Key Points

- Stocks regained their footing as the Fed remained on hold yet again. The fourth quarter, however, features many potential market moving events, and October has offered some nasty surprises in the past. We believe this earnings season is important to the near-term future of the bull market.

- Some recent U.S. economic data has been weaker than expectations and we’ll be watching for coming releases to see if it’s only a soft spot or something more concerning. We lean toward the former but the answer will go a long way to determining if we see a rate hike in 2016.

- World trade has been in focus due to the election and there are both concerning issues and bright spots when looking at the global trade picture.

Investors are gearing up for the fourth quarter

Sports fans know that the fourth quarter is often when much of the game-deciding action occurs, and that may be the case for the stock market this year. The Federal Reserve has pushed the possibility of rate hike this year into the final quarter; the long-awaited return to positive earnings growth could be in store this quarter; economic data needs to show signs of bouncing back; and then of course there’s the U.S. election. Any or all of these could have a substantial impact on stocks. Add in what has a historical tendency for some pretty nasty October surprises, and the potential for an increase in volatility persists.

We continue to believe the secular bull market which began in 2009 is ongoing, but that we’re in a mature phase likely to see some discomforting bumps along the way. Timing these pullbacks right is extremely difficult and we urge investors not to try. Instead, stick with your long-term asset allocations and view pullbacks as a chance to add to positions as needed. If the risks are causing you to lose sleep, we suggest looking into potential hedging strategies, which could cost you some money to implement, but may also keep you from making a bigger investing mistake.

Earnings take the ball

After five consecutive quarters of declining corporate earnings, the coming reporting season could prove to be important to the near-term state of the bull market. With valuations at least modestly elevated by most measures, earnings need to start to carry the weight if this bull market is to advance. Earlier this year, analysts were expecting the third quarter to see earnings growth move back into positive territory according to Bloomberg; but recent downgrades have resulted in a consensus of still-negative growth. If the so-called “beat rate” (the percentage by which companies ultimately exceed consensus expectations) is consistent with the recent past, the quarter could see earnings back in positive territory. But if earnings disappoint, the market could be vulnerable.

According to Bloomberg, analysts are expecting a 10% earnings growth rate in the fourth quarter and a robust 16% growth rate in 2017. This seems a bit on the optimistic side and leaves the market vulnerable to an increase in volatility should those expectations have to be again downgraded. The collapse in the oil market is now in the rear-view mirror, which should help to solidify both the energy and basic materials sectors’ earnings growth rates. And the stability in the dollar has also removed what had been a headwind for exporters and the industrials sector.

Economy needs a fourth quarter comeback

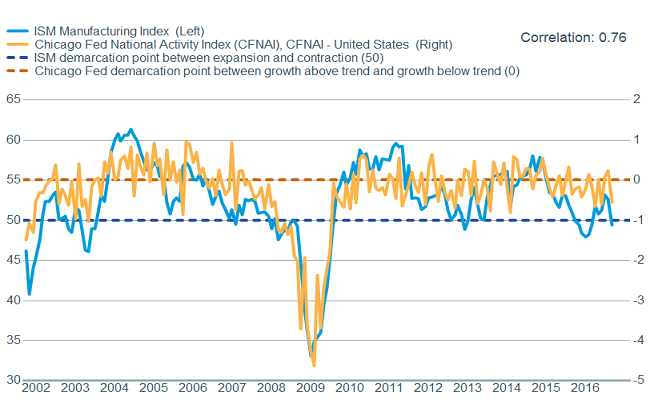

Economic data has been mixed over the past month. It started with soft Institute for Supply Management (ISM) readings at the beginning of September and continued with some weaker-than-expected housing data. Housing starts fell 5.8% in August and building permits dropped 2.3% according to the U.S. Census Bureau; while the National Association of Realtors reported that existing home sales fell 0.9% in August. The Chicago Fed also reported that their National Activity Index fell to -0.55 from 0.24, which has had a pretty good correlation with manufacturing activity in the past.

Chicago Fed confirms soft ISM reading

Source: FactSet, Institute for Supply Management, Federal Reserve. As of Sept. 27, 2016.

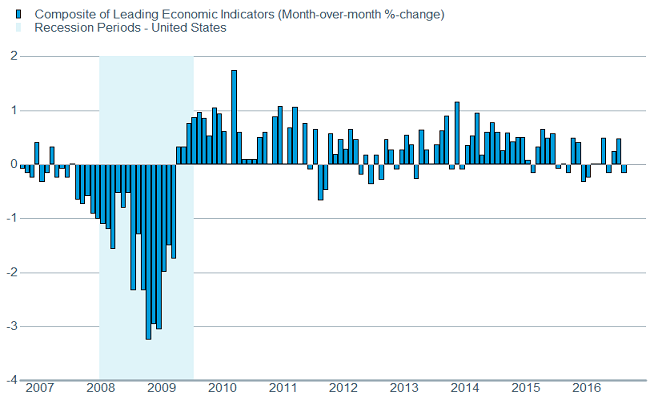

We’re also seeing some signs of potential weakening of the auto market, which had been on a solid run. According to Cornerstone Macro Research, the percentage of banks tightening auto loan standards is now over 8%, not a lot but up from negative territory in the first quarter (indicating more banks were loosening standards). This is likely due to the number of subprime loans that are now 60 days or more delinquent, which is up 17% year-over-year. Not surprisingly, this softer economic tone filtered through to the Index of Leading Economic Indicators, which fell 0.2% in August, although the previous month’s reading was revised slightly higher.

Leading Indicators confirm recent softness

Source: FactSet, U.S. Conference Board. As of Sept. 27, 2016.

Not surprisingly, the Atlanta Fed has had to decrease its estimate of third quarter gross domestic product (GDP) growth as a result of the weakness seen. Their “GDPNow Tracker” has fallen from an annualized growth rate of 3.6% at the beginning of August to 2.9% in their most recent projection.

At this point we believe this is temporary softness brought on by a very quiet August when more folks than usual seemed to be on the sidelines; and are looking for a comeback in the fourth quarter. Continuing historically-low initial jobless claims reading (a key leading economic indicator), the low unemployment rate, rising wages and consumer confidence, and ongoing accommodative monetary policy lead us to believe that the economy will continue to muddle through into 2017.

The Federal Reserve remains the quarterback

All of these factors play into what is likely to be the second-most asked question these days: “When will the Federal Reserve raise interest rates again?” The most recent Federal Open Market Committee (FOMC) meeting boosted expectations that a rate hike is likely before the end of the year; contingent on economic data remaining decent in the coming months. More of the FOMC’s voting body is leaning toward raising rates, as there were three dissenting votes on the decision to hold rates steady—a relatively high number indicating growing discordance among members.

This ongoing “running out the clock” strategy will likely add to the potential increase in volatility in the fourth quarter, which leads us to the most-asked question likely over the next six weeks: “How will the U.S. presidential election turn out and what will it mean?” While many investors will roll their eyes when thinking about the election, we only want to remind folks at this point that the United States has proven to be able to weather many storms and leaders of all stripes, conservative and liberal, strong and weak, popular and not, and we have little doubt the same will be the case this time around.

But it’s an “open election”—with no incumbent running—and those have historically brought choppier market action. If the polls remain tight into the election, volatility is expected to remain elevated.

Trade up?

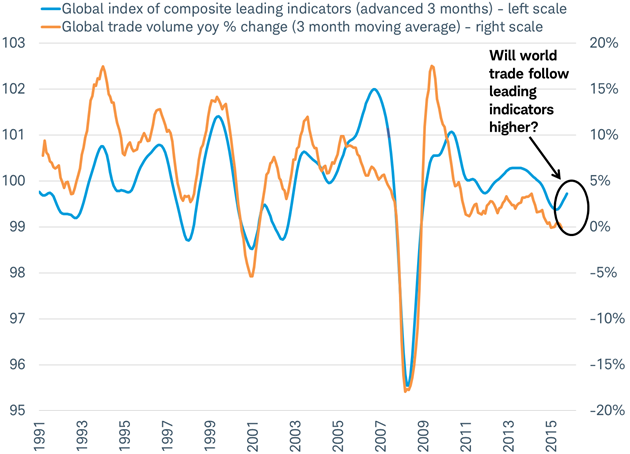

One contentious topic in the spotlight this election cycle is world trade. For the first time in 15 years, world trade is expected to grow at a slower pace than global GDP according to a forecast by the World Trade Organization (WTO). This could act as a headwind for larger capitalization companies which tend to have a higher percentage of non-domestic sales than their smaller peers. But before getting too worried about stocks in light of the WTO forecast, it’s worth considering that an indicator which has been an accurate forecaster of trade growth for 25 years suggests trade may be about to rebound, potentially lifting the sales of global companies.

For the past 25 years, world trade has followed the trend of the global Composite Index of Leading Indicators produced by the OECD (Organization for Economic Co-operation and Development), as you can see in the chart below. The indicator is designed to forecast economic trends in the 35 OECD member nations, plus the six major non-OECD nations. Together they account for more than two-thirds of world GDP. This leading indicator has been rising for the past six months, foreshadowing a potential rise in trade volumes.

Leading indicator points to rising trade volume in coming months

Source: Charles Schwab, Bloomberg data as of 9/27/2016.

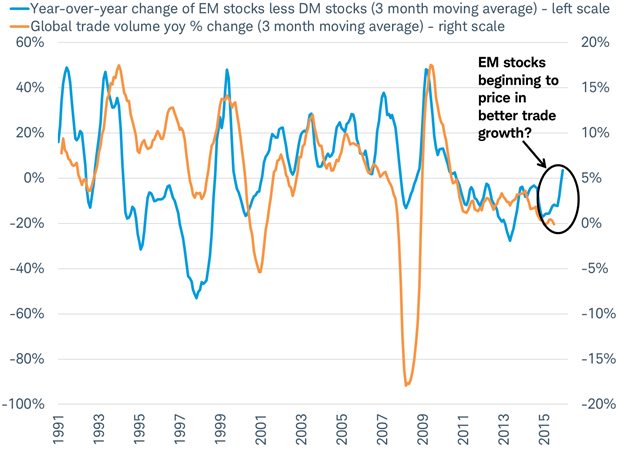

In general, improving trade volumes have been good news for emerging market (EM) stocks in the past. The performance of EM stocks relative to developed market (DM) stocks has tended to move in sync with the direction of trade growth, as you can see in the chart below. This year’s outperformance by EM stocks, driven by several factors including a weaker dollar, may be vulnerable if trade fails to improve.

Emerging market stocks seem to be pricing in a rebound in trade

EM = MSCI Emerging Market Index; DM = MSCI World Index

Source: Charles Schwab, Bloomberg data as of 9/28/2016.

Recent political events—like the surprise Brexit vote, the rise of anti-globalization parties in Europe, along with the aforementioned anti-trade rhetoric of the U.S. Presidential candidates—might suggest that exposure to trade-sensitive stocks may not be a good idea. However, it is important to keep in mind that companies have adapted to changing trade environments in the past. It’s also worth noting that the forces of globalization and technology which are driving some discontent in developed economies are also driving emerging economies into closer collaboration and boosting incomes. For example, China’s import growth turned positive in August for the first time in two years according to the General Administration of Customs, and U.S. automakers (GM and Ford) noted record sales in China on double-digit sales growth in their latest monthly updates. We believe long-term investors should remain committed to a diversified portfolio which may include exposure to U.S. and non-US trade sensitive stocks.

So what?

The fourth quarter is likely to bring bouts of volatility, but we believe the bull market lives on. Earnings growth is on the cusp of turning positive and the economy appears resilient enough to allow the Fed to boost rates. The U.S. presidential election has highlighted the pros and cons of global trade; and while the rhetoric is of concern, there are some potential positives in world trade developing and we would caution against shunning investments that may be exposed to trade issues.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability. Rebalancing a portfolio cannot assure a profit or protect against a loss in any given market environment.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Chicago Fed National Activity Index (CFNAI) is a monthly index designed to gauge overall economic activity and related inflationary pressure.

Leading Economic Index (Indicators) is an index that is a composite average of leading indicators and is designed to signal peaks and troughs in the business cycle.

The Organization for Economic Cooperation and Development (OECD) Composite Leading Indicator is a monthly indicator used to evaluate near-term economic prospects and risks and is designed to capture turning points in an economy's growth cycle at an early stage.

The MSCI Emerging Markets (EM) Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.

The MSCI World Index is a stock market index of 1,642[1] 'world' stocks. It is maintained by MSCI Inc., formerly Morgan Stanley Capital International, and is used as a common benchmark for 'world' or 'global' stock funds. The index includes a collection of stocks of all the developed markets in the world, as defined by MSCI. The index includes securities from 23 countries.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0916-MKRG)

© Charles Schwab