Populism is here—and it isn’t going away. The ideology can come from either side of the political spectrum, and it can have a big impact on policy, the macroeconomic landscape and—ultimately—how we invest today.

The drivers of populism’s rise in the West today include economic insecurity, social insecurity and political ineffectiveness. Based on previous populist episodes (particularly in Latin America) and current populist agendas, we expect policy changes to focus on three broad categories (Display):

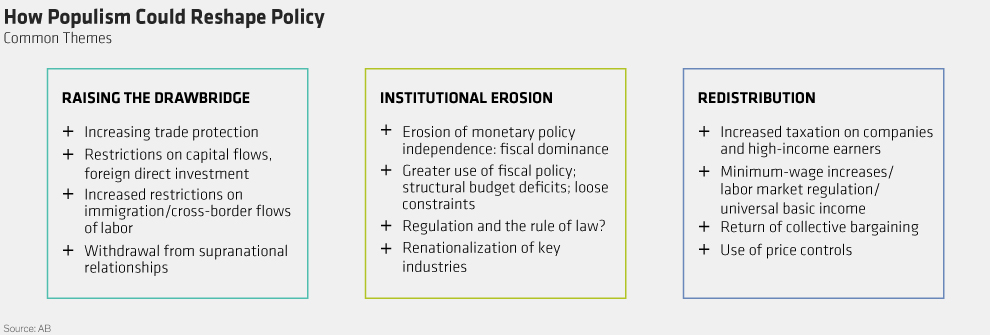

Raising the Drawbridge: These policies, which were prominent in US President Donald Trump’s campaign rhetoric, focus on several areas. They include more trade protection and restrictions on immigration and cross-border labor flows, together with withdrawal from supranational relationships. Immigration has been a key theme in recent European elections, and Brexit is perhaps the most dramatic example of a country choosing to withdraw from a supranational relationship.

Institutional Erosion: Attacks on the media, which have escalated in the US since Donald Trump entered office, are one example of the erosion of institutions globally. There have also been government attacks on the media, institutions of state, bureaucracy, the judiciary, parliamentary arrangements and other institutions. Turkey’s referendum in April, for example, gave President Recep Tayyip Erdogan powers widely regarded as autocratic. From a macroeconomic perspective, a key risk is the potential to undermine central bank independence through money-financed fiscal stimulus.

Redistribution Policies: These policies involve redirecting government largesse from the “rich” or “elites” toward the poor. The specific actions could include higher taxes on corporations and high-income earners and big wage increases. Redistribution is the least evident of the three policy areas in developed countries right now—in fact, the US under President Trump is actually moving to cut corporate taxes. But it did form a core part of the program that helped the opposition Labour Party come within a whisker of winning the recent parliamentary election in the UK.

FOUR STEPS TO FAILURE

The order and extent of the shift toward these types of policies is very important in determining the macroeconomic impact. In the typical Latin American experience—there are very many, including a large number of the biggest disasters in the history of populism—the playbook generally runs like this:

- Redistribution first. This is initially successful—in effect, a big fiscal stimulus. But, eventually, resource constraints begin to bite.

- As a result, the central bank is drawn into redistribution by, for example, printing money so fiscal largesse can continue. Eventually, inflation starts to rise and external accounts go into deficit.

- To deal with inflation and external deficits, the government enacts price controls and raises the drawbridge by putting restrictions on imports, the flow of foreign currency and other economic mechanisms.

- Ultimately, this populist playbook results in economic and political crisis and eventual regime change.

So far, what we’re seeing today is the raising of the drawbridge, but our research is focusing increasingly on the factors that would trigger the other two policy categories.

HOW COULD POPULISM IMPACT MARKETS?

The key point about all these policies is that they tend to be inflationary. But they also suggest that domestic factors will become more important, that bond yields and risk premiums will rise, and that dispersion within and between markets will increase. Ultimately, populism is likely to push policy in a less business-friendly direction, reversing the trend of the past four decades.

But over what time frame, and how strongly, should we expect these forces to play out? Barring a global shock, we would expect them to play out gradually, perhaps over a three-to-five-year time frame. But if the global economy hits the rocks in the next year or so, these risks could crystallize much more quickly and probably much more forcefully.

Clearly, populism and the world economy—and the interplay between them—are factors that global investors need to monitor very closely.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© 2017 AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein