Key Points

- After August’s all-time highs followed by a stall, stocks were once again jolted into action by mixed messages from the Federal Reserve (Fed). We continue to believe the bull market is intact but near term risks are elevated.

- Economic data continues to have a groundhog day quality to it—perking up some before then pulling back again. The attendant movement between tighter and looser financial conditions has caused the Fed to also ping pong between dovish and hawkish rhetoric.

- The Fed isn’t the only game in town and other global central banks have added to uncertainty, with many catalysts this fall potentially adding to the monetary mashup.

Complacency no more

Some complacency had set in along with the low-volatility summer rally, but Fed policy uncertainty yet again shook the market out of its slumber. The S&P 500 didn’t decline more than 1% for 52 consecutive trading sessions, before last Friday’s 2.5% decline (for more see Liz Ann’s article Is That All). Volatility spiked in the ensuing week, largely fueled by a renewed uncertainty regarding global central bank policy, rising U.S. and global bond yields, and exacerbated by valuation concerns.

We remain relatively optimistic that the long bull market in stocks can continue, but have been consistent in our view that risks for a pick-up in volatility and more frequent pullbacks remain elevated. As a result, we maintain our neutral view on U.S. equities and urge investors to remain vigilant and stick to their long-term asset allocations—using volatility to tactically rebalance around strategic allocations.

Frustration building?

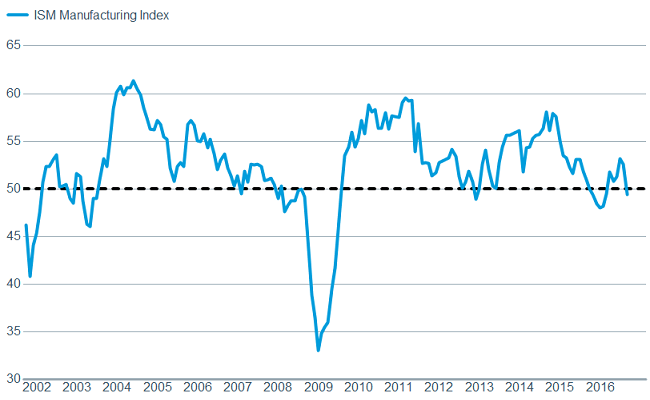

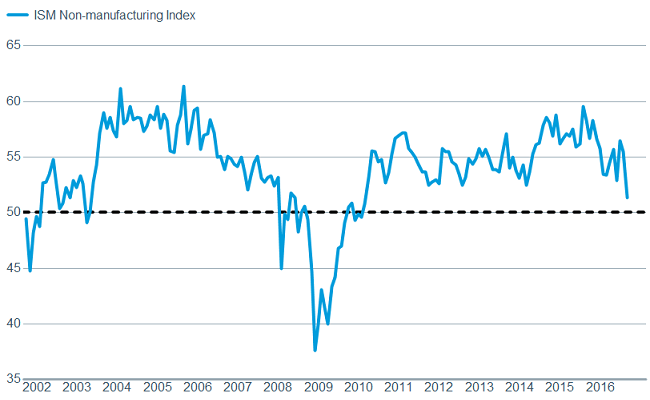

Patience can be difficult in this environment where we seem to be on an economic version of the classic movie “Groundhog Day.” Economic data appeared to be perking up in June and July, with better readings on durable goods orders, housing data, industrial production, and railcar loadings according to ISI Evercore Research. And while the economy still appears to be growing, the recent round of data has thrown some cold water on the hopes for a sustainable uptick in growth. The recent soft patch has become a pattern—with dips in growth having been experienced in every year since the recession ended over seven years ago. Manufacturing continues to struggle with the Institute for Supply Management’s (ISM) Manufacturing Index moving back into territory depicting contraction (below 50) at 49.4. Even more disappointing was the sharp drop in the new orders component (a key leading indicator) from 56.9 to 49.1. We believe that this weakness was exaggerated by the “August” effect when worldwide activity seemed to come to a standstill, but the trend bears close scrutiny. Also discouraging was the ISM Non-Manufacturing (services) Index falling by a larger-than-expected 4.1 points, although still on the expansion side of 50, while the new order component also fell precipitously.

Manufacturing still appears to be spinning its wheels

Source: FactSet, Institute for Supply Management. As of Sept. 13, 2016.

While the service side also seemed to hit a speed bump

Source: FactSet, Institute for Supply Management. As of Sept. 13, 2016.

The labor market still looks healthy, but the rate of improvement appears to be slowing. This should be expected as a tighter labor market means there are fewer qualified workers to fill open positions—which according to the July JOLTS report (Job Openings and Labor Turnover Survey) hit a record high. The tighter labor market has yet to generate a sustainable improvement in wage growth, with average hourly earnings (AHE) declining in August to 2.4% from 2.6% year-over-year. However, the mix shift of workers entering and exiting the workforce may be biasing this growth rate down. That is why an alternate measure of wage growth put out by the Atlanta Fed (via its “Wage Tracker”)—accounting for mix shift calculation problems—shows wage growth of a full percentage point higher than AHE.

There was also recently some very good news on the personal income front. This week the U.S. Census reported that median incomes rose from $53,718 to $56,516—the largest arithmetic and percentage increase in the history of the data back to 1967. While real median incomes are still below their 2007 peak of $57,423, the spiking income growth is being driven most by the bottom two deciles of the income distribution, which is good news in terms of income inequality.

The epicenter of déjà vu

This uptick in economic activity followed by some disappointing results has appeared to continually stymie the Fed and leave investors awash in uncertainty. Fed members have been talking up the likelihood of at least one rate hike this year, but with the disappointing ISM readings and still relatively low market odds of a September move, it seems unlikely they’ll make that move at next week’s meeting. We still believe one rate hike is on the table by year-end.

The uncertainty is global as the recent G-20 meeting produced agreement that more fiscal action was needed from all major countries, with leaders noting that monetary policy has probably reached its efficacy limits. In fact, some of the market’s recent volatility and the move higher in global bond yields are due to the possibility that quantitative easing (QE) is running its course globally and will not continue indefinitely.

Taper tantrum redux?

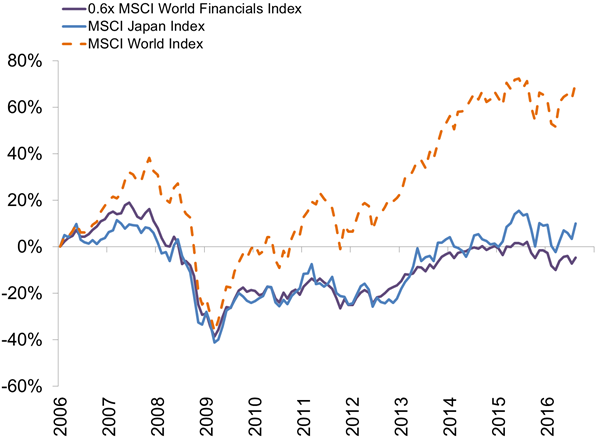

It’s not just the outcome of the Fed meeting that investors will be watching closely on September 21—the Bank of Japan (BoJ) also meets. The BoJ will provide a widely-anticipated “comprehensive assessment” of its current monetary policy at the meeting, and has hinted changes may be forthcoming. The head of the BoJ, Haruhiko Kuroda, has acknowledged the adverse effects of policy on financial companies. As you can see in the chart below, the entire Japanese stock market behaves much like the financial sector, making negative interest rate policy a key factor driving Japan’s stock market this year.

Total return of Japan’s stock market tracks the financial sector

Source: Charles Schwab, Bloomberg data as of 9/12/2016.

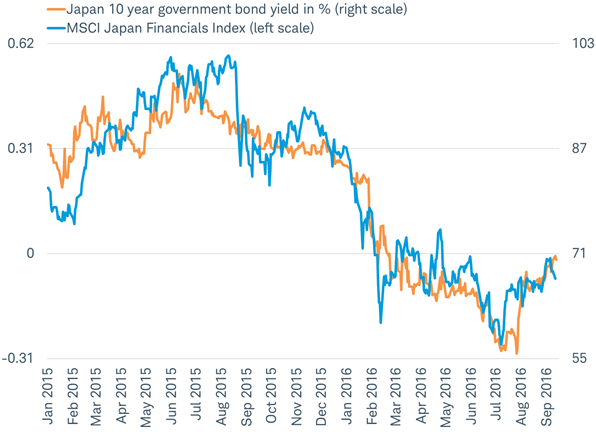

Mr. Kuroda has emphasized the slide in longer-term rates driven by the QE bond purchases as creating a problem for financials (by reducing the net interest earned on new loans). He also noted the challenge low long-term yields pose to Japan’s huge pension programs. This may mean further cuts in short-term rates (which may also benefit the economy by weakening the yen) and tapering longer-term government bond purchases to allow the yields on those securities to rise. When the tapering of QE was announced in the United States in 2013, longer-term rates jumped in a response and the period became known as the “taper tantrum.” In anticipation of a tapering in Japan, longer-term rates have already started to climb in a milder version of the taper tantrum. This has boosted the performance of Japan’s financial sector, as you can see in the chart below, making it the top performing sector so far in the third quarter.

Bond yields are on the rise with financial stocks in Japan

Source: Charles Schwab, Bloomberg data as of 9/12/2016.

The rebound means there is some risk to financial stocks—and, therefore, the entire Japanese stock market—if the anticipated policy changes are not forthcoming and rates head back down.

State of the European Union

Another contributor to global stock market volatility in September is the political and economic outlook for the European Union (EU), collectively the world’s largest economy. The State of the EU address was delivered by EU President Juncker on September 14 at a time when the EU is seeking to assess its health and identity. The upcoming Italian referendum proves a focal point for Europe identity crisis and the struggle between integration and nationalism. Polls remain closely divided on the referendum to streamline the Italian political system set to take place in less than two months. This has raised concerns that Italy is the next domino to fall to anti-EU sentiment;potentially triggering a chain of events that could result in Italy voting to leave the EU, as Britain recently did.

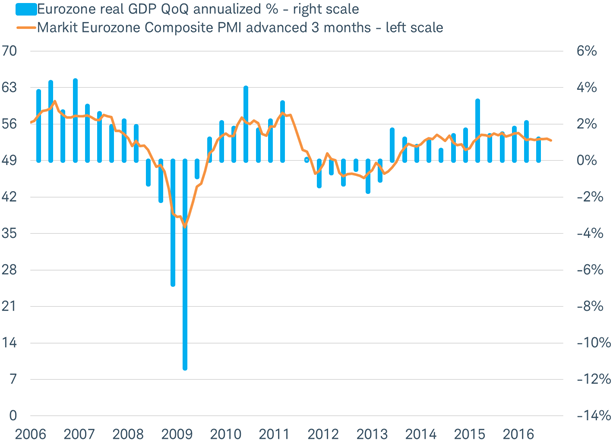

Stock markets may have been rattled by some European data for August missing economists’ estimates. Notably the Eurozone’s composite purchasing managers’ index (PMI), a leading indicator of gross domestic product (GDP) growth, took a dip from 53.2 to 52.9. Fortunately, Europe’s composite PMI has remained within a range of +/- 0.2 points of 53.0 since January 2016. A reading of about 53.0 has historically led to GDP growth for the Eurozone close to the 20-year average of 1.5%, as you can see in the chart below.

Data points to average growth in Europe

Source: Charles Schwab, Bloomberg data as of 9/12/2016.

Incoming data will be watched closely for signs of renewed weakness. The lofty earnings expectations by analysts for more than 20% growth in the coming 12 months, leaves global stocks vulnerable to disappointing economic data. (You can find more on the risks posed by the widest gap between expected and actual earnings since 2009 here: Mind the Gap: Are Earnings Expectations Too High?)

So what?

Volatility has picked up along with global central bank policy uncertainty and a back-up in U.S. and global bond yields. We believe the Fed is likely to hike rates one time this year, probably in December, but that central bank consternation will continue to elevate volatility. The long-running equity bull market should stay intact with modest economic growth continuing; and investors should remain globally diversified.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability. Rebalancing a portfolio cannot assure a profit or protect against a loss in any given market environment.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Institute for Supply Management (ISM) Non-manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms by the Institute of Supply Management. The ISM Non-manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Atlanta Fed's Wage Growth Tracker is a measure of the wage growth of individuals. It is constructed using microdata from the Current Population Survey (CPS), and is the median percent change in the hourly wage of individuals observed 12 months apart.,/p>

The MSCI World Financials Index captures large and mid cap representation across 23 Developed Markets countries*. All securities in the index are classified in the Financials sector as per the Global Industry Classification Standard (GICS®).

The MSCI Japan Index is designed to measure the performance of the large and mid cap segments of the Japanese market. With 318 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Japan.

The MSCI World Index is a stock market index of 1,642[1] 'world' stocks. It is maintained by MSCI Inc., formerly Morgan Stanley Capital International, and is used as a common benchmark for 'world' or 'global' stock funds. The index includes a collection of stocks of all the developed markets in the world, as defined by MSCI. The index includes securities from 23 countries.

The Composite Purchasing Managers Index (PMI) Index is a weighted average of the Manufacturing Output Index and the Services Business Activity Index.

(0916-LY7V)

© Charles Schwab