Global bond markets were roiled at the end of 2016 with higher rates and a re-steepening of the yield curve. The interest rate sell-off occurred during a change in global inflation expectations as discussions regarding deficit financing, infrastructure spending, and fiscal stimulus took center stage at a time when labor markets were generally considered tight given current low unemployment levels.

The recently confirmed Secretary of Treasury, Steven Mnuchin, indicated that he would: 1) look to extend the average maturity of Treasury’s portfolio beyond the already rapid extension that took place from 2009 onwards; and 2) possibly review the issuance of a 100-year bond as an instrument used to achieve that maturity extension.

At GMO, we will not venture a guess as to the likelihood of such issuance by the Treasury, but comments during the Borrowing Advisory Committee immediately following the presidential election suggested such an issuance was less likely than anticipated. However, more recent comments by Mnuchin and Gary Cohn1 have led us to believe that the possibility of an issuance is becoming more and more likely. From the perspective of our Benchmark-Free Allocation Strategy, which has a CPI-based performance target, we believe such bonds would not always make sense.2 However, our colleagues responsible for GMO’s Emerging Country Debt strategies, which are managed against a benchmark with a long duration, appreciate the significant alpha opportunities that some of these bonds represent.

An issuer’s utility function includes concerns about debt market maturity structure as well as, particularly in developed markets, creating a term structure for capital markets. Investor concerns, on the other hand, are focused on liability management and, for active managers, alpha generation. The following discussion is applicable to “ultralongs,” including the 100-year and 50-year maturity points.

100-year debt

There is nothing new about ultralong debt issuance. Indeed, the British government issued perpetual debt, called “Consols” during the Napoleonic War. The United States itself has forayed into the greater than 30-year issuance space with the Treasury issuing several bonds with those maturities, including a perpetual bond in 1900 and a 50-year bond in 1911.3 Some academic observers, such as John Cochrane, have argued that the US Treasury should issue perpetual securities as part of its regular and predictable issuance program. While Consols no longer exist, several governments have taken advantage of low absolute rates and the relative historical flatness of forward curves to issue longer-dated debt both in the developed and emerging market space. Countries as diverse as Mexico, Ireland, Belgium, and the UK have issued these so-called ultralongs. Certain corporates and private issuers have also tapped the long end of the curve, with names as disparate as Disney, Coca-Cola, and Petrobras. Non-profits such as Cal Tech, the Cleveland Clinic, DC Water and Sewer, Tufts, MIT, and New York Presbyterian have also taken part in this market.

At GMO, we have invested, at times, in 100-year issues, particularly through our Emerging Country Debt team. As we will explain later, century bonds, at the right price, allow a judicious and thoughtful long-term investor to harvest risk premia and garner outperformance relative to that issuer’s other, more vanilla, short-term issuances. In this paper, we explore both the issuer and investor motivation for borrowing and lending money for a century.

What are the issuer motivations?

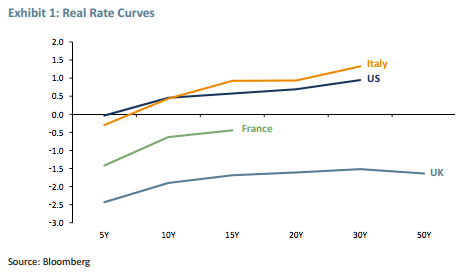

Interestingly enough, the motivations for issuance varies between different entities. For private sector funders, it could mean locking in longer-term funding at credit spread or all-in yields that the issuer feels are optimal. For public sector issuers, the rationale can be more varied: It could mean creating the public good of a benchmark reference rate; or simply meeting a policy target such as maturity extension; or offering supply to a captive investor base such as the liability-driven investment (LDI) community, which uses such maturities for discounting purposes. For example, the UK has been among the most aggressive of developed market sovereigns in extending the weighted average maturity (WAM) of its portfolio versus other countries, but is able to do so because of the ready LDI market that exists. Indeed, if one looks at historical UK real rate curves, their richness, characterized by their inversion, is driven by persistent LDI demand that is economically incentivized to hold these securities. Yet what primary risks or issuance opportunities are both these public and private sector issuers attempting to address?

#1: Rollover risk

The most common reason cited anecdotally by debt managers for extending the maturity of their liability portfolio is rollover risk. What do we mean by rollover risk? In this case we mean either the risk that short-dated debt has to be rolled over at a cost higher than current forward rates indicate or, in the most extreme case, the inability to roll over any debt due to loss of market access. The catalyst for this risk can be either endogenous to an entity’s credit quality, or can be an exogenous event driven by conditions in financing markets. We saw this risk play out for private issuers during the Global Financial Crisis: During the crisis, several issuers, including General Electric, were able to tap the debt market only through a government guarantee program such as TLGP – the Temporary Liquidity Guarantee Program. In addition, we have seen emerging market countries attempt to mitigate rollover risk in foreign currency issuance via longer-dated issuance. For these entities, the goal of long-dated debt issuance is to minimize or forestall higher funding costs or threats to issuance.

#2: Portfolio liability management

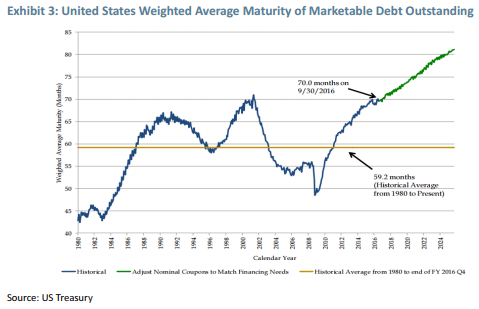

Issuance can be driven by portfolio liability management, by which we mean that the issuer has a reason for a specific weighted average maturity of the portfolio. There can be a number of interconnected reasons for this such as cost, asset liability management, or policy targets. The exhibit below shows the extension of the WAM of the US Treasuries market. This was a deliberate decision to increase the WAM after a large amount of short-dated bill issuance for TARP and other extraordinary financing measures that occurred during the Global Financial Crisis. Obviously #1 and #2 are somewhat intertwined, as portfolio liability management is sometimes driven by concerns of rollover risk, but can be driven by other objectives such as cost.

#3: Market structure

Issuance decisions are often based on existing market structure or an attempt to enhance current operations. Current market structure may encourage longer-dated issuance. The example we have utilized in the UK is that of the LDI community, whose discounting rates are linked to the longerdated UK sovereign rates, particularly in the inflation-linked securities market. In contrast, the US developed the floating rate note program (FRN), and in recent years increased bill issuance due to the scarcity of money-like sovereign debt assets. Likewise, the much-derided 20-year nominal Treasury,4 and later 20-year TIPS, were eventually ended because of tepid market demand relative to the 30-year maturity point.

What are the investor motivations?

Indexing requirements

Many fixed income indices are rules-driven products that stipulate the criteria for a bond to be a member security. For example, if the relative benchmark is the Barclays US Aggregate Bond index, then a fixed-rate ultralong issuance that meets its criteria will be included. We’ve noted that $20 billion of issuance in a year is likely worth less than a tenth of a year of duration extension in the Aggregate index (assuming constant proportion in the index).

Liability-driven investing

For investors who have long-duration, rate-sensitive liabilities, an ultralong bond may be a useful or even critical asset for appropriate asset liability management.

Cheapness or value

Bond investors knowingly or unknowingly invest in a risk premium. Generally the three types of premia that a fixed income investor is exposed to are the following:

-

Credit risk premia. We find that credit curves generally tend to be upward sloping for most types of issuers. The net present value of spreads relative to default risk tends to be higher than the actual cumulative default risk for that period of time.

-

Liquidity risk premia. This is the premium charged on a security in case of liquidity risk. One practical way to gauge the liquidity risk premium is to compare securities with similar maturities and credit risk. For example, a clear case of liquidity pricing in fixed income markets is to compare the “on-the-run” versus the “off-the-run” spread metrics of the same issuer.

-

Term Premia. The term premium on an interest rate is the premium charged by investors to hold a fixed rate instrument in case rates move higher than currently priced into their expectations for forward rates. Another way of stating this is that the term premium is the difference between observed forward interest rates (such as in the commonly cited 5y5y) and the future spot rates that investors expect to manifest.

-

Convexity. Ultralong bonds have enormous convexity. There are a number of definitions of convexity, but the most commonly used ones are as follows: 1) the rate of change of the duration of a bond as yields change (the second derivative of bond pricing formulas); and 2) the shape of the non-linearity of a bond’s capital gains in an interest payout model. The wonderful thing about long-duration fixed income instruments for an investor is that as yields increase, duration decreases, and as yields move lower, duration increases. The implicit outcome is that the investor has less to lose on an interest rate sell-off than he or she would make on an interest rate rally. Indeed, the buyer of an ultralong bond is somewhat equivalent to being long gamma in an option strategy with likely better theta characteristics.

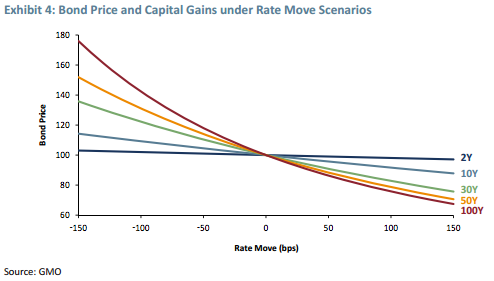

Another way to illustrate the asymmetry of payoffs can be seen in the chart above, which shows the capital gains payoffs of bond prices for a variety of maturities. Note the curve of the longer-dated bond: A 100-basis-point rally provides considerably higher capital gains than the losses due to a 100-basis-point sell-off in interest rates, particularly as maturity extends. The curvature of the line becomes more acute with increasing maturities. The increased curvature allows a bond investor to garner a higher capital gain when rates decrease than the amount of capital losses if rates increase by the same amount. This is visibly present when comparing the points such as the +100 or -100 areas on the curve. The most extreme example is an approximately 42% gain and approximately 25% loss on the 100-year maturity. This asymmetry of returns has value in capital markets.

Summary

For most investors, the 100-year issuance is likely to be cheap relative to other securities that are part of their investable benchmark. However, there remains a catch. Investors such as GMO will purchase the security (or indexers will take an active weight) if they determine it is “cheap,” but that cheapness will come at the expense of the issuers who are required to pay for the various premia that were described earlier in this paper. Issuers who are new to such a market should be aware of that phenomenon: Alpha-driven investors will be purchasing this security because they believe that they are being more than compensated for the maturity characteristics of the issuance. The issuer will likely pay in liquidity, credit, and term premia, and will most likely not be compensated for the convexity they have dispensed into the market. That does not mean the issuers are doing anything wrong in their financing strategy: Their justification is that they are willing to pay higher financing rates, or premia, as insurance against conditions that would jeopardize other goals.5 Given this willingness, thoughtful investors can be selective about the security selection choices available in the long-dated issuance market.

Amar Reganti: Mr. Reganti is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2015, he was the Deputy Director of the Office of Debt Management for the U.S. Department of the Treasury. Previously, he was a director and portfolio manager for investment grade credit at UBS Global Asset Management. Mr. Reganti earned his BA in Economics from Vassar College, his MS in European Political Economy from the London School of Economics, and his MBA from the University of Chicago Graduate School of Business.

Disclaimer: The views expressed are the views of Amar Reganti through the period ending March 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Copyright © 2017 by GMO LLC. All rights reserved.

Copyright © 2017 by GMO LLC. All rights reserved.

1 Mr. Cohn is Director of the National Economic Council.

2 However, GMO’s Global Asset Allocation Strategy has a 65% equities/35% fixed income benchmark. It may allocate to fixed income through the GMO Core Plus Bond Strategy, which may consider ultralong bonds as an alpha opportunity.

3 Kenneth D. Garbade, “Beyond Thirty: Treasury Issuance of Long-Term Bonds from 1953 to 1965,” Federal Reserve Bank of New York, Staff Report No. 806, January 2017.

4 April 30, 1986 Treasury Quarterly Refunding Statement.

5 As my colleague Ryan McManus aptly states, “Many of those issuers do not have a P&L target they need to earn, but rather a set of policy targets or a utility function in their liability management.”

© GMO

Read more commentaries by GMO