Schwab Market Perspective: Will the Momentum Continue Into 2017?

Key Points

- U.S. equities have held gains seen following the election, while there has been a definitive sector rotation indicating more confidence among investors. We believe the bull market will continue, although the sharp gains seen recently may give way to more sideways movement and/or potential pullbacks.

- Economic data has improved alongside a more business-friendly incoming Trump administration, helping bolster both stock and Treasury yields. The Fed is likely to raise rates at its December meeting, and may also raise its forecasts for economic growth and the trajectory of interest rates for the first time in this cycle.

- Populism has been a theme in 2016, but that doesn’t necessarily mean it carries into 2017, while for investors, it may not matter so much.

Animal Spirits?

November turned out to be an excellent month for the major U.S. stock indexes, with all three, plus the Russell 2000 index of small caps, hitting record highs. Although seasonal tailwinds should persist throughout the remainder of this year, we do expect to see some sideways trading and consolidating of gains at some point. That said we do believe the secular bull market is intact and, in fact, recently upgraded our view of U.S. stocks to outperform from neutral—offsetting a move to underperform for developed international stocks and the maintenance of a neutral rating on emerging market stocks.

We appear to be witnessing the revival of “animal spirits” among businesses and investors. After consistent outflows from U.S.-based mutual funds throughout this bull market, inflows have been strong over the past few weeks. This is a trend which could have significant legs into next year. In addition, the outperformance of more cyclical areas of the economy—financials, industrials, and energy—all indicate greater investor confidence in economic growth.

Economic momentum building into 2017

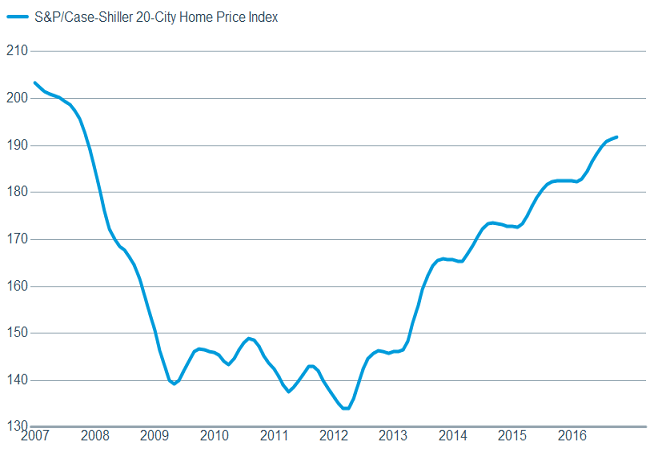

That improvement in investor confidence is matched by a boost in consumer confidence, which reached the highest level since July 2007 at 107.1 according to The Conference Board. The economy has shown steady improvement throughout the year, with quarterly annualized real gross domestic product (GDP) growth moving from 0.8% in the first quarter, to 1.4% in the second, and 3.2% in the third according to the Commerce Department. And the most valuable asset for most Americans continues to increase in value.

Home prices continue to rise

Source: FactSet, Standard & Poor's. As of Dec. 5, 2016.

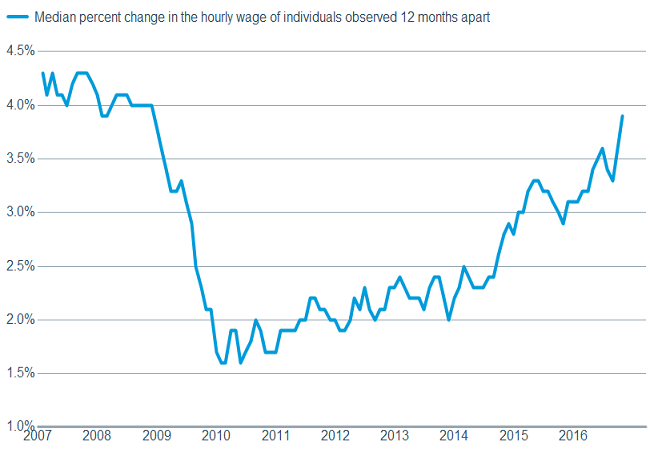

Also bolstering consumer confidence has been strong labor market data. Jobless claims remain near historic low levels, 178,000 non-farm payroll jobs were added in November, and the unemployment rate declined to a nine-year low of 4.6%. We saw a surprising pause in the rise in average hourly earnings (AHE), but we believe that to be an anomaly as the Atlanta Fed Wage Growth Tracker—arguably a better measure than AHE as it eliminates “mix shift” problems—shows much stronger wage growth.