Stable stocks are out. Riskier reflation plays are in. But who knows which way fickle market winds will blow tomorrow? That’s why strategies that harness stability and good judgement never go out of style.

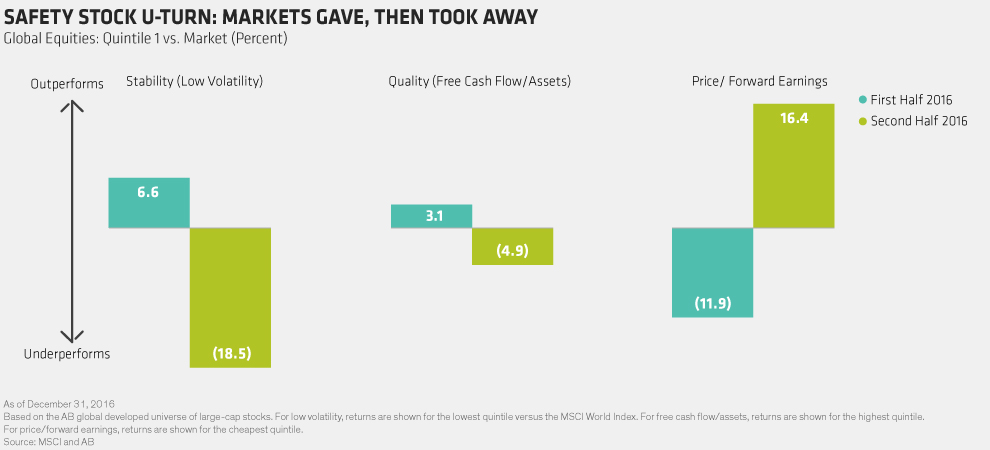

The U-turn in investors’ affections has been swift and dramatic. After more than a year of flying high, less volatile and higher-quality global stocks plunged to earth in the second half of 2016, massively underperforming the market. Cheaper (read, more cyclical) stocks took the lead (Display). The second-half sell-off in defensive consumer-staples, healthcare and utilities sectors wiped out nearly all of their collective first-half gains.

The reasons for this about-face are simple: pledges for big tax cuts, deregulation and higher fiscal spending in the US have raised expectations for global growth, inflation and interest rates. That backdrop favors financials and economically sensitive sectors, which have mostly struggled in the low-rate, low-growth postcrisis era. But it’s bad karma for the stable earners, high-dividend payers and other bond proxies that have led the market for the past several years, especially now that return-hungry investors are spotting juicier upside elsewhere.

NEW REGIME, NEW LINES OF DEFENSE

But, as any seasoned investor knows, what the markets give, they can take away—and then give right back again. As we wrote in an earlier post, this is no time to forsake defensive investing. Signs point to more turbulence ahead. And, remember, smoother-ride strategies have a long and impressive history of outperforming the market over full cycles.

Even so, safeguarding portfolios against downside risks will require far more creativity and agility than in the past, in our view. Traditional safe-haven stocks are highly sensitive to rising rates and risk appetites. These sensitivities intensify when rates are climbing from extreme lows, a scenario that looks increasingly likely given a more hawkish US Federal Reserve. These stocks’ premium valuations amplify these risks.

COMMON-SENSE STABILITY CAN STILL WIN

Despite this trickier terrain, we still see ways to build a winning defensive portfolio. First, be willing to give up some stability when it’s overpriced. Today, that means steering clear of the quintessential bond proxies in real estate, utilities, telecom and certain portions of the consumer-staples sector.

It may also mean accepting a bit more cyclicality and controversy when targeting companies with resilient profitability and healthy balance sheets. Examples are banks and insurers in countries where these industries are highly concentrated, or specialty chemical and software companies with strong pricing power. Though they are less obvious sources of stability than their more bond-like peers, they are less pricey than the market as a whole and should perform well regardless of the macro outlook. As these descriptions suggest, hunting in this territory requires intensive research and a keener risk radar.

Second, be ready to pivot. No trend lasts forever. Bond proxies are less crowded since the recent sell-off and, at some future point, new opportunities will surface. Case in point, we’re starting to eye some traditional defensive sectors that could ultimately benefit more from reflation than they are hurt by rising rates—for example, utilities with inflation-linked fees or supermarket chains with high operating leverage.

ACTIVE KARMA VS. PASSIVE DOGMA

Changes are coming fast, and uncertainties abound. Smoother-ride equity strategies must be adaptive. Approaches that dogmatically track low-beta stocks appear especially vulnerable. Because these indices are constructed largely based on historical patterns, they can’t change course when conditions diverge from those of the past.

For long-term, outcome-oriented investors, we think the secret to capturing the outperformance potential of lower-risk equities lies in a flexible, fundamentals-driven approach that can keep an even keel, no matter which way market winds blow.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

© 2017 AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein