GMO

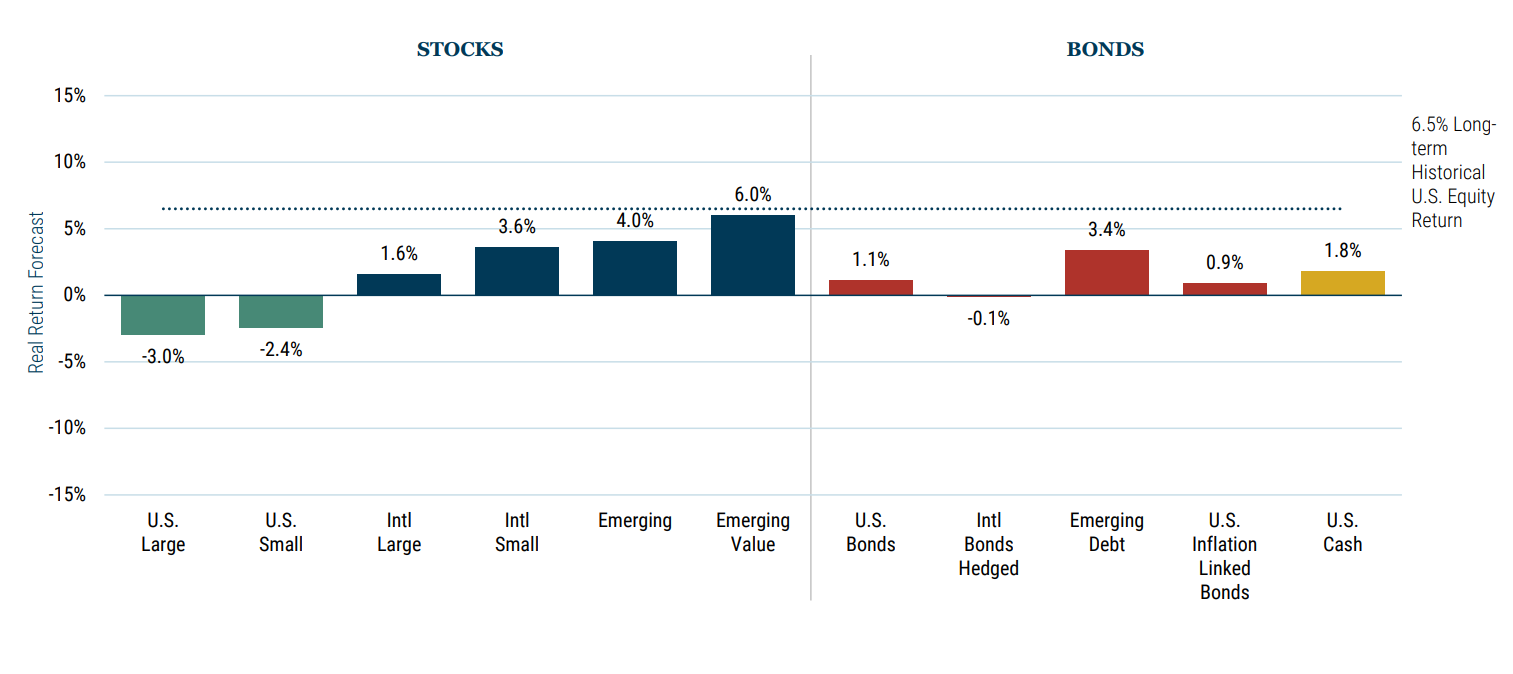

GMO 7-Year Asset Class Forecast: 2Q 2026

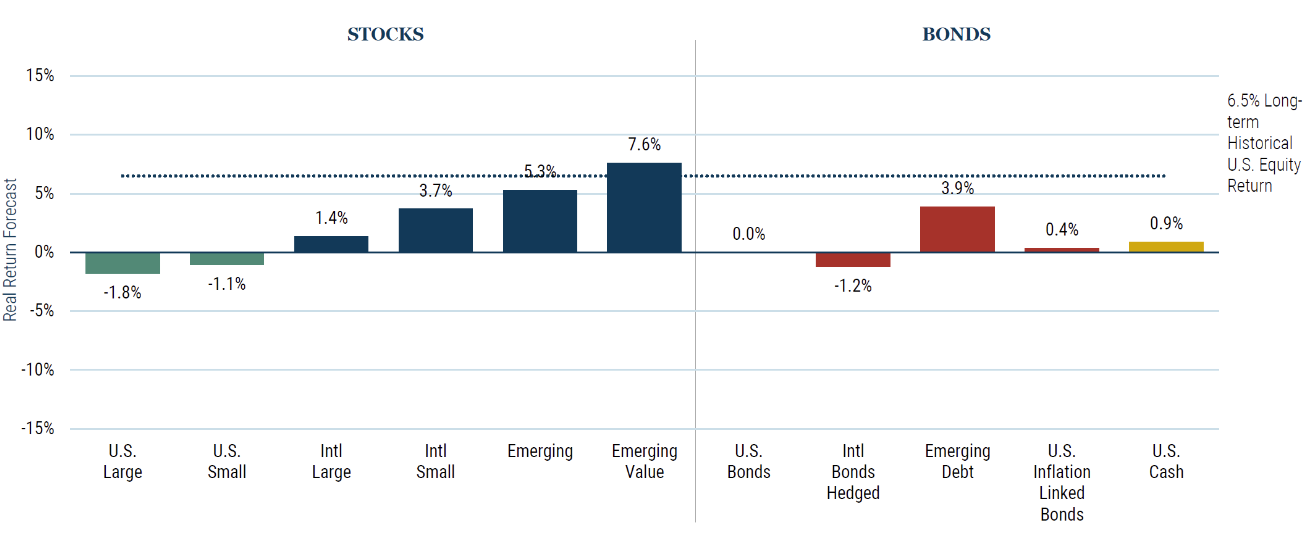

GMO has posted a new 7-Year asset class forecast for 2Q 2026.

Mid-Year Update: Equity Dislocation Strategy

It has been an eventful six months, and we are delighted that the Equity Dislocation Strategy has risen to the occasion. The Strategy generated a 9.05% net return in the first half of 2026, compared with a 1.3% return for MSCI ACWI Value minus MSCI ACWI Growth, a broad proxy for the value-growth spread.

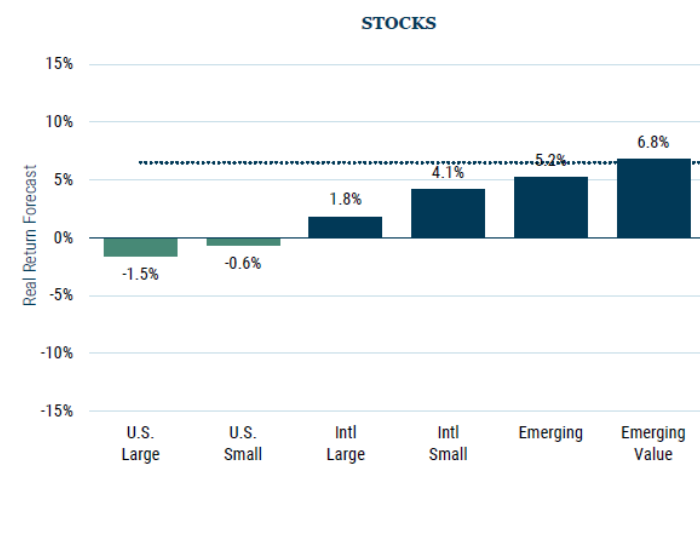

GMO 7-Year Asset Class Forecast: May 2026

GMO has posted a new 7-Year asset class forecast as of May 31, 2026.

Japan Equities

For the last eight years, GMO’s Asset Allocation team has held a differentiated view on Japanese equities. Long before Japan re‑entered the global investment narrative, we argued that the country was undergoing slow but durable structural changes aimed at improving corporate governance, growth, and capital efficiency. These reforms were never expected to deliver quick results. Instead, we expected them to compound quietly over time.

Diversifying Beyond 60/40 With a More Dynamic Allocation

Thanks to strong gains in markets over recent years, the 60/40 default portfolio has quietly morphed into a bundle of expensive U.S. growth equities and credit exposures offering narrow spreads over Treasuries.

Letter to the Investment Committee on Private Equity

Some institutional investors who had grown accustomed to outperforming the broader private equity composites are finding they have not done so consistently in recent years. Their diagnoses of the problem often center on specific decisions or biases they made in their recent manager selection, whereas a likely culprit is a falloff in the persistence of outperformance among private equity managers.

What Barbarians Like to Take Private

While most institutional investors recognize that private equity and public equity share similar economic risks, they often seem to ignore how their aggregate equity portfolio is affected by their substantial allocation to private equity.

GMO 7-Year Asset Class Forecast: April 2026

GMO has posted a new 7-Year asset class forecast as of April 30, 2026.

The Case for Liquid Alternatives in Today’s Environment

The logic of balanced investing is straightforward: equities drive long-term growth, bonds provide income and ballast when stocks fall, and the combination delivers a smoother ride than either asset alone. For decades, the 60/40 portfolio has been the default framework for good reason – it has worked, often brilliantly, across multiple market cycles.

The Case for Acting Now in International Deep Value

After years of U.S. equity dominance, conditions were shifting coming into 2026. Earnings growth outside the U.S. had begun to converge, wide valuation gaps narrowed modestly, and investor interest in international equities was rebuilding. While the Iran war injected uncertainty and temporarily dampened enthusiasm for non‑U.S. stocks, the underlying setup remains intact.

How A “Big Bet” Remains Poised for Future Outperformance

International deep value stocks are a high-conviction, active position across all GMO Asset Allocation portfolios. We define the deep value group of securities as the cheapest 20% of the market, a broad opportunity set that allows us to construct portfolios that are cheaper than traditional value indexes but still high in quality.

Valuation Metrics in Emerging Debt: 1Q26

GMO has posted a new Valuation Metrics in Emerging Debt: 1Q26

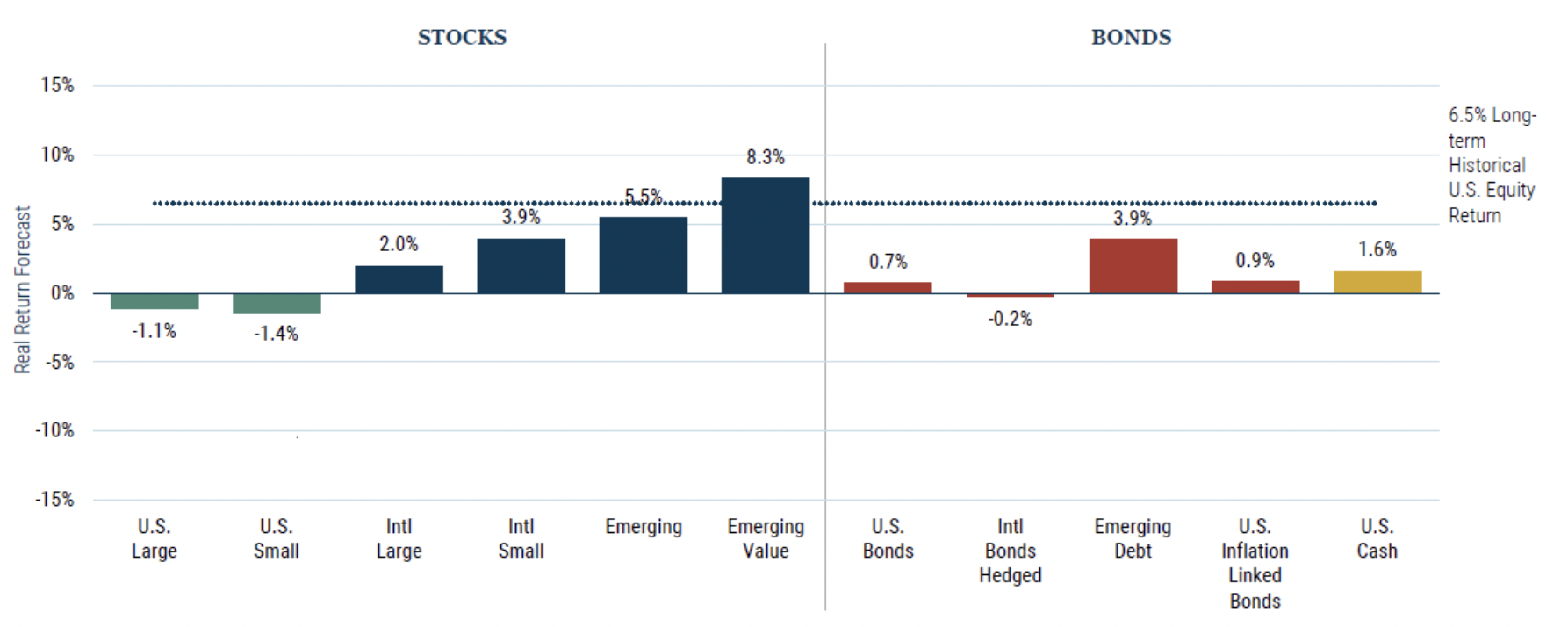

GMO 7-Year Asset Class Forecast: 1Q 2026

GMO has posted a new 7-Year asset class forecast for 1Q 2026.

10 Takeaways from the Past Three Years

It has now been over three years since GMO launched our Small Cap Quality Strategy in September 2022. During that period, the world has shifted, and we have navigated unexpected market conditions.

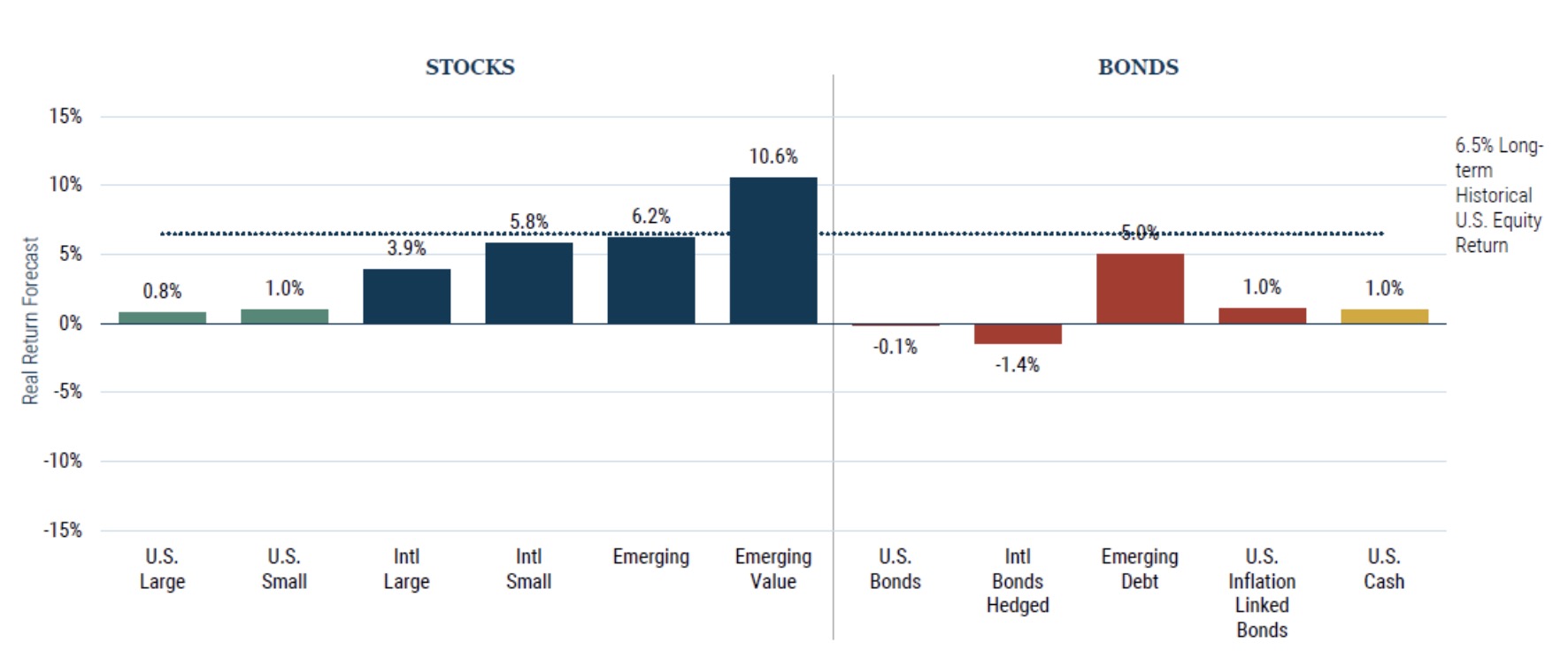

Beyond 60/40: Four Opportunities to Improve Expected Real Returns

Thanks to strong gains in markets over recent years, with many indices at or near record highs, the 60/40 default portfolio has quietly morphed into a bundle of expensive U.S. growth equities and credit exposures offering narrow spreads over Treasuries. In our view, such a portfolio is likely to disappoint investors by delivering low single-digit real returns.

Sink or Swim

There is little doubt that something unprecedented is happening in the world of AI, corporate investment, and equity returns. While AI may reshape the global economy, the surrounding investment cycle is still governed by the same macroeconomic and sentiment-driven forces that have shaped previous technological innovation and expansion periods.

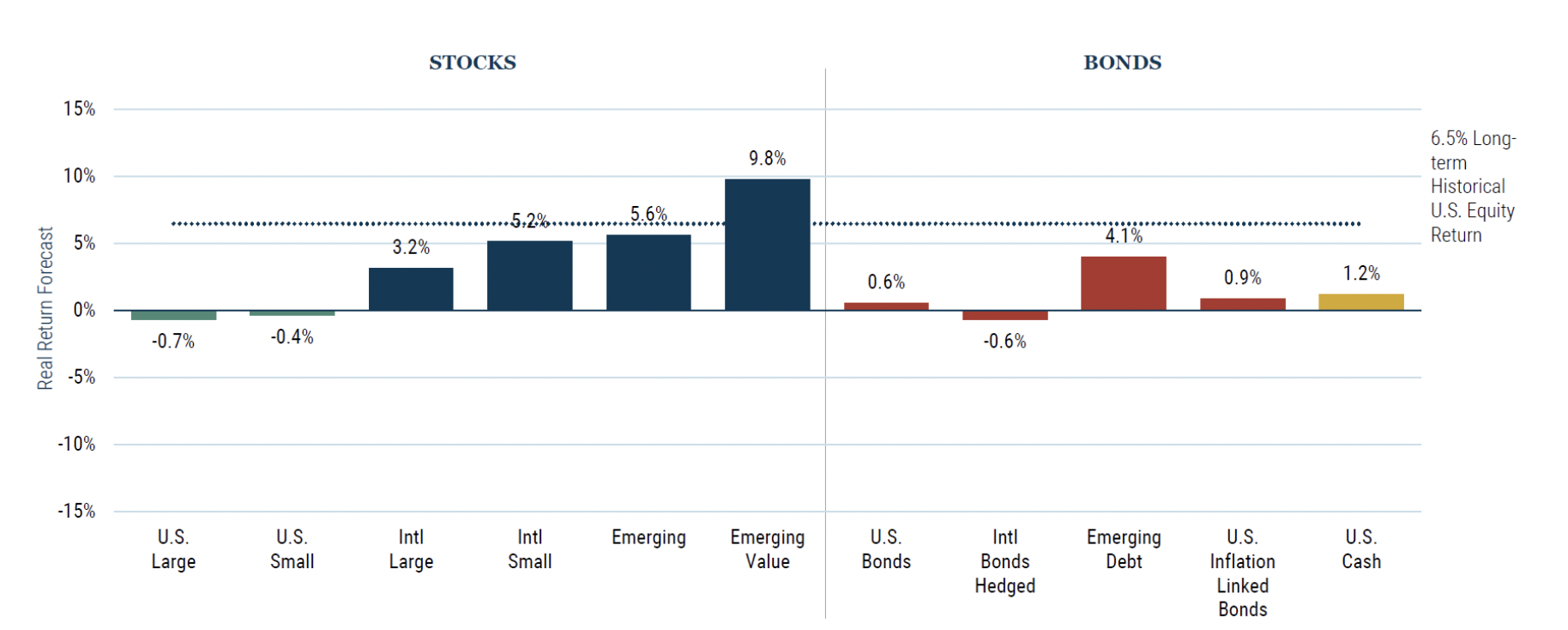

GMO 7-Year Asset Class Forecast: February 2026

GMO has posted a new 7-Year asset class forecast as of February 28, 2026.

Year-End Letter for 2025: Deep Value

Deep value stocks remain our highest conviction long-only investment idea. Globally, they trade at abnormally wide discounts and offer attractive expected returns in an environment where many equities trade at elevated valuation levels.

When the Upside Is Thin, Upgrade the Carry

At these levels, valuations are stretched, leaving investors with little potential upside and increased vulnerability to spread widening. In our view, such an environment warrants a shift toward high-quality assets.

Hype vs. High Conviction

Three years after the launch of ChatGPT 3.5, positioning around artificial intelligence-related companies has become a (perhaps “the”) critical decision for equity investors. AI investment spending by companies far exceeds current revenue generation from end-market use cases, leaving highly leveraged players facing existential risks.

2025 Year-End Letter: Event-Driven Strategy

GMO’s Event-Driven Strategy posted a +11.1% return, net of fees, in 2025. This result compares favorably to the returns of our benchmark (the FTSE 3-month Treasury returned +4.4% in 2025) and our peers (the HFRX Merger Arbitrage Index returned +9.6%) over the same period.

2025 Year-End Letter: Equity Dislocation

Equity Dislocation celebrated its fifth birthday in October, and we are delighted that this was enjoyed in the positive context of returning 15.8% gross (13.4% net) for 2025.

2025 Year-End Letter: Quality Strategy

With another year of market ebullience behind us, January seems a good time to take stock and share our thoughts on the portfolio for the years ahead.

GMO 7-Year Asset Class Forecast: January 2026

GMO has posted a new 7-Year asset class forecast as of January 31, 2026.

Valuing AI: Extreme Bubble, New Golden Era, or Both

At GMO, we have always defined a bubble as a two-standard deviation divergence of the price of any asset class above its long-term real price trend. The U.S. stock market has now been in bubble territory for a prolonged period. Sooner or later, the bubble will burst and the price will return to its historic level.

Valuation Metrics in Emerging Debt: 4Q25

Local currency rates and FX screen very cheap, while hard currency credit is rich.

GMO 7-Year Asset Class Forecast: 4Q 2025

GMO has posted a new 7-Year asset class forecast as of December 31, 2025.

Quality Opportunities in Healthcare

Despite recent results, healthcare has been one of the most compelling sectors over the past decade, consistently outpacing earnings growth in both the U.S. and across developed markets.

Artificially Inflated

As enthusiasm for artificial intelligence and its potential to reshape business models and deliver extraordinary profits accelerates, we worry that rational, disciplined investing is taking a back seat. Many investors appear to be abandoning fundamental analysis and prudent valuation in favor of paying any price to own the hottest stocks.

Improving On The Traditional 60/40 Allocation

The traditional 60/40 portfolio (60% equities, 40% bonds) has long been a standard for investors. Its limitations, especially during "lost decades," suggest the need for a fresh perspective.

Quality: The Real Deal

According to market theory, persistent outperformance shouldn’t exist. However, companies with high and stable profitability, strong balance sheets, and disciplined capital allocation have demonstrated the ability to deliver superior returns with lower risk over time.

It’s Probably a Bubble, but There Is Plenty Else to Invest In

AI looks like a classic investment bubble to us, with very high valuations and signs of rampant speculation. But we recognize that while many investors harbor fears that AI might be a bubble, they are far from sure of that fact and tend to assume the market is appropriately priced as a fairly strong prior.

GMO 7-Year Asset Class Forecast: October 2025

GMO has posted a new 7-Year asset class forecast as of October 31, 2025.

Asset Allocation Is Easy in Theory, Difficult in Practice

An advisor or allocator needs to do three things: understand the goals of their client, find different ways to earn returns for taking risks, and then take the right amount of risk to meet those goals.

Valuation Metrics in Emerging Debt: 3Q25

Local currency rates and FX screen very cheap, while hard currency credit is rich.

A Second Opinion on the 60/40 Default

The de facto “passive” allocation of 60% equities/40% bonds has proven effective at compounding wealth over time by tapping into two key risk premia: the equity risk premium earned by underwriting the risk of an economic growth shock and an inflation risk premium received for bearing the risk of surprise inflation.

GMO 7-Year Asset Class Forecast: 3Q 2025

GMO has posted a new 7-Year asset class forecast as of September 30, 2025.

EM Debt Resiliency Deserves More Credit

To make an allocation to any asset class, it’s essential to understand not just the return potential but also the underlying riskiness. In hard currency emerging debt, the primary risk is sovereign default.

Time to Take Another Look at Alternatives

Earlier this year, GMO’s Asset Allocation Team invested a sizeable 13% of its flagship unconstrained Benchmark-Free Allocation Strategy into the GMO Alternative Allocation Strategy (ALTA). ALTA provides daily liquidity and seeks to deliver equity-like returns with sensible and competitive fees, allowing for realistic return forecasts and prudent risk management.

GMO 7-Year Asset Class Forecast: August 2025

GMO has posted a new 7-Year asset class forecast as of August 31, 2025.

Many Happy (Fundamental) Returns

Although the relationship between fundamental returns and total returns after a decade is solid, valuations do matter – their impact is evident in the vertical distance between each stock observation and the diagonal line on the chart.

American Unexceptionalism

Investors today take for granted that the S&P 500 is an inherently superior group of stocks to those outside of the U.S. We believe investors who are substantially overweight U.S. large cap stocks would be well advised to rethink their stance.

3 Ways to Boost International Equity Exposure

After a mega, multi-year run of outperformance in U.S. equities over non-U.S. equities, investors have begun to question their regional equity weights.

Structured Credit: A Better Margin of Safety When Spreads Are Tight

Currently, spreads in most credit markets are at or close to historically tight levels, meaning that investors are locking in significantly lower levels of compensation than they have, on average, over the past several decades.

Frenzied Speculation in U.S. Stocks

U.S. equities experienced a sharp sell-off in early April, hitting a low point on "Liberation Day" when higher-than-expected tariffs intensified recession and inflation concerns.

Valuation Metrics in Emerging Debt: 2Q25

Local currency rates and FX screen very attractive, while hard currency credit is neutral.

GMO 7-Year Asset Class Forecast: 2Q 2025

GMO has posted a new 7-Year asset class forecast as of June 30, 2025.

Value: That Was Then, This is Now

As of June 2025, the relative valuation of the cheapest 50% of the U.S. stock market compared to the expensive half is at the 3rd percentile in our 40+ years of data.

Still A Once-in-a-Generation Opportunity

We continue to believe we are seeing a rare opportunity in EM local debt, and our conviction has been strengthened by the Trump administration’s trade and economic policies, which suggest continued dollar weakness and relative strength for EM local currencies.

Are Foreigners Changing Their Minds on India?

India has seen foreigners leaving the market for most of 2025. For this and other reasons, India has become one of the bigger shorts in our Systematic Global Macro Strategy’s equity portfolio

GMO 7-Year Asset Class Forecast: May 2025

GMO has posted a new 7-Year asset class forecast as of May 31, 2025.

Navigating a Sea of Investment-Grade Credit

In our view, using quantitative methods in a transparent, repeatable way to extract alpha through diversified factor tilts offers a compelling alternative in this new IG environment.

GMO 7-Year Asset Class Forecast: April 2025

GMO has posted a new 7-Year asset class forecast as of April 30, 2025.

Valuation Metrics in Emerging Debt: 1Q25

Local currency rates and FX screen very attractive, while hard currency credit is neutral+.

GMO 7-Year Asset Class Forecast: 1Q 2025

GMO has posted a new 7-Year asset class forecast as of 1Q 2025.

Tariffs: Making the U.S. Exceptional, but Not in a Good Way

The tariffs that the U.S. is imposing on its trading partners will bring about several costs that are important for investors to understand. Some of those costs are inherent to what a tariff is, while others stem from the fact that U.S. industrial policy has, and looks to continue to have, a huge amount of uncertainty associated with it.

Don’t Blame the Middleman

While we sympathize with consumers who have had difficult interactions with the healthcare system, we believe that much of the antipathy toward health insurers is misplaced. Their role as middlemen is a vital and increasingly important one in a U.S. healthcare system that struggles to balance between the incentives of providers and consumers.

Three Reasons We’re Overweight Japanese Equities

In a world of rich valuations and heightened geopolitical uncertainties, we believe Japanese equities are well positioned to deliver attractive returns.

A High-Quality Moment in High Yield

The value today of quality bond exposure in your high yield portfolio.

International Quality

The perfect pairing for your U.S. large-cap portfolio?

GMO 7-Year Asset Class Forecast: January 2025

GMO has posted a new 7-Year asset class forecast as of January 31, 2025.

Beyond China

We are observing a significant shift in global supply chains away from China, presenting a substantial investment opportunity. What are the reasons behind this shift?

Three Reasons to Consider Dedicated Emerging Market Debt Exposure

Some allocators may focus their search efforts on corporate credit segments or simply a portfolio that can opportunistically trade across fixed income sectors.

Valuation Metrics in Emerging Debt: 4Q24

Local currency rates and FX screen very attractive, while hard currency credit is neutral. In our Quarterly Valuation Update, we provide our Q4 assessment.

GMO 7-Year Asset Class Forecast: 4Q 2024

GMO has posted a new 7-Year Asset Class Forecast.

Bargain, Value Trap or Something in Between?

Over the last decade, U.S. large cap growth stocks have been far and away the best performing major financial asset in the world.

GMO 7-Year Asset Class Forecast: November 2024

GMO has posted a new 7-Year Asset Class Forecast.

The Future of the Inflation Reduction Act

Republicans have lashed out at the Inflation Reduction Act (IRA), a landmark package of incentives for clean energy, since it was passed two years ago.

GMO 7-Year Asset Class Forecast: October 2024

GMO has posted a new 7-Year Asset Class Forecast.

Quality: The Real McCoy

At GMO we have spent the last four decades taking a long-horizon approach to equity investing. Over time, a unique and reliable group of standout companies emerged from our research.

Don’t Miss Out

Deep value stocks are GMO Asset Allocation’s highest conviction investment idea. In a world where many stocks are being driven ever higher by positive sentiment and investor optimism, some fundamentally sound but unloved companies are being left behind, consequently trading at extraordinary discounts.

Misguided Mayhem

In the last year, we’ve written about the poor performance of clean energy, while highlighting the strong long-term outlook for the sector and the attractive valuations. These are typically the sorts of things we focus on…valuations and the long-term fundamental prospects for companies. We tend to shy away from overanalyzing short-term market dynamics.

A Second Opinion Is Just What the Doctor Ordered

In theory, growing a pool of wealth over decades – whether for a family, an endowment, or a pensioner – is a straightforward endeavor.

The What-Why-When-How Guide to Owning Emerging Debt

As GMO celebrates its 30th anniversary managing emerging debt this year, we offer our comprehensive guide to emerging debt markets. Given the tumultuous recent events – a global pandemic, defaults, repricing of interest rates, relentless strength in the U.S. dollar – we’ll focus on the Why as a starting point. Then we’ll dive into the proliferating How, covering strategies and vehicles.

GMO 7-Year Asset Class Forecast: August 2024

GMO has posted a new 7-Year Asset Class Forecast.

Small Wonders: Overlooked Japan Small Caps Poised for Resurgence

After a decade of consistent outperformance, Japanese small caps began underperforming their large cap peers in 2018, a trend that has accelerated since 2023.

Deep Value

Deep value stocks are currently our highest conviction long-only investment idea. For the avoidance of any doubt, when we talk about “deep value,” we simply mean stocks that are cheap, often screamingly so, relative to our appraisal of their fair value. We do not care about a “growth” or “value” label that has been assigned, sometimes seemingly arbitrarily, by one index provider or another.

GMO 7-Year Asset Class Forecast: July 2024

GMO has posted a new 7-Year Asset Class Forecast.

Concentrate!

Like you, we have read countless comparisons between today’s enthusiasm for all things AI and the top of the TMT bubble in 2000, with the implication being that stocks are on thin ice.

Valuation Metrics in Emerging Debt: 2Q24

Local currency rates and FX screen attractive, while credit is neutral. In our Quarterly Valuation Update, we provide our Q2 assessment.

GMO 7-Year Asset Class Forecast: 2Q 2024

GMO has posted a new 7-Year Asset Class Forecast.

FAQ: Passive Investing

In this piece, we attempt to answer a number of questions we have gotten from clients about the impacts that rising levels of passive investing may have had on the stock market.

GMO 7-Year Asset Class Forecast: May 2024

GMO has published a new 7-Year Asset Class Forecast.

The Quality Advantage in Small Cap Stocks

GMO’s Small Cap Quality portfolio managers, Hassan Chowdhry and James Mendelson, discussed why small cap valuations are attractive today and why they believe using quality is a better way of investing in the asset class.

Timing Your Swing

In September, we wrote a piece discussing some of the growing pains that have impacted clean energy in the last few years. Despite what we believe are compelling long-term growth prospects, the sector has continued to struggle over the past two quarters.

Valuation Metrics in Emerging Debt: 1Q24

Local currency rates and FX continue to screen attractive, as credit spreads transition to neutral. As we look ahead to our Emerging Country Debt Strategy’s 30-year anniversary on April 19th, our team paused to reflect on how important our valuation metrics have been in discussions with our clients.

GMO 7-Year Asset Class Forecast: 1Q 2024

GMO has published a new 7-Year Asset Class Forecast.

GMO 7-Year Asset Class Forecast: February 2024

GMO has published a new 7-Year Asset Class Forecast.

Record Highs…but We’re Still Excited

Despite strong gains in equity markets last year and year-to-date as well as indexes sitting at all-time highs, we are extremely excited about the investing landscape from an asset allocation perspective.

The Great Paradox of the U.S. Market!

In a new piece, GMO’s long-term investment strategist Jeremy Grantham reexamines the ‘great paradox’ of the U.S. market.

Emerging Debt Energy Transition

In this paper, GMO proposes a novel approach to financing emerging countries’ transitions toward cleaner energy production. Indeed, we believe a significant opportunity exists across two dimensions: greenhouse gas (GHG) emissions reduction and investment returns.

GMO Equity Dislocation

In this paper, GMO proposes a novel approach to financing emerging countries’ transitions toward cleaner energy production.

GMO 7-Year Asset Class Forecast: January 2024

GMO has published a new 7-Year Asset Class Forecast.

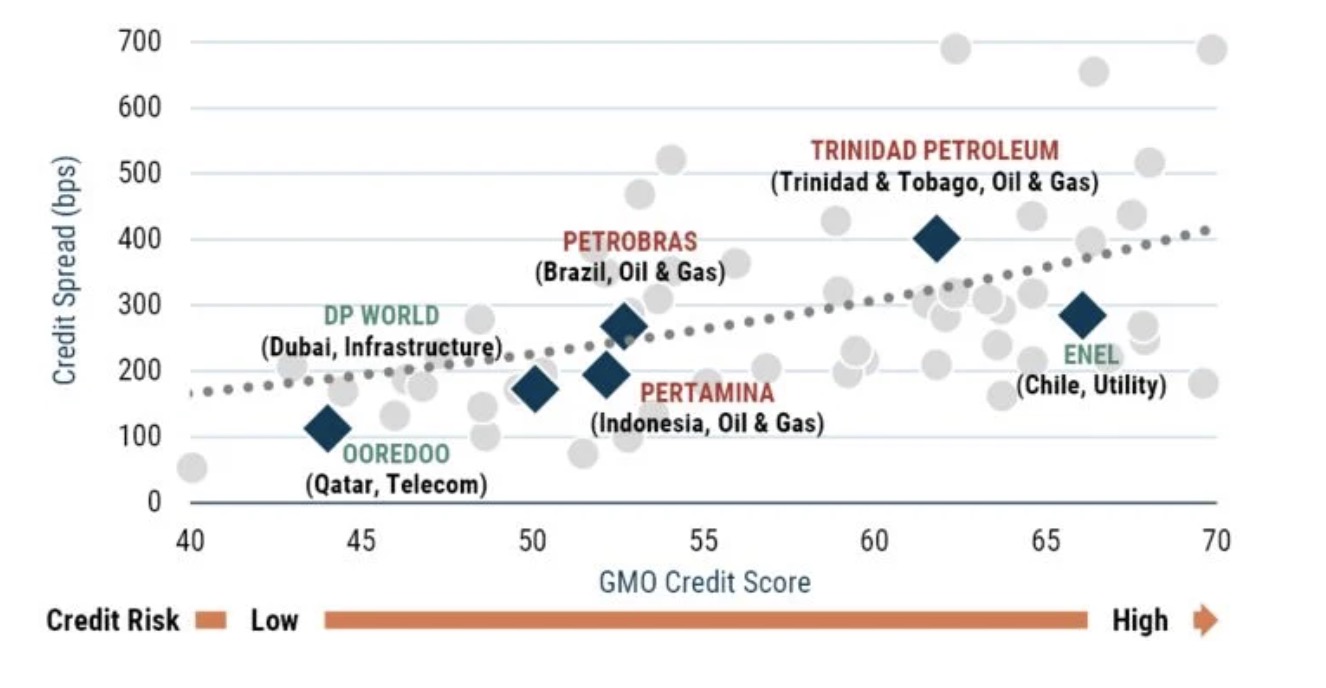

A Structural Alpha Opportunity

Ratings are an important organizing principle in credit markets, often relied upon as a summary metric of default risk. While they offer a broad categorization, investors in credit markets must rely on much deeper analysis to measure and price the actual default risks involved.

LiveCast: Quality: An Essential Ingredient to a Healthy Portfolio

Quality companies have long-term, durable business models and capital discipline, with proven track records. A strategy built around Quality that also considers valuation can mitigate risk and enhance returns.

Join the experts at GMO for a look at their robust Quality strategy that leverages four decades of Quality investing experience, blending quantitative discipline and fundamental analysis.

Emerging Local Debt

In this piece we compare two ways to take advantage of the USD’s richness versus emerging market currencies: EM equities and EM local currency debt. We believe that for relative value, diversification, and potential alpha reasons, EM local currency debt deserves a prominent place in portfolios today.

The Four 4s Behind the Compelling Opportunity in Japan Equities

Enthusiasm for Japanese equities picked up in 2023 as evidenced by the 28% rally in the

TOPIX (local) index through November.

The Quality Anomaly

As GMO launches its first ETF, it seemed like a good time to share my thoughts on the market inefficiency that the strategy seeks to exploit – the quality anomaly.

Quality: The Real McCoy

While equity styles go in and out of favor, quality companies continue to serve clients as a core holding, resilient to economic headwinds and market drawdowns. For long-term investors searching for a durable equity solution, we believe quality is “the real McCoy"

GMO 7-Year Asset Class Forecast: October 2023

GMO has published a new 7-Year Asset Class Forecast

Valuation Metrics in Emerging Debt: 3Q23

Our emerging market debt valuation metrics across all but the U.S. interest rate dimension remain unambiguously attractive. In our Quarterly Valuation Update, we provide our Q3 assessment.

Japan: The Land of the Rising Profits

Japanese profits have benefited from the prolonged deleveraging of Japan Inc. The reduction in debt coupled with exceptionally low interest rates has allowed cash flow to impact the bottom line.

GMO 7-Year Asset Class Forecast: 3Q 2023

GMO has published a new 7-Year Asset Class Forecast

Japan Equities are Compelling...But More Than 80% of Active Managers Are Underweight

Investors have been underweight Japan for decades, but conditions on the ground have changed meaningfully. Amid improving fundamentals and governance reforms, we believe it’s time to close the gap and take advantage of the attractive opportunity among small-to-mid cap Japanese companies.

Argentina and Ecuador: Testing the Boundaries of Sovereign Incorrigibility

For various reasons, both have since struggled to recoup the necessary confidence to once again borrow in international commercial debt markets.

Beyond the Landing

In our latest Quarterly Letter, Ben Inker and John Pease discuss the new economic regime, how investors can prepare for a recession, and the merits of combining high quality and cheap assets in today’s environment.

GMO 7-Year Asset Class Forecast: August 2023

GMO has published a new 7-Year Asset Class Forecast.

Turbulence on the Path to Transformation

Despite substantial growth and huge advancements in public policy support, clean energy has had an abysmal stretch in the stock market the last two and a half years.

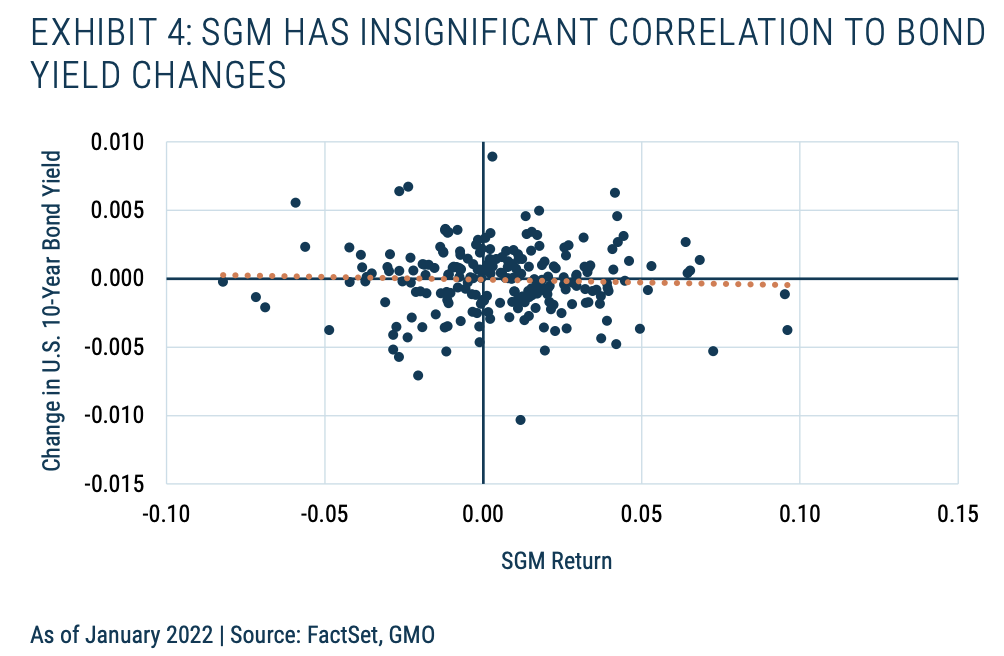

Why Is There More Volatility in My Portfolio?

We have observed increasing volatility within our Systematic Global Macro (SGM) portfolio, partly driven by an increase in volatility in our equity positions.

Does Democracy Matter for Emerging Sovereign Debt?

Russia’s 2022 invasion of Ukraine and the ensuing war have prompted new and difficult questions for sovereign debt investors.

Weighted Average Green Revenue (Wagr): Integrating Climate Solutions into Portfolio Construction

Transitioning to a green net-zero economy requires climate solutions that enable the economy to decarbonise, such as renewable energy, electric vehicles, and recycling technologies.

Estimating Value Chain Emissions for Portfolio Construction

Climate change presents a significant source of transition risk for investors as companies face increasing pressures from regulators, consumers, and shareholders to lower their carbon footprints.

Slow Burn Minsky Moments (and what to do about them)

In his latest paper, James Montier lays out a framework for spotting what he terms “slow burn Minsky moments,” or the economic vulnerabilities associated with the build-up of private sector debt.

Weighing The Risk of Sanctions in Emerging Debt

Political risks have always been present in emerging debt markets and we’ve long taken them into consideration within our overall country risk process.

Jump In The Deep End

Value equities have faced years of tough sledding, outside a run of outperformance following “vaccine day” and the lift-off from zero rates. Broadly, this has left value stocks extraordinarily cheap relative to growth. However, looking closer, the cheapest 20% of stocks – what we call “deep value” – trades unusually cheap today despite offering surprisingly attractive fundamentals.

Value Does Just Fine in Recessions

A core concern for investors contemplating taking advantage of the incredible cheapness of deep value stocks today is the potential for a near-term recession.

The Quality Spectrum: Stability in an Unstable World

War, inflation, rising rates, banking chaos, and recession are among the challenges facing markets. Investors must balance these shorter-term risks with the long-term return prospects of equities.

GMO 7-Year Asset Class Forecast: April 2023

Here are GMO’s updated forecasts for performance of various asset classes over the next seven years.

The Curious Incident of the Elevated Profit Margins

Profit margins have remained elevated in the U.S. for a decade, and in a new white paper, GMO’s James Montier examines why that has been the case, ultimately finding the culprit in fiscal deficits.

GMO White Paper: Why High-Quality Local Currency Debt Looks Attractive in EM

In a new white paper, Victoria Courmes, Riti Samanta and Mina Tomovska of GMO discuss how higher yields and similar defensiveness are a compelling combination in favor of high-quality local currency EM debt.

Agency MBS: Focus On Current Coupons

As of April 25, the Bloomberg U.S. Mortgage-Backed Security (MBS) Index was trading at an option-adjusted spread of 65 bps, which ranked in the 91st percentile since 2010. We believe moves in the asset class have been overdone and that current valuations present an opportunity.

GMO 7-Year Asset Class Forecast: 1Q 2023

GMO has published a new 7-Year Asset Class Forecast.

Valuation Metrics in Emerging Debt: 1Q 2023

Our emerging market debt valuation metrics across all but the U.S. interest rate dimension remain unambiguously attractive. In this new, compact version of our Quarterly Valuation Update, we provide our Q1 assessment and introduce summary valuation graphics to assist in quantifying expected returns.

AT1 Bonds

Born of the Global Financial Crisis, additional tier-1 securities were designed to absorb bank losses in times of turbulence and maintain financial safety at no cost to taxpayers. Despite good intentions, we’ve found AT1s to be flawed instruments that are contingently junior to common equity in practice.

AAA CMBS: Loss-remote, Liquid, And Cheaper Than IG

Fixed income spreads have widened across sectors over the past few months.

Echoes Of '08? Don't Bank On It

The GMO Focused Equity team has evaluated banks in the context of our Quality Strategy for 20 years, using both quantitative and fundamental analysis to invest in high-quality banks with healthy financials and in our opinion responsible management practices.

GMO 7-year Asset Class Forecast: February 2023

GMO 7-year Asset Class Forecast: February 2023

The Many Faces of Sovereign Default

In recent years we have witnessed a surge in sovereign bond defaults in emerging markets.

GMO 7-year Asset Class Forecast: January 2023

GMO 7-year Asset Class Forecast: January 2023.

What is Value? Methodology Matters

After a bruising 2022 for equities globally, Value stocks in the U.S. have become attractive in an absolute sense and worthy of inclusion in one’s portfolio.

Valuation Metrics In Emerging Debt: 4Q 2022

Valuation metrics across all but the U.S. interest rate dimension remain unambiguously attractive.

4Q 2022 GMO Quarterly Letter

2022 was a painful year in financial markets with almost all traditional assets delivering significant losses.

After a Timeout, Back to the Meat Grinder!

The first and easiest leg of the bursting of the bubble we called for a year ago is complete.

Memo To The Investment Committee: A Hidden Gem

Deep value offers a compelling opportunity within U.S. equities.

GMO 7-year Asset Class Forecast: November 2022

GMO 7-year asset class forecast: November 2022,

The U.S. Superbubble

The U.S. Superbubble, as Jeremy Grantham has termed it, featured the most dangerous mix of factors in modern times at the end of last year: all three major asset classes – housing, stocks, and bonds – were critically historically overvalued.

Opportunities In Today’s Environment

As the super-growth cycle is ending in dramatic fashion, we are already seeing some of the most attractive valuation opportunities in years.

Quarterly Letter 3Q 2022

Value equities are still priced for significant outperformance, globally.

GMO 7-Year Asset Class Forecast: October 2022

GMO has published a new 7-Year Asset Class Forecast.

Quality Time in Small Cap

Quality investing is an approach well suited to small cap equity.

Valuation Metrics in Emerging Debt: 3Q 2022

In this piece, we update our valuation charts and commentary, with additional details on our methodology available upon request.

Sovereign Contingent Bonds

In August 2020, as the global pandemic was straining emerging countries’ ability to make debt payments, we published a white paper – “Sovereign Contingent Bonds: How Emerging Countries Might Prepay for Debt Relief” – introducing the concept of “sovereign coco bonds,” a way for countries to structure bond agreements to allow for more flexible policy options in the face of a crisis.

Value Vs. Growth: The Unwind Continues

The world seems an increasingly uncomfortable place for traditional stock and bond investments.

Growth Investing Ain’t About the Rates

Rising rates hurt investors; claims on profits in the future are simply worth less if you discount them at a higher rate.

2Q 2022 GMO Quarterly Letter

The U.S. dollar has been on a tear in recent months, bringing it to its highest valuation versus other major developed currencies in more than 35 years.

Investing For Retirement III: Understanding And Dealing With Sequence Risk

As one of us points out relentlessly, risk isn’t a number, rather it is a notion or a concept.

Entering The Superbubble’s Final Act

Only a few market events in an investor’s career really matter, and among the most important of all are superbubbles.

Let’s Not Get Carried Away

With the recent increases in interest rates, the carry trade has had a sudden resurgence in performance, which could make it a tempting strategy for investors.

Emerging Countries Are More Resilient Than They Get Credit For

Over our decades of involvement in emerging country debt markets, we’ve witnessed many ups and downs.

Time to Jump Aboard the Value Train

The market has spent much of 2022 worrying about inflation and associated interest rate rises, and Growth stocks have certainly borne the brunt of this.

Time To Jump Aboard The Value Train

In a new piece, GMO’s Asset Allocation Team notes that even with the battering of growth stocks in 2022 there is still ample opportunity to benefit from betting on cheap value stocks versus expensive growth names.

What Does 8% Yield Pay For?

The yield of the U.S. high yield (HY) market, currently at 8.4%, has risen by over 420 basis points since the start of the year.

Inflation in Japan Should Be Cheered, Not Feared

Japan has been stuck in a low growth, low inflation (and at times, deflationary) environment.

No Stone Unturned

We strongly believe that the traditional benchmark-led approach to investing in emerging market debt can be far from optimal.

Growth Traps Snap Shut

What do Netflix, Peloton Interactive, Coinbase, and Palantir Technologies have in common?

Who Needs Tips When You’ve Got Friends Like This?

Soaring commodity prices have helped drive inflation to 8.5%, by far the highest level in the last few decades.

The Turn in Value is Just Getting Started

Over the past decade it has seemed like Value investors have been very much left on the sidelines, bemoaning rampant speculation and valuations untethered from fundamental reality, while Growth investors have, quite frankly, been living it up in some style.

Watch Out For The Balance Sheet

It’s not just interest rate changes that affect the markets, changes in the Fed balance sheet can also be a source of negative returns to equity and bond markets.

Putin's Invasion Reminds Us That We Live In A Finite World

Putin's invasion reminds us that we live in a finite world in which resource prices tend to rise.

Making Money And Reducing Risk In An Equity Superbubble

Navigating the career risk associated with bubbles (especially superbubbles) has always been tricky and is one of the biggest failings in the investment management industry.

Investment Mistakes To Avoid

As we turn over the page to a new year, there are plenty of decisions that investors will need to make.

Let The Wild Rumpus Begin

All 2-sigma equity bubbles in developed countries have broken back to trend.

Japan Equities: Entrenched Perceptions Ignore Improving Reality

Most global equity managers today are underweight Japan.

3Q 2021 GMO Quarterly Letter

This quarterly is a piece written by my Asset Allocation co-head John Thorndike. In it, he explains the rationale behind our strong preference for non-U.S. stocks despite the stellar performance the U.S. stock market has delivered over the last decade. The research behind the piece is an example of the bread and butter of our historical asset allocation analysis.

Value Traps vs Growth Traps: Value Traps Exist, But Growth Traps Are More Insidious

A new piece from the GMO Asset Allocation Team discusses value traps, growth traps and which are worse for investors.

Wounds That Never Heal

GMO Asset Allocation team presents a chart of four major U.S. equity bubbles dating back to 1929, illustrating just how long it really takes for investors to climb back to historical levels of return.

“Growth Bubble: Making Money on Companies That Make No Money”

GMO Asset Allocation Team examines the fact that although every bubble is unique, classic common threads also run through everyone.

Part 2: What To Do In The Case Of Sustained Inflation

We have a relatively sanguine view on the likelihood of inflation becoming ingrained in the system (much as it pains us to agree with the Fed). However, the dark arts of macroeconomics are notoriously tricky, and we have often talked of the need to build robust (as opposed to optimal) portfolios – effectively, portfolios that can withstand multiple outcomes.

2Q 2021 GMO Quarterly Letter

After several strong quarters for value stocks, the last few months have seen a sharp reversal in favor of growth.

Part 1: Inflation – Tall Tales And True Causes

Inflation is often a poorly understood concept, with monotheistic explanations abounding.

The Best 3-year Period For Value Vs. Growth Also Suffered Some Of Its Worst Drawdowns

The Value vs. Growth reversal, which started in earnest in the late Fall of 2020, generated exciting returns for many of our portfolios through May.

GMO 7-year Asset Class Forecast: May 2021

The GMO Asset Allocation Team has released its latest 7-Year Asset Class Forecasts through May 2021 (click to view online or see chart below).

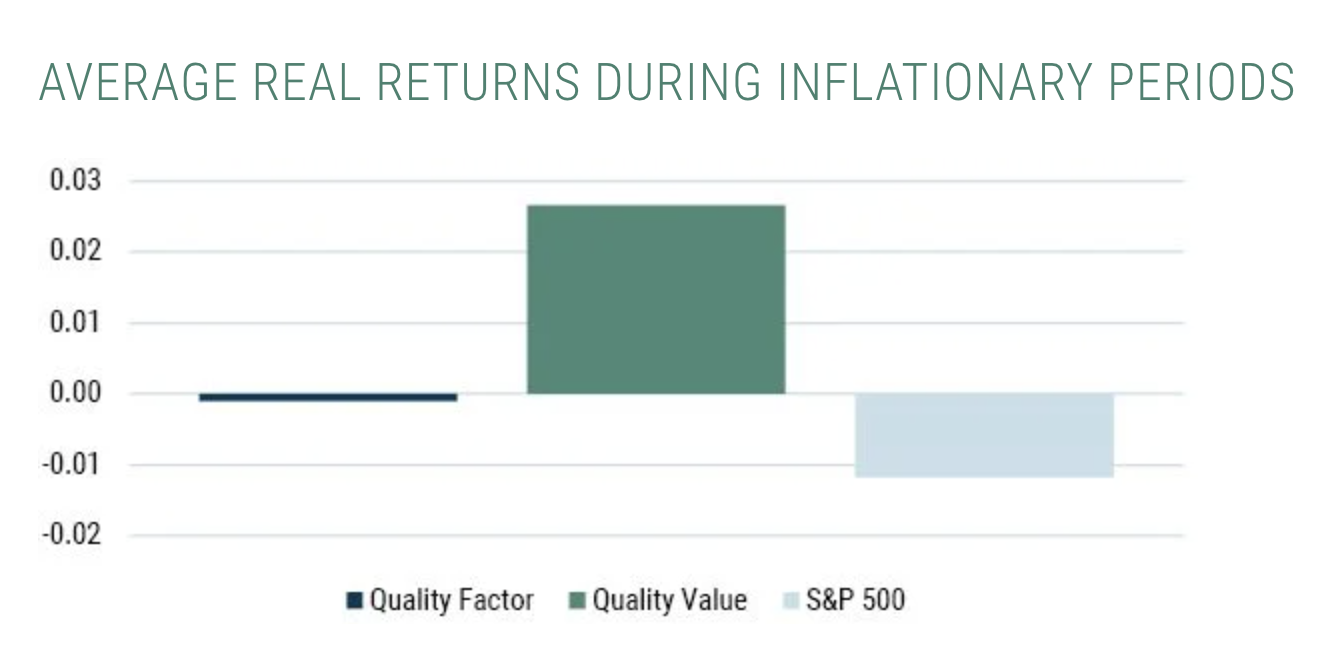

Quality Investing And Inflation

With inflation spiking as the world adjusts to the post-Covid regime, investors are naturally interested in how their portfolios might perform in an inflationary world.

There Are No Bad Assets…Just Bad Prices

In a new Insights piece, GMO’s Asset Allocation Team addresses a common response to bearishness in the current markets.

GMO Quarterly Letter: Speculation and Investment

Speculative booms provide both entertainment and outsized profits while they are happening, but they do generally burst painfully,” Inker writes. “Speculative booms provide both entertainment and outsized profits while they are happening, but they do generally burst painfully. This is particularly true in equity markets, where the demand growth is ordinarily met with increased supply from savvy capitalists. Maintaining excess demand in the face of growing supply becomes ever more difficult and eventually proves impossible.

A Year Of Investing In Quality Cyclicals

April 3rd marked the 1-year anniversary of the first investments deployed by GMO’s Quality Cyclicals Strategy,1 within a fortnight of the trough that ended 2020’s quickfire bear market.

The Duration of Value And Growth

It is commonly assumed that growth stocks are bigger beneficiaries of falling interest rates than value stocks, an assumption driven by a belief that growth stocks are much longer “duration” than value stocks due to the fact that more value in growth companies comes from relatively more distant cash flows.

Japan Value: An Island of Potential In A Sea of Expensive Assets

Global stocks and bonds are both expensive. U.S. stocks are trading at particularly elevated valuations with the CAPE ratio standing at 35x (vs. a 10-year average of less than 27x) while the Barclays Bloomberg U.S. Aggregate index offered a negative real yield at the end of February.

GMO 7-Year Asset Class Forecast: January 2021

The GMO Asset Allocation Team has released its latest 7-Year Asset Class Forecasts through January 2021.

GMO 7-Year Asset Class Forecast: 4Q 2020

GMO 7-Year Asset Class Forecasts: Value vs. growth is coming off its worst year ever.

Waiting for the Last Dance

Featuring extreme overvaluation, explosive price increases, frenzied issuance, and hysterically speculative investor behavior, I believe this [bull market] event will be recorded as one of the great bubbles of financial history, right along with the South Sea bubble, 1929, and 2000.

GMO 7-Year Asset Class Forecast: November 2020

While real return forecasts for broader markets are not particularly promising, there are some pockets that look more attractive than others. As GMO put it in the firm's recent Quarterly Letter, "Value is cheap, no matter where you look."

Don't Wait for Another Wave

With a COVID-19 vaccine rolling out and markets enjoying a post-election relief rally, credit investors may be asking “is there any opportunity left?”

Value: If Not Now, When?

GMO’s new quarterly letter to clients examines the worst 12-month performance for value stocks in history and explores how investors can profit from a period reminiscent of previous bubbles in global markets.

Tonight, We Leave the Party Like It’s 1999

History does not repeat, but it rhymes, as Mark Twain observed. As such, we are struck by the eerie and dangerous parallels between today’s markets and the markets back in 1999. Back then, Value investing and Value managers were under the gun for having underperformed their Growth brethren for too long.

Covid-19, Climate Change, and the Need for a New Marshall Plan

In a new piece – “Covid-19, Climate Change, And The Need For A New Marshall Plan” – GMO’s Jeremy Grantham discusses the impact of Covid-19 on the economy of the developed world, arguing great strides are necessary in order for the U.S. and the world to accelerate growth.

GMO 7-Year Asset Class Forecasts: 3Q 2020

We believe this is the best opportunity set we’ve seen since 1999 in terms of looking as different as possible from a traditional benchmarked portfolio.

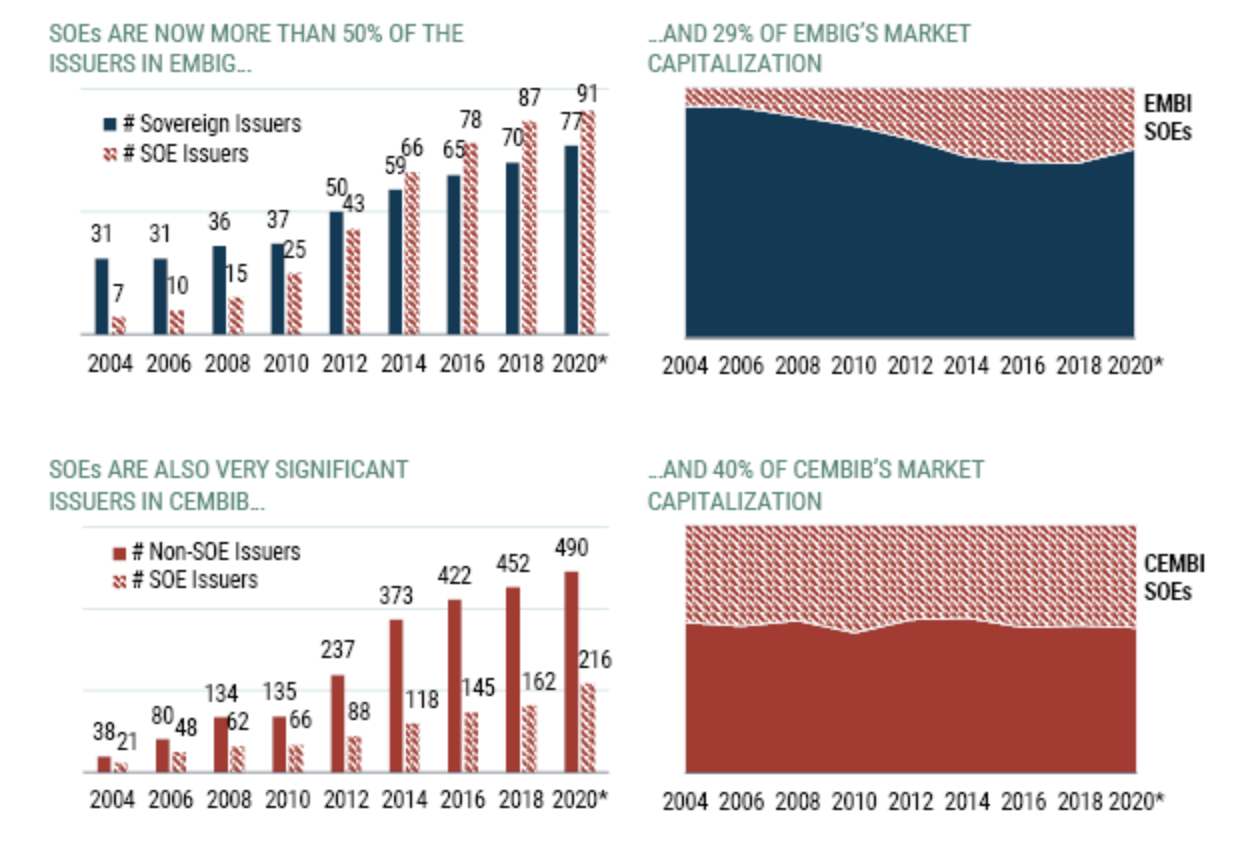

The Mystery of SOE Debt

In a new white paper, Mustafa Ulukan and Sergey Sobolev from GMO’s Emerging Country Debt Team examine the notable rise of State-owned Enterprises (SOEs) in international capital markets since the Global Financial Crisis.

2Q 2020 GMO Quarterly Letter

In a new quarterly letter to GMO cl

Sovereign Contingent Bonds: How Emerging Countries Might Prepay for Debt Relief

Emerging countries have been in the midst of a crisis that is not of their own making. A great majority of these countries are navigating the crisis fairly well.

GMO 7-Year Asset Class Forecast: Emerging Market Value Stocks Remain a Standout

The GMO Asset Allocation Team has released its latest 7-Year Asset Class Forecast through July 2020.

Reasons (Not) to Be Cheerful

Never before have I seen a market so highly valued in the face of overwhelming uncertainty. Yet today the U.S. stock market stands at nosebleed-inducing levels of multiple, whilst the fundamentals seem more uncertain than ever before. It appears as though the U.S. stock market has drunk from Dr. Pangloss’ Kool-Aid – where everything is for the best in the best of all possible worlds.

Five Reasons EM Are More Resilient Than in the Past

In a new white paper, the GMO Emerging Markets Equity Team argues that Emerging Markets in aggregate are more resilient today than in prior periods, an important consideration as investors evaluate the rebound the asset class has experienced since late March.

No Need to Bank on a Rebound

The pandemic has created an extraordinary risk/return trade-off for the shares of high quality U.S. banks. We believe there is the potential for decent returns for bank investors without improvement in the current environment, and the potential for enormous returns if the rate of change in the economy remains positive.

1Q 2020 GMO Quarterly Letter

In a new quarterly letter to GMO clients, Ben Inker, head of asset allocation discusses the current uncertainty over the market and economic outlook and the decision to significantly reduce net equity exposure in the GMO Benchmark-Free Asset Allocation Strategy. Alongside Inker’s letter, Jeremy Grantham writes in “The Virus, The Economy and The Market” ...

Introducing ‘Stressed Performing Credit'

In a new white paper, GMO Credit Opportunities Strategy co-PM Jeff Friedman looks at the Federal Reserve’s unprecedented actions in the corporate credit market amid the COVID-19 pandemic and highlights an area of the market where investors might capture attractive opportunities.

GMO 7-Year Asset Class Forecast: 1Q 2020

The GMO Asset Allocation team has released its latest 7-Year Asset Class Real Return Forecasts through the first quarter of 2020.

COVID-19 – Risk and Resilience in EM

In a new white paper from GMO’s Emerging Markets Equity Team, Amit Bhartia, Tiger Tong and Uday Tharar examine

It's Always Darkest Before the Dawn

In a new white paper from GMO’s Asset Allocation team -- "It's Always Darkest Before the Dawn" -- Ben Inker, Catherine LeGraw, John Pease and John Thorndike examine the three phases of bear markets against the backdrop of the current market environment.

Shelter In Credit

Jon Roiter reflects on a wild ride in the high-yield credit market and whether now is the time to capitalize on attractive investments in the space.

Fear And The Psychology Of Bear Markets

While it is, of course, a cliché to say that markets are driven by fear and greed, like many clichés this one contains a strong element of truth. The bad news for us humans is that within our brains, emotion appears to have primacy over cognitive function. While this may well have kept us alive and allowed our species to thrive, this uncomplicated hierarchy doesn’t necessarily work in our favour when it comes to thinking about financial markets.

An Update on the Current Environment Amid COVID-19

GMO’s Ben Inker discusses the recent turmoil in financial markets and the firm’s perspective on valuations amid the sharp declines in many asset classes.

Memo to the Investment Committee: Dare to Be Different

The conventional 60/40 portfolio of today is not going to generate the kind of returns that investors say they need. Investors must seek to embrace the terrifying concept of being different. As the ghosts of many great investors past have amply demonstrated, being different is the path to investment success. However, such advice falls into the simple but not easy category, to borrow Warren Buffett’s expression.

60/40 Portfolios Face Double Trouble Ahead

While the passive balanced portfolio (60% stock/40% bond) has outperformed more diversified allocations over the last decade, we believe investors should temper their expectations for a repeat. Two key problems lie ahead for such a portfolio.

GMO 7-Year Asset Class Forecast January 2020

Our forecasts for stocks generally improved in January as stocks declined, but they fell for bonds as rates rallied. Coronavirus and growth fears weighed on markets, pushing Value and non-U.S. stocks down most.

Chemical Toxicity And The Baby Bust

In today’s society people are choosing to have fewer children, and delaying having children at all into later, less fertile years. These two factors have driven fertility rates below replacement level in most of the world, but a crucial third factor gets little attention and is having a profound impact on fertility: toxicity. The economic and social ramifications will be severe.

How Higher Ratings Are Changing Emerging Debt

By moving our USD emerging debt strategy benchmark to the diversified (issuer-capped) version of J.P. Morgan’s EMBIG benchmark, we will limit our exposure to the ballooning issuance of low-return-potential, opaque countries. Our objective is to retain the “high dividend sovereign equity” nature of this asset class for our investors...

7 Year Asset Class Real Return Forecasts

Emerging market value stocks are the most attractive asset class for two reasons, explains GMO's John Thorndike.

Health Insurance Companies: Rhetoric vs. Reality

The policy proposal of "Medicare for All" calls for nationalizing the U.S. health insurance system. While this is a politically unlikely outcome, the stock prices of the private sector Managed Care insurance companies have suffered as rhetoric heats up.

Climbing the ESG Learning Curve in Emerging Markets

ESG integration is best used as a tool to improve portfolio returns and/or reduce risk. While usually thought of as a company-level concern, material ESG data can be very useful at the country level as well, especially in emerging markets. ESG signals are only as good as the quality of their inputs.

Emerging Market Stocks: Getting Comfortable with the Uncomfortable

In a new GMO Insights piece titled “Emerging Market Stocks: Getting Comfortable with the Uncomfortable,” asset allocation team member Rick Friedman looks at how lackluster emerging market equity returns in recent years have led many investors to write off the asset class, but GMO “humbly suggest(s) investors get more comfortable owning the uncomfortable.”

Shades of 2000

The years leading up to the 2000 stock market bubble were extraordinary and unprecedented. They caused unique pain to the portfolios of valuation-driven investors. The valuation extremes, though, created the greatest opportunity set for valuation-driven investors since the Great Depression.

Bigger's Been Better

Ben Inker highlights the multiple benefits large U.S. companies enjoy when compared with smaller ones, and examines whether the conditions that have caused this situation will remain in place.

GMO’s 7-Year Asset Class Forecasts: Higher Prices and Lower Rates Dim Expectations

“GMO’s 7-Year Asset Class Forecasts for both stocks and bonds have generally declined in 2019, predominantly due to strong appreciation in asset prices,” said Rick Friedman from GMO’s Asset Allocation team.

Risk and Premium - A Tale of Value

Investors who have watched the U.S. stock market over the last decade might be wondering whether the appeal of value stocks has been whittled away by a long run of underperformance.

EM Illiquid Is Not the Same as EM Small Cap - And That’s a Good Thing!

Small cap stocks within emerging markets have outperformed large cap stocks by around 0.5% annualized since January 2000,” George writes. “However, illiquid stocks (regardless of capitalization) have outperformed large cap stocks by around 3%. This illiquidity premium is related to, but not the same as, the small cap premium.

Gaming out Sovereign Default When China Is a Major Creditor

Game theory is a useful framework for modeling aspects of sovereign debt recoveries, given that it models the interactions among debtors and creditors in the lending/borrowing "game." While there is a long-established set of precedents for Paris Club (U.S. & European) and multilateral (IMF, etc) creditors’ actions, we still have little available information about how China will act in debt negotiations.

Alphabet and the DOJ

Shares in Alphabet have come under a good deal of pressure over the last year as investors process the implications of increasing regulatory scrutiny, culminating in reports this month that the U.S. Department of Justice (DOJ) is preparing for an antitrust probe into big tech.

7-Year Asset Class Real Return Forecasts

We continue to favor emerging markets equities, particularly emerging market value, and see some appeal in international value stocks. In the U.S., small-cap value is a pocket that has become quite attractive to us.

Value Investing - Bruised by 1000 Cuts

The duration and magnitude of value’s recent underperformance has caused many to ask once again if value investing is no longer effective. While it is possible that secular shifts have helped to compress value’s premium relative to its long-term history, we believe most of the recent decline can be traced to more transitory factors.

Stop Worrying about Your Portfolio

Investors have a tendency to obsess about their investment portfolios. On the surface, this is a perfectly reasonable focus given results in the portfolio are a crucial determinant of success for whatever purpose the portfolio is there to serve.

7-Year Asset Class Forecasts: Outlook Muted After Strong First Quarter

Our forecasts have come down due to the extraordinary performance of equities and credit in the first quarter. However, we continue to find pockets of opportunity across equities: we believe value stocks are trading at attractive levels globally, and emerging markets value stocks are priced to deliver more than 7% above inflation.

Thinking Outside the Box

Lucas White and Jeremy Grantham examine the benefits of investing in a climate change strategy, including diversification, protection from climate risk, inflation protection and the ability to invest in growth-oriented companies at a discount.

Why Does Everyone Hate MMT?

In a new Viewpoints piece on GMO's website, James Montier examines Modern Monetary Theory (MMT) and the negative view on it taken by many highly-regarded economists.

Closing the Gulf: How the GCC Countries Fit into our Emerging Debt Investment Process

On January 31, 2019, J.P. Morgan, which manages the EMBI suite of emerging market bond indices, added five new countries of the Gulf Cooperation Council (GCC)1 to the external debt benchmarks. This addition represents the largest ever one-time adjustment to the index that our foreign currency sovereign debt funds have historically used as a benchmark.

Total Factor Productivity Growth = Totally Ficiticious Pretentious Garbage

In a new white paper on GMO’s website -- “Total Factor Productivity Growth = Totally Fictitious Pretentious Garbage” -- James Montier and Philip Pilkington take aim at the argument that stagnating incomes are to be blamed on poor productivity growth.

GMO Quarterly Letter

In a new quarterly letter to GMO’s clients, head of asset allocation Ben Inker looks back on a confounding 2018 and discusses how to assemble a portfolio of attractive assets looking ahead.

Is the U.S. Stock Market Bubble Bursting? A New Model Suggests “Yes”

GMO's Martin Tarlie argues in a new white paper that the U.S. stock market was a bubble from early 2017 through much of 2018, and that the bubble started to deflate in Q4 2018, despite strong fundamentals.

7-Year Asset Class Forecasts Increase After Steep Market Declines

Steep declines across most asset classes in the second half of 2018 resulted in significant increases in forward-looking returns.

Crisis and Opportunity in Emerging Debt

Periodic bouts of volatility are a fact of life for emerging market investors, but for those who can ride out such periods of real or perceived crisis, dollar-denominated EM sovereign debt can offer compelling returns.

Quality Equities: The Solution to Today’s Equity Conundrum

Ten years into a bull market, the conventional wisdom is that U.S. stocks are richly valued based on most well-cited metrics. Fortunately, solid investment opportunities remain in places that some value investors may find surprising. This is why the GMO Quality Strategy remains fully invested in equities. We invest globally, yet the portfolio holds primarily U.S. domiciled companies.

The Late Cycle Lament: The Dual Economy, Minsky Moments, and Other Concerns

Overoptimism and overconfidence are two well-known psychological traits of our species. They are particularly dangerous in the late stages of an economic cycle where these terrible twins result in investors overestimating return and underestimating risk – a potentially lethal combination of errors.

GMO's 7-Year Asset Class Forecasts Still Favor Emerging Markets Over U.S. Stocks

Our forecasts continue to favor emerging markets in both the equity and credit markets, says GMO Asset Allocation team member John Thorndike. As of the end of September, the spread between our forecasts for emerging markets equities and large cap U.S. stocks was nearly 8.5%. You have to go back to 2003 to find a wider spread in favor of EM.

Emerging Corporate Debt Fundamentals - How High Is The Risk?

State-owned enterprises (SOEs) account for much of the emerging market corporate debt universe, and with fundamentals weak relative to history, there are concerns about the impact of rising rates on these corporations. In a new GMO Emerging Debt Insights, Mustafa Ulukan explores these concerns.

The Race of Our Lives Revisited

In a new white paper on GMO’s website, Jeremy Grantham updates his discussion of the threats posed by climate change, population growth and increasing environmental toxicity, and his perspective on the role investors can play in combating these threats. In “The Race of Our Lives Revisited” Grantham summarizes the current state of affairs and the likely impact on the future ability to feed the 11 billion people projected to live on Earth by 2100.

Emerging Markets—No Reward Without Risk

Emerging equities are more volatile than developed market equities. This owes little to the volatility of emerging stock markets in local terms and much more to the strong positive correlation between their local stock markets and movements in their currencies. The spring of 2018 was a classic example of this, with US dollar strength driving significant emerging weakness.

Multi-Asset Class Strategies: How Do I Use Thee? Let Me Count The Ways.

Not too long ago, investors, consultants, and advisors in the asset management field struggled with the role of Multi-Asset Class (MAC) strategies. They were perceived as misfits, given their cross-asset mandate and their dynamic nature. Today, however, they are utilized and embraced in all sorts of different settings.

Emerging Debt in a Rising Interest Rate Environment

"A rising global interest rate environment is once again leading to volatility in the emerging debt markets,” writes GMO’s Carl Ross in a newly-published Emerging Debt Insights piece. As the US 10-year Treasury has risen to the 3% neighborhood, benchmarks of emerging country bonds, both in hard currency and local currency, have fallen.

Is Investing Starting to Get Difficult Again?

In a new quarterly letter to GMO's institutional clients, head of asset allocation Ben Inker reflects on a change in the investment environment in the first quarter, characterized by a rise in volatility and a significant shift in the correlation between stock returns and bond returns ("Is Investing Starting to Get Difficult Again? I Hope So").

GMO's 7-Year Asset Class Forecasts Still Favor Non-US Markets

Most global equity markets declined in the first quarter despite the corporate sector generally reporting reasonable fundamental data. As a result, GMO's 7-year equity forecasts mostly improved over the first quarter. Even with these improvements, International and U.S. equities are still forecast to have flat to negative real returns over the next 7 years, with Emerging equities remaining an exception, forecast to have a positive real return of 1.9%.

Russia: A Riddle, Wrapped in a Mystery, Inside an Enigma

In the latest GMO Emerging Equity Insights, Arjun Divecha, head of GMO's Emerging Markets Equity team and a member of the GMO Board of Directors, shares his thoughts on the recent selloff in Russian equities.

Go West, Young Investor…But Go Wisely: Intelligent Investing in an Unintelligent Landscape

Investing requires bearing risk to reap rewards, but there is no definitive causal relationship here. Just because you might be willing to pack up your wagon and head off into the sunset doesn’t ensure you’ll be rewarded with wealth. Today investors should be particularly diligent in assessing risk before setting off on any journey.

ESG: Improving Your Risk-Adjusted Returns in Emerging Markets

Emerging market economies are more vulnerable to the ill effects of ESG issues, but because transparency into such issues in these regions has been lacking, and because investors may have different understanding of risks and opportunities than ESG ratings agencies, integration has been difficult," the white paper says.

Contemplating Value in Emerging Markets Intelligently, with a Little Help from Ben Graham

In the latest GMO Emerging Equity Insights, titled “Contemplating Value in Emerging Markets Intelligently, with a Little Help from Ben Graham” Amit Bhartia and Matt Seto revisit Ben Graham’s principles of value investing and extrapolate them to investing in emerging markets.

Trade Wars are Bad, and Nobody Wins

Inker, the head of GMO's asset allocation team, warns that a full-blown trade war "is probably more dangerous for investors at this time than at any other time in recent history."

The Value of Short Volatility Strategies

The authors believe that with today’s heightened valuations across global equity markets, and volatility no longer cheap, now is a fitting time for investors to take a careful look at put writing strategies and consider swapping a portion of their traditional equity exposure for index put-writing. The piece concludes with a “Special Topic” dedicated to examining the recent VIX Blowup.

GMO Quarterly Letter

In a new quarterly letter to GMO's institutional clients, head of asset allocation Ben Inker considers the hypothetical question posed by chief investment strategist Jeremy Grantham in his third-quarter 2017 letter, "What should you do if you are tasked with managing Stalin's pension portfolio?" ("Don't Act Like Stalin! But maybe hire portfolio managers that do?").

The Advent of a Cynical Bubble

James Montier, a member of GMO’s Asset Allocation team, has just published a new white paper -- "The Advent of a Cynical Bubble” – examining the nature of the bubble we find ourselves in, noting the concept that “the US equity market is obscenely overvalued can hardly be news to anyone.”

7-Year Asset Class Forecasts

The GMO Asset Allocation team has released its latest 7-Year Asset Class Forecasts, which show emerging market equities are likely to generate the best real returns over the next seven years, though investors should temper their expectations for those returns.

Bracing Yourself for a Possible Near-Term Melt-Up

In the latest GMO Viewpoints -- "Bracing Yourself for a Possible Near-Term Melt-Up" -- Jeremy Grantham has a warning for bubble watchers: the next phase in this long-running bull market may be even more dizzying gains. Among the factors Grantham considers are the acceleration of price, increasing concentration like that in tech "winners," outperforming quality and low beta stocks and the role of the Fed in recent bubbles.

GMO Quarterly Letter

In a new quarterly letter to GMO's institutional clients, head of asset allocation Ben Inker discusses why investors should be thinking about the risks of surging inflation, even if such a surge may not be inevitable or even probable. Chief investment strategist Jeremy Grantham considers the current market environment and how to most rationally take risk with the ultimate stakes on the line.

FAANG SCHMAANG: Don’t Blame the Over-valuation of the S&P Solely on Information Technology

A small group of technology stocks have recently delivered stellar returns. Facebook, Apple, Amazon, Netflix, and Alphabet (Google), the so-called “FAANG” stocks, are up 36% on average year to date through September. This superlative performance, in such a narrow group of large cap names, has led many to raise questions about the current valuation of the S&P 500, its sector composition, and comparisons to other markets.

China’s Rising Presence in Emerging Debt Markets

Countless articles have been written in the past 10 years predicting (or warning) of China’s imminent financial demise, with the number of articles accelerating in recent years amid China’s debt build-up in the post Global Financial Crisis period. Investing on the basis of a “China collapse” view of the world would likely have resulted in more risk-averse portfolios in the emerging debt space and, hence, lower returns in recent years.

The Good Thing About Climate Change: Opportunities

In a new white paper, “The Good Thing About Climate Change: Opportunities,” GMO’s Lucas White and Jeremy Grantham discuss the growing problem of climate change, the exciting investment possibilities in companies combating that peril and the best ways for investors to approach the opportunity.

The S&P 500: Just Say No

James Montier and Matt Kadnar, members of GMO’s Asset Allocation team, have just published a new white paper -- “The S&P 500: Just Say No” -- warning of the risks to investors throwing in the towel on valuation, diversification and active management in favor of a passive allocation to large-cap U.S. equities.

Merger Arb and Unicorns

Imagine an asset class with a decently positive expected rate of return, little to no equity beta, and little to no interest rate duration. A unicorn? We think not.

Quarterly Letter

Emerging Value and Margin of Superiority by Ben Inker and Why Are Stock Market Prices So High? by Jeremy Grantham

Revisiting the Traditional Emerging Market Equities Allocation Framework

Bhartia, a portfolio manager on GMO’s Emerging Markets Equities team, and his colleague Mehak Dua, explore the benefits of combining a risk-based approach with valuation in an asset class that has grown considerably more complex over the last three decades.

I Do Indeed Believe the US Market Will Revert Toward Its Old Means – Just Very Slowly

Jeremy Grantham explains why he believes that the high equity prices in today’s market have some staying power, and expects it will take much longer than usual for the power of mean reversion to draw profit margins and price earnings ratios back to historical norms.

Whiplash: On Value, Growth, and Ignoring the Fundamentals

After a decade of lagging relative returns, value equities delivered impressive performance in 2016, outperforming growth stocks by 10% in the US.

Qatar: A Test Case for the “America First” Doctrine?

Saudi Arabia and the United Arab Emirates effectively excommunicated Qatar from the Gulf Cooperation Council (GCC); they cut off all transportation links, forced Qatari citizens in the GCC to leave, and closed their airspace to Qatar Airlines’ flights to Europe and the US. The stated goal of these measures is to force the Qatari government to stop allying with the government of Iran and to stop supporting certain political/terrorist groups, like the Muslim Brotherhood, in Egypt and across the Middle East. However, if the Qataris do not accede to their demands, their objective may become to cause regime change in Qatar. The US has a major military base in Qatar and so has a stake in the outcome.

America Is Great. Home Country Bias Ain’t.

Investors have a tendency to prefer home cooking when it comes to their stock portfolios. In the latest GMO Asset Allocation Insights, Rick Friedman writes that US-based investors are paying steep prices for domestic equities. but straying from their home market presents more attractive prices.

GMO Quarterly Letter

In a new quarterly letter to GMO's institutional clients, head of asset allocation Ben Inker addresses "perhaps the most common question I get from clients: What keeps you up at night?" ("Up At Night").

The Reserve, Part II The US Dollar: Still the Cleanest Dirty Shirt?

Is the dollar losing its grip on its status as the world’s reserve currency?

For Whom the Bond Tolls: Low Rate Beneficiaries in a Rising Rate Environment

Sluggish growth and aggressive central bank actions following the Global Financial Crisis pushed interest rates down to unprecedented levels, even negative outside the US, for longer than many would have expected.

What are the Risks and Opportunities?

Amar Reganti, a member of GMO’s Asset Allocation team, examines “ultralong” debt in his new white paper “The 100 Year: A Take on the Century Bond.” The recently confirmed Secretary of Treasury, Steven Mnuchin, has indicated that he would "possibly review the issuance of a 100-year bond as an instrument used to achieve that maturity extension."

The Deep Causes of Secular Stagnation and the Rise of Populism

In a companion paper, “Six Impossible Things Before Breakfast,” we present evidence that asset markets are generally priced for “secular stagnation,” and argue that this requires a number of extreme assumptions on the part of investors.

Six Impossible Things Before Breakfast

One of the great joys of working at GMO is the freedom to disagree. Indeed, many moons ago when Ben Inker first approached me about joining GMO, he told me that, having read my work, he believed we were very much philosophically aligned.

Beware The Wu Wei of Passive Bond Investing

Passive “doing-by-not-doing” is no way to run a bond portfolio today.

Emerging Markets Can Trump US Policy Rhetoric

We believe the consensus view of a Trump presidency translating into a blanket “stay clear of ” investing in emerging markets is overly simplistic. Our analysis of President Trump’s proposed policy of trade protectionism suggests that the impact on emerging markets is more nuanced – the vulnerability of these markets is significantly lower today than it was five years ago...

Emerging Markets: Value Trumps Headlines

Some investors are swearing off emerging markets in the age of President Trump. That’s a mistake, says Rick Friedman, a member of GMO’s Asset Allocation team. To these bears, “the double whammy of stimulative US fiscal policies coupled with possible protectionist barriers, makes emerging investments less attractive,” Friedman writes in a new piece “Emerging Markets: Value Trumps Headlines.”

Getting "The Biggest Bang For The Buck" In Target Date Plans

Can target date plans be better? That’s the question many defined contribution plan sponsors are asking and a new paper from GMO’s Peter Chiappinelli and Ram Thirukkonda argues yes, they can.

The Reserve: The Dollar, the Renminbi, and Status of Reserve

An Investment Only a Mother Could Love: The Case for Natural Resource Equities

Lucas White and chief investment strategist Jeremy Grantham highlight the long-term investment opportunity in natural-resource equities.

The Duration Connection

Immigration and Brexit

In a commentary today, GMO chief investment strategist Jeremy Grantham addresses risks and potential unintended consequences of the U.K.'s Brexit decision.