The One Statistic Every Bond Investor Should Know

If you’re a passive fixed-income investor trying to make sense of last Friday’s sell-off, the one statistic you must check—and now—is the average duration of your portfolio.

Why? Because investors who have moved to passively managed global aggregate bond funds—which had about 7.5 years of duration and a 1.8% yield to maturity as of August 31, 2016—have a lot more exposure to duration than they probably realize.

When interest rates are declining, duration—the measure of the sensitivity of a bond’s price (the value of its principal) to a change in rates—provides more bang for the buck.

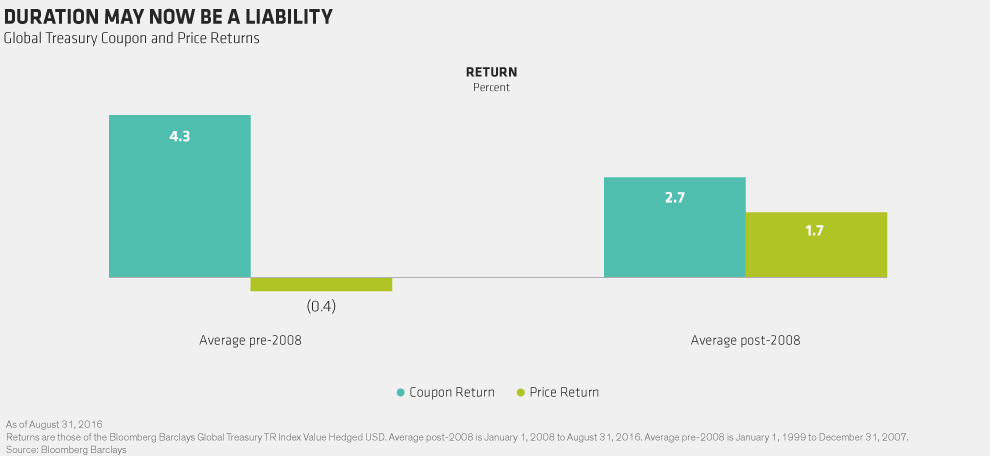

Duration has been a winning bet for the past several years as global interest rates have fallen. Since 2008, falling rates have generated stronger price returns—2.10% more, on average, annualized—than over the prior decade, even as coupon returns weakened (Display 1).

THERE IS NO SNOOZE BUTTON

But last week should be a wake-up call to all bond investors. The days of making easy money in a falling-rate environment are over. When interest rates rise, as they did last Friday in advance of next week’s Fed meeting, investors who have long-duration positions are usually punished.

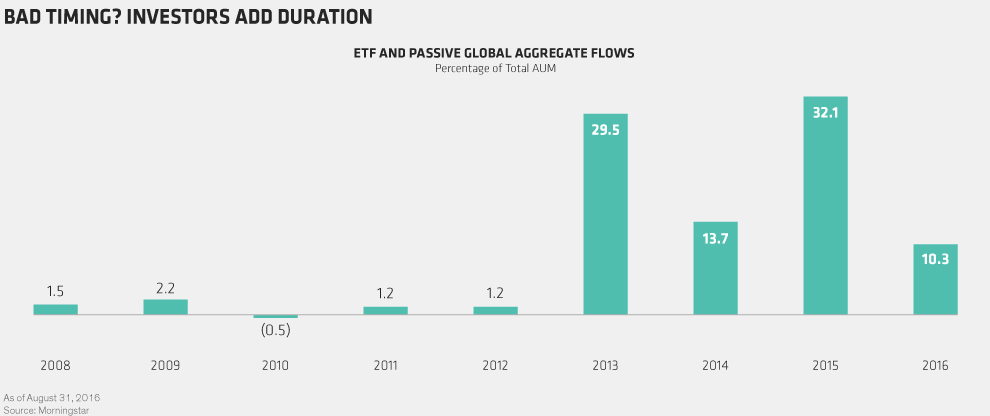

To make matters worse, most investors have poured money into funds at the bottom of this interest-rate cycle, when rates were at their lows. Since the beginning of 2015, ETF and passive global aggregate mutual funds have seen more than US$28 billion in net flows. That represented about 42% of total assets at the end of August (Display 2).

This is leaving many investors, probably unknowingly, with low yields and outsized interest-rate risk at possibly the worst time.

A TICKING TIME BOMB

Many investors could be sitting on a ticking time bomb. They won’t likely realize much more price appreciation, but they continue to have very long duration. Although it’s possible that interest rates may decline a bit from here, it couldn’t be anything like the degree of decline we’ve seen in recent years.

And given where we are in the cycle, it’s far more likely that interest rates will begin to rise. If rates were to rise by one percentage point, these passive funds could lose as much as 7.5%. That would far outweigh any potential coupon return, given their low yields.

This may turn out to be one of those cases in which investors who went to passive solely because of the low fees will be paying significantly for that decision over the long run. Actively managed world bond funds currently have an average duration of 5.8 years and a yield to maturity of 3.3%. That makes them far less sensitive to interest-rate changes than the passive funds.

PULLING THE RIGHT LEVERS

Of course, the average active fund could still experience negative returns if rates back up. However, active managers have more levers to pull to provide investors with better downside protection, which is one of the reasons for investing in fixed income in the first place.

For example, unlike passive funds, active bond funds have the ability to shorten their duration going into a rate sell-off. Furthermore, given their higher average yields to maturity, they have higher potential coupon return.

Lastly, most passive global aggregate strategies mirror aggregate indices, which are dominated by sovereign securities. More than 97% of the assets invested in ETF and index global aggregate funds are in sovereign-dominated strategies. In contrast, the average active manager has the ability to balance such interest-rate exposure with higher exposure to credit securities, which may smooth potential downside in a rising-rate environment.

It’s time passive investors start paying attention to duration and how much exposure their portfolios have. Active managers certainly are.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.