Key Points

- Investors appear to be shying away from risk, resulting in a pullback in stocks. We view this as temporary, although patience will be required and sharper downturns could occur within the ongoing bull market.

- "Hard" economic data hasn’t accelerated to the same degree as "soft" data (confidence/survey-based), and some convergence is expected. Political and geopolitical uncertainty abounds, while the Fed has begun to address the slow draining of its balance sheet.

- Global earnings have aided stock market gains, but the expectations bar is getting higher to hurdle. The next several weeks should show whether gains will persist or if expectations may have gone too far.

Risk and reflation rerating

Investors appear to be taking another look at the risks they are willing to take, while also considering whether the reflation story may not develop as hoped. Reflation is the process of getting economic growth and price broadly back to pre-recession levels. While progress has been made, growth is still not accelerating. First quarter real gross domestic product (GDP) is forecasted to come in around a 1% annualized level according to Bloomberg. Add in disappointment with the political developments—the hoped for stimulus coming from Washington is at least delayed; the Federal Reserve is talking about reducing its balance sheet; and geopolitical tensions are rising—and you have a good mix for investors to pare back some risk. Stocks have trended modestly downward, while more cyclical areas of the stock market have struggled at the expense of more defensive areas. We've also seen yields reverse course after surging on hoped for fiscal stimulus and rising economic growth.

Yield reversal indicates paring back of risk

Source: FactSet, Federal Reserve. As of Apr. 10, 2017.

We don't see this as the beginning of the end of the bull market, however. Economic growth is still positive, and business and consumer confidence surveys continue to be quite strong. Additionally, as we head into the heart of earnings season, expectations are for a strong season, with FactSet reporting that analysts are expecting first quarter S&P 500 earnings to rise 9.1% over a year ago, which would be the highest growth since 2011. A risk, however, is that the bar has been set too high, which could make it harder to achieve upside surprises. But solid earnings and economic growth should enable the long running bull market to continue. Investors will likely have to don their patience and discipline caps, as there could be further pullbacks. Geopolitical tensions are also threatening to shake the market, with North Korea testing weapons and Syria’s atrocities; with the U.S. response to both gaining worldwide attention. The world doesn't yet have a good idea how the current administration, or other global leaders, will handle these tensions, so bouts of volatility should be expected. In fact, for the first time in over 100 days, the CBOE Volatility Index (VIX) moved above its 200-day moving average.

Economic picture mixed but still positive

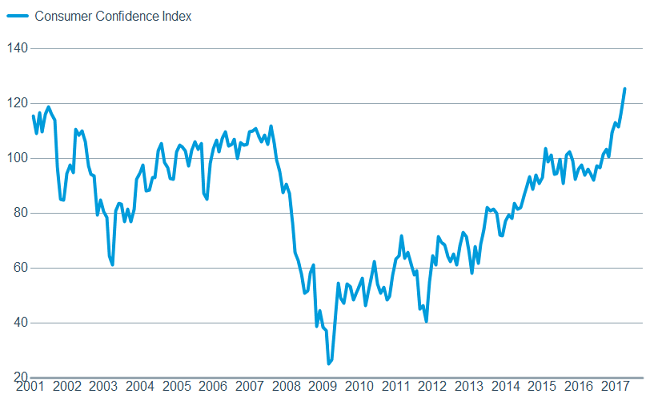

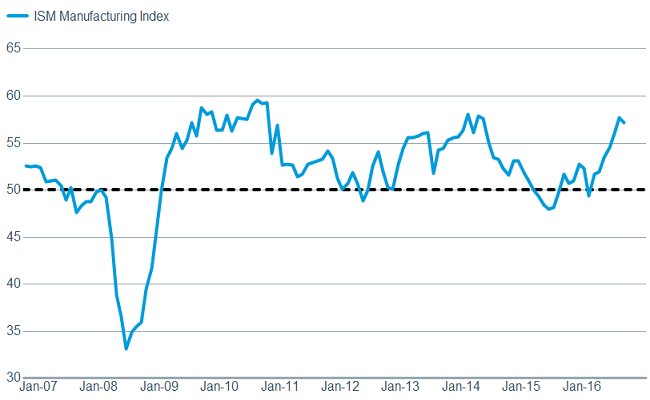

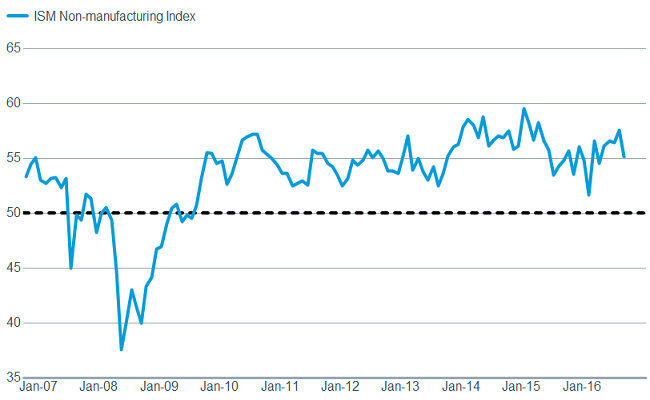

Frustration with the lack of meaningful acceleration in the "hard" data persists although the labor market continues to look solid—notwithstanding the modestly weaker-than-expected March labor report, which likely had weather as a culprit. After ticking slightly higher, jobless claims again fell last week and remain historically low; while the ADP employment report showed a surprising 263,000 private sector jobs were added. As noted, the jobs report from Department of Labor was disappointing with only 98,000 jobs being added, however the unemployment rate fell to 4.5%, the lowest level since 2007. We have highlighted that we expect job gains to moderate as the unemployment rate falls, due largely to there being fewer qualified workers available for hire. However, corporate and consumer caution persists, despite elevated sentiment readings, likely due to policy uncertainty in the aftermath of the failure of healthcare reform. As seen below, the Conference Board’s measure of consumer confidence remains elevated, while both Institute for Supply Management's indexes (manufacturing and services) remain firmly in territory depicting expansion.

Consumer confidence remains elevated

Source: FactSet, Conference Board. As of Apr. 10, 2017.

As does business confidence

Source: FactSet, Conference Board. As of Apr. 10, 2017.

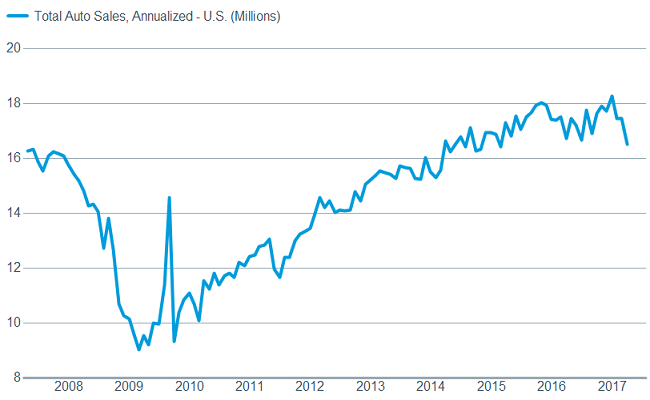

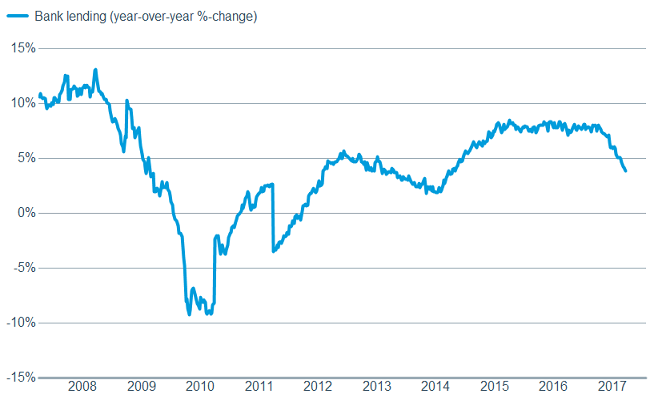

Two areas of concern are auto sales and bank lending; both of which have been weak; indicating a continued disconnect between elevated optimism and pro-growth action.

Source: FactSet, Bloomberg. As of Apr. 10, 2017.

While bank lending is sluggish

Source: FactSet, Federal Reserve. As of Apr. 10, 2017.

For growth to accelerate, we need to see optimism translate into action. Forward-looking commentary from companies during earnings season may be a tell on how this divergence narrows.

Washington not helping

Investors are also mulling both monetary and fiscal policy uncertainty. The meeting minutes from the March Federal Open Market Committee (FOMC) meeting showed that they are talking about reducing the Fed's balance sheet, while also noting that several members were concerned about valuations in certain segments of the stock market, which seemed to unnerve investors a bit. We are less concerned. The Fed continues to express caution and caveat all potential further normalization moves within the context of an improving economy. Inflation doesn’t appear to be a major concern right now, which should enable the Fed to continue to be slow and deliberate with both rate hikes and balance sheet reductions.

Slowness, however, is not so appreciated down the street in DC; with investors expressing disappointment about the lack of progress on promised tax reform. Leaving for the Easter break without a proposal for either healthcare reform or tax reform in either house of Congress doesn't bode well for any action in the near term. We increasingly believe it will be late this year or into 2018 before we see anything done on the tax reform front, but we remain optimistic that it will get done, potentially providing a boost to stocks. And although somewhat overlooked, regulatory reform is already acting as a tailwind for business, and in turn stocks.

Earnings season: what we're watching

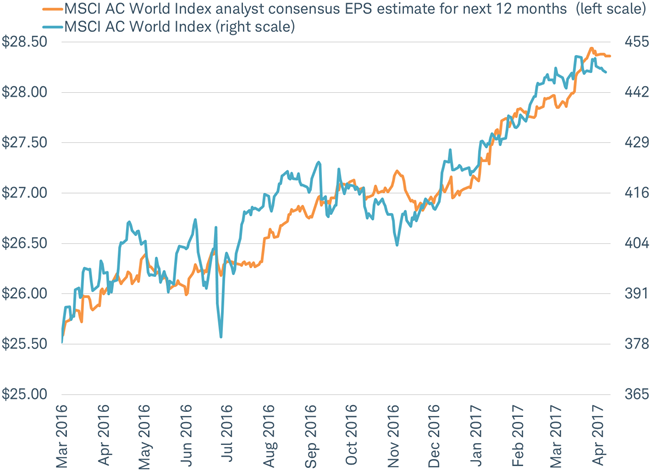

It's not just in the United States that earnings are starting to take center stage. The widely-looked for political and geopolitical risks haven't severely impacted the markets—with the earnings outlook likely a major driver. Analysts have not been broadly incorporating into their estimates potential positives (U.S. tax reform, U.S. infrastructure spending) or potential negatives (trade barriers, European break-up costs) from policy changes. Instead they have been focused on the acceleration of global economic growth. In fact, stocks have been rising in lock step with earnings expectations, as you can see in the chart below.

Stocks have been tracking the earnings outlook, not politics

Source: Charles Schwab, Factset data as of 4/11/2017.

This suggests that the biggest risk to the global equity rally may be just ahead in the coming weeks, with the delivery of the first quarter earnings reports. We think the news will be good. But will it be good enough to sustain gains in the stock market which has already priced in a solid global earnings' recovery? Watch the key profit trends, including the outlook for revenue growth and cost pressures on materials and labor.

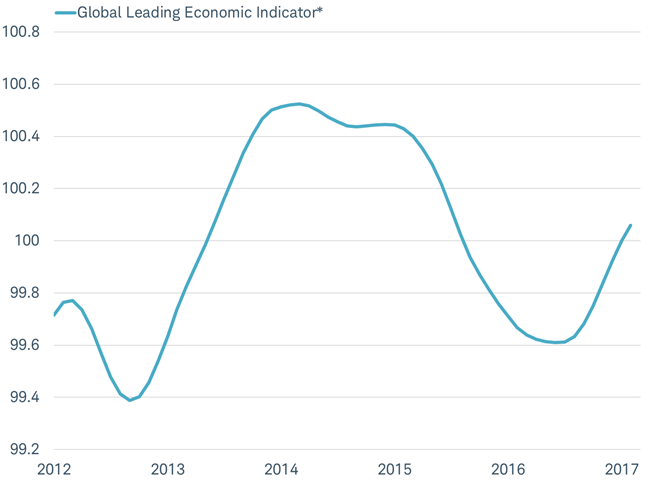

Revenue growth is improving. After peaking three years ago and suffering a long slide thereafter, the widely-watched global index of leading economic indicators (LEI) from the Organization for Economic Cooperation and Development (OECD) has rebounded in recent months, pointing to improving global economic growth.

Global leading economic indicator on the rise after a long slide

*OECD Total Composite Leading Indicator seasonally-adjusted amplitude-adjusted.

Source: Charles Schwab, Bloomberg data as of 4/12/2017.

The combination of real growth and reviving global inflation may push global nominal GDP growth over 5% this year—the strongest pace since 2011. Since sales growth for global companies tends to track nominal GDP, 2017 may deliver the best sales growth in years.

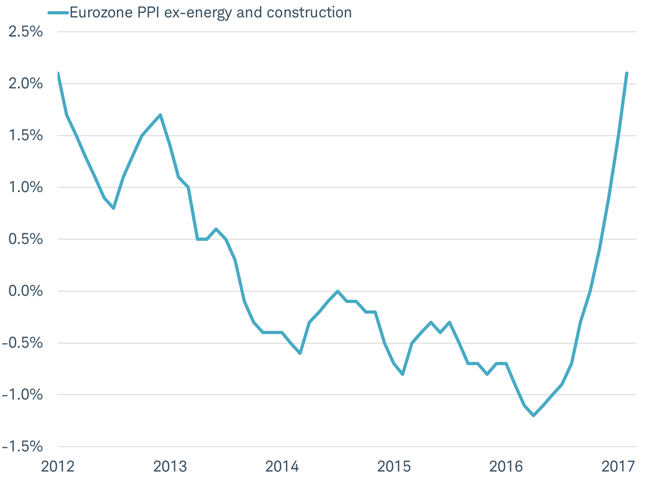

Revenue is on the rise, but so are input costs—which can act as a negative on profit growth. For example, in the Eurozone, the producer price index has risen to the highest level in five years (excluding volatile categories like energy and construction), as you can see in the chart below.

Input prices are also on the rise

Source: Charles Schwab, Bloomberg data as of 4/12/2017.

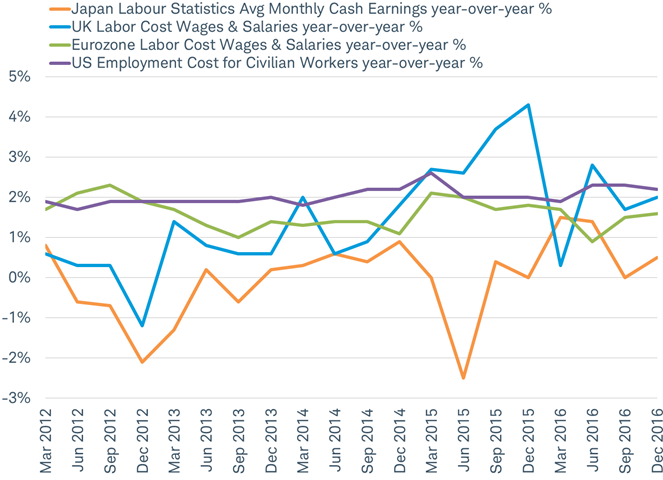

Although input costs may be up, the big cost for most businesses is labor. So far, labor costs have been stable and are not showing the rising momentum seen in non-labor input costs, as you can see in the chart below.

Labor costs remain well contained in 0-2% range

Source: Charles Schwab, Bloomberg data as of 4/12/2017.

Overall, the picture for profits is the brightest in years, but so are investor and analyst expectations. Indications that global revenue growth is not accelerating as expected, or that costs are picking up more quickly, could stall the steady rise in analysts’ earnings outlook for the coming year, removing the primary driver of the rise in global stocks over the past year.

So what?

U.S. stocks have had a modest pullback as investors appear to be reassessing potential global geopolitical risks and the reflation story. Volatility is finally picking up and further pullbacks are possible; but solid economic growth and a strong global earnings picture should allow the bull market to continue.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Diversification and rebalancing a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The Chicago Board of Exchange (CBOE) Volatility Index (VIX) is an index which provides a general indication on the expected level of implied volatility in the US market over the next 30 days.

The Consumer Confidence Index is a survey by the Conference Board that measures how optimistic or pessimistic consumers are with respect to the economy in the near future.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Institute for Supply Management (ISM) Non-manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms by the Institute of Supply Management. The ISM Non-manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

MSCI AC World Index (All Country World Index) is market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world. The MSCI ACWI is maintained by Morgan Stanley Capital International, and is comprised of stocks from both developed and emerging markets.

The Organization for Economic Cooperation and Development (OECD) Composite Leading Indicator is a monthly indicator used to evaluate near-term economic prospects and risks and is designed to capture turning points in an economy's growth cycle at an early stage.

The Eurozone Producer Price Index (PPI) is an index that measures the average change in selling prices received by Eurozone producers of goods and services.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© Charles Schwab

Read more commentaries by Charles Schwab