Key Points

- U.S. stock indexes broke to the upside, on better economic data but also heightened expectations of tax and regulatory reform. The bar is now set higher for policy action to support the rhetoric, setting up the possibility for a market pullback and/or a pickup in volatility.

- The economic picture continues to look good, but inflation is heating up, which has put a March rate hike by the Federal Reserve firmly on the table.

- An earnings growth recovery has helped fuel a global rally, but there are risks that expectations and valuations have gotten a bit extended.

Heating up…too much?

Stocks had been trading in a range around the 20k mark on the Dow for several weeks, but found their upside catalyst when President Trump promised "phenomenal" tax reform on February 9th. The renewed emphasis on tax reform as an economic stimulus helped push U.S. stocks to set records for the subsequent five sessions—the first time all three major indexes (Dow, S&P 500, and NASDAQ) had done that since January 1992. The Dow hit record highs for 12 consecutive days, something that hadn’t happened since 1987, took a pause, and then powered through the 21k mark following the President's address before Congress. We remain optimistic that U.S. businesses will get some much-needed tax and regulatory reform, but concede we may be borrowing gains from the future. Schwab's Washington team believes much of the administrations' proposals—specifically on tax reform—are more likely in the second half of the year than earlier.

As a result of recent gains, and the close to 20% gain in the S&P 500 over the last 12 months, attitudinal measures of sentiment are showing signs of excessive optimism, which is typically a contrary indicator. Ned Davis Research’s (NDR) Crowd Sentiment Poll has moved into extremely optimistic territory, while the National Association of Active Investment Managers Survey has moved into a range that has typically coincided with annualized gains of less than 1% in the S&P 500.

In short, be prepared for a pullback, but don't fear it marks the end of the bull market. We would likely view any pullbacks as buying opportunities for those needing to add to equity exposure; while also taking some of the pressure off from sentiment. In addition, although the attitudinal measures of sentiment show a bit of frothiness, the behavioral measures (like fund flows) aren’t yet matching that enthusiasm according to information from ISI Research.

Economy strengthening

Supporting stocks have been incoming data showing the economy appears to be strengthening. Surveys continue to indicate growing optimism in economic prospects with the Empire Manufacturing Index rising to a robust 18.7 from 6.5, while the Philadelphia Fed Index rose to the highest level since January 1984 at 43.3. Regional surveys were corroborated by the Institute for Supply Management's (ISM) Manufacturing Index moving to 57.7, while the new order component rose to a very robust 65.1. The National Federation of Independent Business (NFIB) Optimism Index ticked still-higher to 105.9—another 12-year high.

Business optimism continues to grow

Source: FactSet, Natl. Federation of Independent Business. As of Feb. 28, 2017.

The retail sales release by the Census Bureau also bested expectations, showing the sales grew 0.4% month-over-month (m/m); while excluding the more volatile autos and gas components, sales rose 0.7% m/m. And employment continues to look quite strong, with the leading indicator of initial jobless claims falling to a new post-1973 low.

The labor market looks quite strong

Source: FactSet, U.S. Dept. of Labor. As of Feb. 28, 2017.

Could the Fed’s hand be forced?

All of this positive data appears to be starting to filter through to inflation gauges. The Consumer Price Index (CPI) rose a higher-than-expected 0.6% m/m, while the core rate rose 0.3% m/m, and is up 2.3% year-over-year.

Inflation is trending higher

Source: FactSet, U.S. Dept. of Labor. As of Feb. 28, 2017.

Higher inflation and stronger economic data—and perhaps the stock market's rip higher—have led to more "hawkish" commentary from the Fed recently. March Fed hike expectations have risen considerably, now well over 80%, following Chairman Yellen’s testimony before Congress where she appeared to make an effort to indicate that March was indeed a "live" meeting. Following her appearance, there was a concerted effort among other Fed voting members to prepare the market for a potential March hike. History compiled by Strategas Research Partners shows that the best stock market performance during a rate hiking cycle comes when the Fed moves slowly in the first year, but quicker in the second year. That pattern appears to be panning out in this cycle.

Politics dominates

The Trump administration's comments about upcoming tax reform and regulatory relief, as well as meetings with various business leaders, has bolstered business and investor optimism. But the expectations bar may be set a bit high now relative to how slowly the policy sausage is actually made in Washington. Additionally, the details of potential tax reform will matter as there could be some areas of the economy that benefit more than others. We and our colleagues in Washington believe that tax reform is likely to be "unpacked," with the corporate side tackled first and the personal side pushed further toward next year. For this and many other reasons, policy uncertainty is likely to remain elevated. For now, it's been accompanied by an unprecedented lack of volatility, but likely not in perpetuity.

Earnings reflation

The theme of elevated expectations continues globally; as at the start of this year, analysts' double-digit earnings growth expectations for 2017 for companies in Europe, the United States, and Japan set a high bar after two years of back-to-back declines. Often too optimistic, analysts are typically forced to lower their earnings per share targets for the current year as it unfolds. The cuts in estimates from the beginning of the year to the end of the year vary in size, but on average over the past five years, according to FactSet, they have been about 3% for the U.S. (S&P 500), 5% for Japan (Nikkei 225) and 11% for Europe (Euro STOXX 600).

So far those elevated expectation are being met and the typical cuts aren't happening this year. The trend in analysts' estimate revisions has been better than average in all three regions, as you can see in the chart below. This has likely helped support solid gains in global stocks this year.

Trend in revisions to analysts' 2017 earnings estimates are better than average

U.S. = S&P 500 Index; Japan = Nikkei 225 Index; Europe = Euro STOXX 600 Index

Source: Charles Schwab, Factset data as of 2/28/2017.

Encouragingly, the double-digit growth expectations remain intact for all three regions even following the close of the fourth quarter reporting season, when corporate leaders offer guidance on the coming year. However, there are risks to the trend.

One risk to analysts' outlook is the potential for a moderation in the pace of inflation. Inflation is a key driver of growth in revenue and costs. As a result, over long periods of time changes in the level of inflation tend to have little net effect on the profit growth of most industries. But when selling prices temporarily rise relative to wages, profits may improve. Measures of the near-term trend in inflation—such as the latest readings on output prices from the regional manufacturing purchasing managers' indexes—have been highlighting rising selling prices to various degrees, as you can see in the chart below (readings above 50 indicate rising prices from the prior month).

Selling prices have been rising…

Source: Charles Schwab, Bloomberg data as of 2/28/2017.

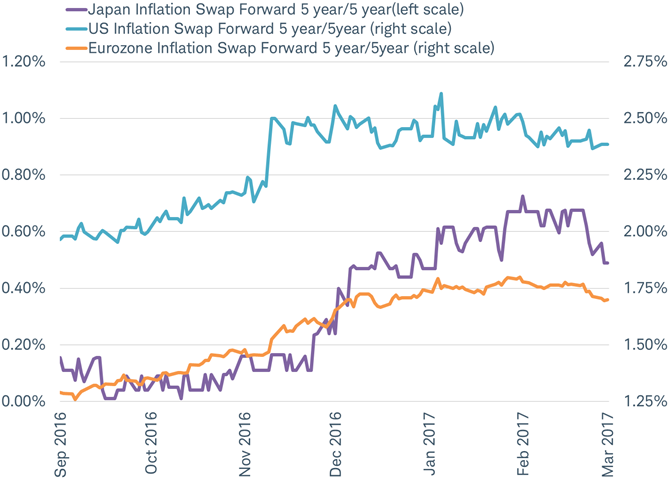

However, after rising for much of the past six months, market-based measures of future inflation began to roll over in late February, as you can see in the chart below.

…But the outlook for future inflation stopped rising in February

Source: Charles Schwab, Bloomberg data as of 3/1/2017.

"Reflation" has been a key theme for global stock and bond markets in recent months. One month of a slumping inflation outlook doesn’t necessarily mean that theme has come to an end. But we will be watching it closely since a stall or slowdown in the pace of inflation may act as less of a short-term tailwind to profit growth for many global industries and could weigh on stock prices.

So what?

The stock market's rally resumed following the President's comments on tax reform and investor optimism continues to rise. There are solid economic supports for the market's surge, but gains may have gotten a bit ahead of themselves and a pullback should be expected at some point. As lovely as "melt-ups" feel while they're happening, a healthier pattern for stocks is to consolidate gains after significant rallies. Fundamentally, earnings have been solid, supporting the rally, but there are risks there as well as doubt about the "stickiness" of pricing power increases. Stay patient, diversified, and remember the power of rebalancing. We believe this secular bull market still has legs, but discipline is essential.

© Charles Schwab