US economic policies have always mattered to international investors. While President Trump’s agenda is still taking shape, equity investors can already map out broad guidelines for identifying winners and losers among companies outside the US.

In a recent blog, our colleague Jim Tierney outlined a checklist for selecting US companies that could do well in an era of unpredictable policymaking. While US companies are on the front lines of changes emanating from Washington, firms around the world will be affected as well. Looking at the issues from a global perspective can help investors frame the criteria that should influence a selective stock-picking process in a changing world (Display).

PERSPECTIVES ON TRADE

Trade and tariffs are a hot topic. But the potential impact of new policies aimed at defending US industry is not so clear-cut.

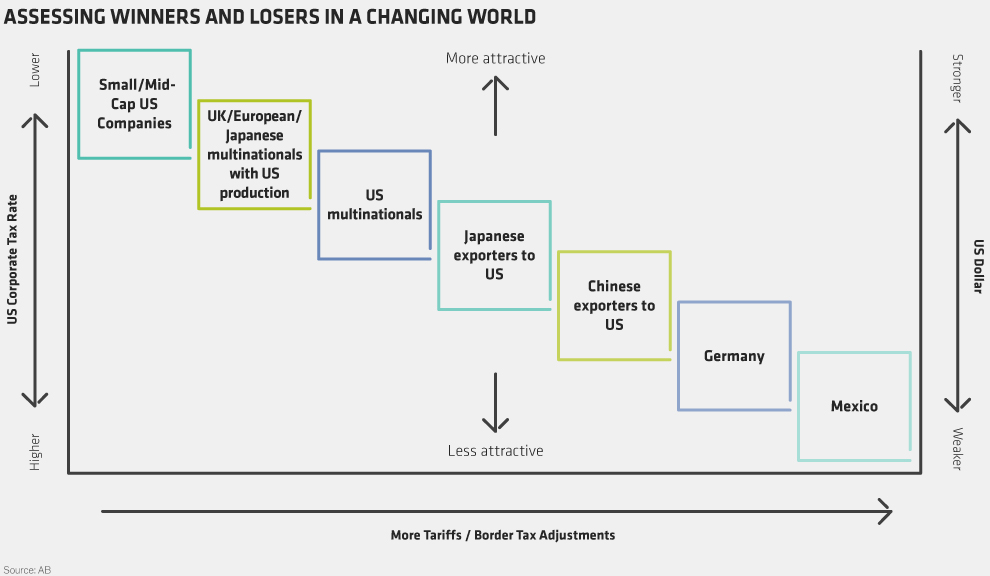

Some international companies could actually benefit from an increase of US tariffs. That may sound counterintuitive, but non-US multinationals with significant US production for the US market might come out ahead if imports become less competitive.

From a country perspective, China might not be as vulnerable as widely believed. Since the world’s most populous nation buys a lot of US goods, Trump may be deterred from taking a hard line on Beijing, in our view. At the same time, we think Germany might get hit harder than expected by tariffs, given its large trade surplus with the US. While we don’t think that “top-down” perspectives based on country economic outlooks should drive portfolio construction, these dynamics are important to consider in company-specific analyses.

TAX CUTS MATTER FOR MULTINATIONALS

US tax cuts aren’t purely a domestic US issue. Non-US multinational firms that pay a high US tax rate could benefit from a Trump tax cut. Still other multinationals that rely on international treaties to reduce the amount of tax paid in the US could be vulnerable to new efforts to clamp down on tax avoidance.

Fiscal spending priorities are poised to change under Trump. That could spell good news for international suppliers to the US infrastructure and defense industries. Other sectors such as pharmaceuticals, could find themselves at Trump’s mercy; if high drug prices become a policy target to reduce expenditures, international drugmakers with big business interests in the US could take a hit.

Many of Trump’s stated policies could support a sustained strengthening of the US dollar. For non-US companies with significant US sales, this could help boost profits when translated back to home currencies. For others, a strengthening US dollar could push up raw material prices, which threatens to hurt earnings.

INTEREST RATES AND CAPITAL ALLOWANCES

The appreciating dollar reflects expectations that US inflation may rise under Trump’s presidency, which could fuel a sustained increase in interest rates. Here, too, the effects on non-US companies are diverse. Companies with dollar-denominated debt might be vulnerable to higher financing costs, particularly in emerging markets, where dollar-denominated borrowing is commonplace.

Trump has also touted increasing the amount of capital allowance that companies can write off quickly for investment. We believe that a move like this would encourage global companies to boost their investments in the US, particularly in the technology sector. At the same time, interest charges may be disallowed as an expense against taxes, which would suppress the amount of capital available for US companies to launch takeovers and buy back shares. This would level the playing field between US and international companies, which do not always enjoy similar deductible interest benefits, and would make some international companies appear more attractive.