Is the Fog Starting to Lift?

Key Points

- Stocks slumped in the days leading up to the election, but despite a surprising result, stocks have soared off their post-election night lows. But there is much uncertainty ahead and we expect continued bouts of volatility.

- Stocks are up, but so are inflation expectations, explaining the sharp move up in Treasury yields. Reflecting this, and with election behind us, it still appears the Fed is set to raise interest rates in December.

- Wages are rising, but that doesn’t necessarily mean profit margins have to contract significantly.

The fog thins

The U.S. Presidential election is complete and despite the surprising result, stocks have staged an impressive rally. The country has managed to move on following bitter election fights and continue to prosper to varying degrees, and we have little doubt that will occur this time around, too. As such, we urge investors not to overreact to the results and to remain focused on long-term goals.

Investor sentiment leading up to the election had slumped as polls tightened, which set the stage for a rebound as some of the money that was moved to the sidelines in the run up to the election quickly moved back into stocks. But just because the U.S. election is over, it doesn’t mean volatility is likely to ease. The priority of President-elect Trump’s policy proposals are being weighed; and although the election was a Republican sweep, they still don’t have 60 votes in the Senate, other countries have important elections coming up, Fed policy uncertainty persists, and foreign central banks have begun to back away from negative interest rates.

Economic expansion continues—at a modest pace

Despite all the hand wringing over the election, the U.S. economy continues to grow, with third quarter gross domestic product (GDP) growth accelerating to 2.9% on an annualized basis, up from 1.4% in the second quarter, according to the Bureau of Economic Analysis. Part of the acceleration was due to inventories rebuilding after falling in the previous quarter; while the reading also got a boost from a surge in soybean exports due to crops in Brazil and Argentina being hit by weather issues (Reuters). As such, those boosts are unlikely to be repeated; but the early fourth quarter data suggest that we won’t give back all of the gains seen from the previous quarter. For example, auto sales rebounded after concerns that they may be in for a longer slump.

Auto sales rebound

Source: FactSet, Bloomberg. As of Nov. 7, 2016

Additionally, the Institute for Supply Management’s (ISM) Manufacturing Index moved further into territory depicting expansion by posting a 51.9 reading, up from 51.5. The ISM Non-Manufacturing Index also posted a solid reading, despite a modest pullback from the jump seen the previous month, moving to 54.8 from 57.1.

We are also hopeful that some political certainty could finally move companies to expand their capital expenditures which could be aided by promised regulatory relief, corporate tax reform, a plan to bring back cash held overseas, or a combination thereof. As seen below, capital expenditures have typically tracked with the operating rate, which remains somewhat depressed. It’s a bit of a chicken-or-egg scenario—companies won’t extend capex until their current resources are used to capacity, but they likely won’t be used at capacity until companies increase investment.

Companies remain reluctant to invest

Source: FactSet, U.S. Bureau of Economic Analysis, Federal Reserve. As of Nov. 7, 2016.

The fact that oil prices have stabilized and rig counts have started to rise should have a positive impact on spending in the energy space, which was slashed following the meltdown in prices. However it is unlikely we’ll see a big recovery in spending as caution in the space remains high judging from comments from major oil companies during earnings season.

Housing has been a positive force in the U.S. economy recently, and the increase in household formations should continue to support both the economy and consumer confidence. Consumers should also be bolstered by continued healthy employment conditions. Another 161,000 jobs were added to non-farm payrolls in October, while the unemployment rate dropped to 4.9% and average hourly earnings (AHE) increased again to 2.8% growth year over year. Other wage data measures—some adjusting for the mix-shift problems inherent in AHE—show an even sharper increase.

Rising household formations should help economy

Source: FactSet, Bloomberg. As of Nov. 7, 2016.

Fed picture becoming clearer but….

“Full” employment is at least in sight, housing is recovering, economic growth has improved and inflation is heating up. As such, the Fed funds futures markets are pointing to a rate hike at the Fed’s final meeting of the year in December. That may remove some uncertainty, but questions will remain as to the path and frequency of rate hikes in 2017 and beyond. We continue to believe the Fed will be able to go slow in normalizing rates, as they have stated they want to do, but signs of rising inflation could force its hand. Of note, commodity prices have shown signs of stabilizing, wages are rising, and the core Consumer Price Index (CPI ex food and energy) has moved to 2.2% on a year-over-year basis.

Commodity prices may be reversing their downtrend

Source: FactSet, Commodity Research Bureau. As of Nov. 7, 2016.

And inflation could become a concern

Source: FactSet, U.S. Dept. of Labor. As of Nov. 7, 2016.

At this point, we don’t see inflation taking off or causing the Fed to aggressively hike rates, but there is a risk the Fed could be seen as getting “behind the curve” if inflation heats up. We’ve already seen a significant increase in Treasury yields. Much attention pre- and post-election has been on Fed chair Janet Yellen and whether her post is in jeopardy. A president is limited in his ability to remove a sitting Fed chair, but it does bring up the possibility that she may not remain beyond the end of her term in 2018.

Three key votes remain in 2016

The year of surprising election results may not be over. The Brexit vote and U.S. presidential election point to the challenges in predicting outcomes. There are a few key votes before year end that could surprise and impact global markets. Here is what investors need to know:

- French republican primary on Nov 20 and 27 - The Eurozone might not survive in its current form if France elects National Front leader Marine Le Pen to the presidency next May. Le Pen seeks a re-negotiation of European Union (EU) treaties, restoring the primary of French laws over EU laws, ending the free movement of people, changing the European Central Bank’s mandate, and returning to a national currency (ditching the euro for the “new franc” in domestic transactions). While the run-off election isn’t until May 7, the unpopularity of current President Francois Hollande means Le Pen’s odds of winning depend on who she runs against from the Republican Party. The Republican primary is on November 20 and the run-off is a week later; a win for Alain Juppe may be seen as the tougher rival to Le Pen and a comfort to investors worried about a breakup of the Eurozone in 2017.

- Italian constitutional referendum on December 4 – The referendum to streamline Italy’s government is being viewed as a vote on Prime Minister Mateo Renzi, who has suggested he might step down if it doesn’t pass. The vote is the first of five hurdles before an Italian exit of the EU—and an ensuing potential financial crisis—is possible: 1) “no” outcome for referendum, 2) PM Renzi steps down, 3) the ruling coalition calls a snap election rather than nominating a replacement PM, 4) the anti-EU Five Star Movement wins the election, 5) a binding referendum would need to pass on leaving the EU. In our view, the risk of Italy leaving is likely low at this time, but as each hurdle is cleared, the risk of “Italeave” rises as you can see in the table below.

Italeave probability currently low but rises as each hurdle is cleared

Source: Charles Schwab & Co. Inc., as of 11/7/2016.

*Probability of December 4 referendum passing in current polling is at 50%. If the outcome of the referendum is “no”, there is a significant chance that Renzi will stay given that he seems to have backed away from his earlier statements. Leaders of the ruling coalition have stated they do not favor a snap election if Renzi leaves, but could still do so. The Five Star Movement party is currently polling under 30% support but nearly tied with the top party. Support for the EU in Italy was at 60% in the recent July IFOP poll.

For illustrative purposes only.

- Austria on December 4 – Austria is holding a re-run of May’s Presidential election due to faulty glue on ballot envelopes. The far-right Freedom Party of Austria is generally considered anti-EU. But even if Freedom party leader Norbert Hofer wins in a close race, the President in Austria is mainly a figurehead, with real power in the hands of the Chancellor who has said he would not hold a referendum on EU membership. Markets may react nonetheless.

Of course, 2017 holds German and French elections that will help to decide the fate of the Eurozone. While we think the most feared outcomes will be averted, we also believe markets may overreact in the short-term to surprise outcomes in these votes.

Great mall of China

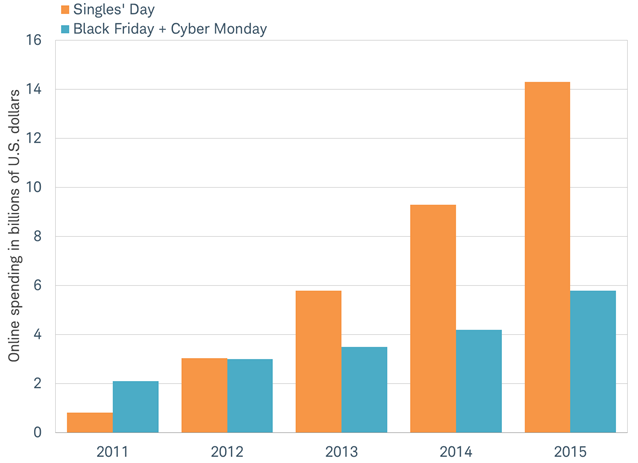

Finally, as a potential surprise to many Americans, the biggest shopping holiday in the world is November 11th—no, it isn’t Black Friday already—it’s Singles' Day. It started as an alternative to Valentine’s Day in China where there are 30 million more men than women according to the United Nations and it is held every year on November 11 (since the date is written as one-one-one-one). It’s China's version of Black Friday, but several times bigger.

This year China’s online sales may again rival all U.S. online and in-store sales on Black Friday, with this year’s Singles’ Day sales reported by Alibaba likely to be in the $15-20 billion range. Last year, the Chinese spent $14.3 billion on Singles’ Day—nearly three times what Americans spent online on Black Friday and Cyber Monday combined. In fact, China’s online sales total for Singles’ Day exceeded the U.S. total not just for online sales but for brick and mortar stores’ sales as well (at a combined $13.1 billion), according to data published by ShopperTrak and comScore.

November 11th is the biggest shopping holiday in the world

Source: Charles Schwab, Alibaba, comScore. Data as of 11/8/2016.

Many of the biggest U.S.-based retailers participate in Singles' Day, but their online deals are focused on Chinese shoppers. Asia is rapidly becoming the focal point for global consumer spending with middle class spending in China rivaling that of the U.S. middle class by 2020, according to World Bank estimates. The growth of Singles’ Day is a reminder why it is important to have a global perspective when investing.

So what?

The election is over but some uncertainty remains, which means bouts of volatility are likely to persist. The Fed is likely to hike rates in December but uncertainty about the path of rates in 2017 will persist. Additional uncertainty may come from elections around the world, with the potential for a continuation of surprising outcomes that could rattle markets at times.

© Charles Schwab