inventory correction of the last five quarters is predicted to have ended. A small accumulation of inventories is one of the factors driving real gross domestic product (GDP) growth in the near term. Real GDP is predicted to rise 2.9% in the third quarter following three quarters of subdued growth.

Key Elements of the Forecast

The inventory correction of the last five quarters is predicted to have ended. A small accumulation of inventories is one of the factors driving real gross domestic product (GDP) growth in the near term. Real GDP is predicted to rise 2.9% in the third quarter following three quarters of subdued growth.

Key Elements of the Forecast

- Some slowing in consumer spending in the third quarter should not be surprising given the 4.4% increase seen in the second quarter. Although auto sales slipped in August, the average of the first two months of the third quarter exceeded the total second quarter average. The strength in employment and income are solid and household balance sheets are in good standing. These factors support expectations of continued forward momentum for consumer spending.

- The Institute of Supply Management’s factory and services survey results for August were on the soft side. The factory survey’s composite index fell below 50; readings below 50 denote a contraction in factory activity. Survey outcomes of the service sector suggest continued growth as the August index held slightly above 50.0, but it is the lowest since February 2010. These reports are a single month’s assessment; we will be monitoring the September survey reports for signs of additional weakness, if any.

- Business sector spending has not added to GDP growth for three straight quarters. The weakness is not confined to the energy sector but is also visible in the non-energy segment. The July report for durable goods shows a pickup in new orders, which is an encouraging sign. The oil rig count continues to advance after hitting a record low mark in May 2016, implying that the signals from the energy sector appear to be turning positive. Factory production numbers in July advanced following an increase in June. Putting these numbers together, there is a chance for an improvement in business spending during the third quarter.

- Economic reports from the housing sector were mixed. The increase in construction spending in July was concentrated in the home improvement component. The good news is that housing starts rose in July and permits issued for multi-family units increased. Purchases of new homes hit a new post-2008 high (654,000) in July. Sales of existing homes slipped in July and wiped out most of the gains recorded in the second quarter. Home prices rose 5.1% in the second quarter from a year ago, which is close to the gains seen in the past nine months. The level of the house price index is very close to the all-time seen in 2005 and is being watched.

- The strong dollar held back export growth during 2015. The trade-weighted dollar fell in the second quarter and traded sideways in the July-August period. Net exports have been mostly neutral for GDP growth in the first half of this year. Exports moved up in the second quarter and the July trade report showed the best performance of exports in almost three years.

- Inflation numbers continue to present a sanguine picture but caution should be exercised. The year-to-year change in the personal consumption expenditure price index is still below 1.0% and the core price gauge, which excludes food and energy, has not budged from around 1.6% during the first seven months of this year. The latest Beige Book indicates that there is wage acceleration in some Federal Reserve Districts. Higher wages will translate in to higher inflation in the months ahead.

- Labor market data continue to indicate that hiring continues at a decent clip. The unemployment rate at 4.9% held steady and is close to what is considered full employment. The three-month moving average of payroll gains at 232,000 exceeded the number of jobs necessary to have a steady unemployment rate. The details of the August employment report were good, but they did not signal the necessity to tighten monetary policy immediately.

- The 10-year U.S. Treasury note yield, at 1.69% as of this writing, has risen from the lows seen in July (1.37%) following the Brexit referendum. Still, long-term rates remain well below their standing at the beginning of the year (2.25%). Most analysts see the reduction of the term premium (extra yield required to hold a long-term bond versus a short-term bond) as the cause for lower yields.

The Federal Open Market Committee meets on September 20-21, and is widely expected to leave the policy rate unchanged at this meeting. The Fed is likely to use this opportunity to alert markets about the potential for a higher federal funds rate at the end of the year.