Disruptive forces are wreaking havoc across the global business world. But not all disruption is fatal. Lots of companies are facing the threat—and thriving. We think they deserve more credit than investors are giving them.

Disruptive innovation is a red-hot investment theme today, and investors can’t seem to get enough of the technology goliaths leading the onslaught. The so-called FAANG stocks—Facebook, Apple, Amazon, Netflix and Google-parent Alphabet—have strongly outperformed the market this year, notwithstanding the recent sell-off.

These juggernauts of disruption continue to demonstrate that their spectacular growth may be sustainable. Yet we also think the market is underrating the ability of other companies to adapt to unfolding changes. Plenty of them are proving more disruption-resilient than generally acknowledged.

Here are three common beliefs about disruption and examples of companies that are defying them. We view these overlooked pockets of resilience as fertile investment hunting grounds.

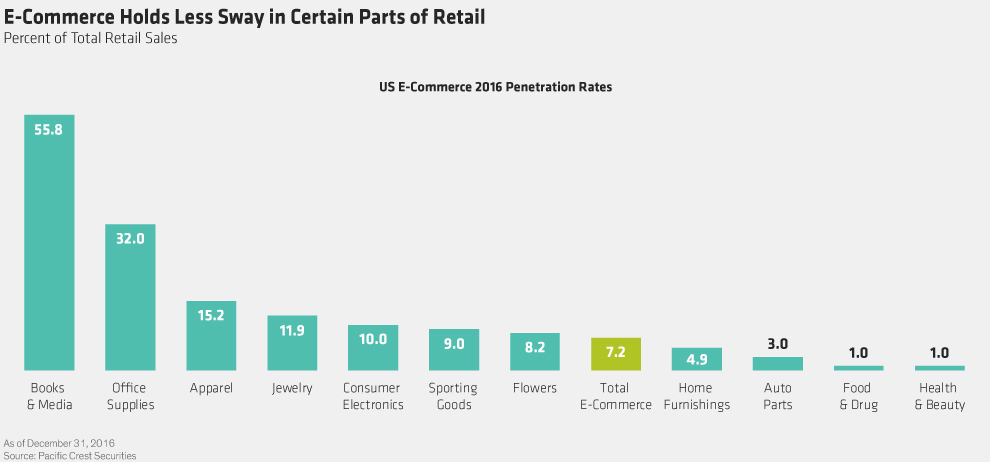

#1: AMAZON WILL RULE ALL RETAIL

Amazon has built a near-indomitable shopping machine, with its recent $13.7 billion takeover bid for Whole Foods marking its latest foray. It’s not hard to imagine this e-commerce behemoth taking over all retail itself.

But, while in-store traffic is declining, there are certain items consumers still prefer to buy in a physical store (Display). Off-price apparel and home-goods chains, auto-parts retailers, and sellers of items such as men’s suits and luxury goods are holding up well amid the retail gloom. They’ve crafted business strategies focused on personalized services and encouraging customer loyalty and frequent store visits.

Examples include off-price apparel retailers, which lure shoppers to their doors by offering ever-changing, limited-lot designer-brand assortments and a treasure hunt appeal. Auto-parts stores benefit from an aging car fleet and do-it-yourselfers who don’t have time to spare when making repairs and want to talk to someone knowledgeable if they have questions.

Another takeaway: consumers are buying experiences over stuff. That insight inspired makeovers at some restaurant chains and the major US movie-theater chains, which have buoyed attendance and profits with upgrades such as cushy recliner seating; premium concession items, including alcohol; and alternative content, such as live events and classic films on slow nights.

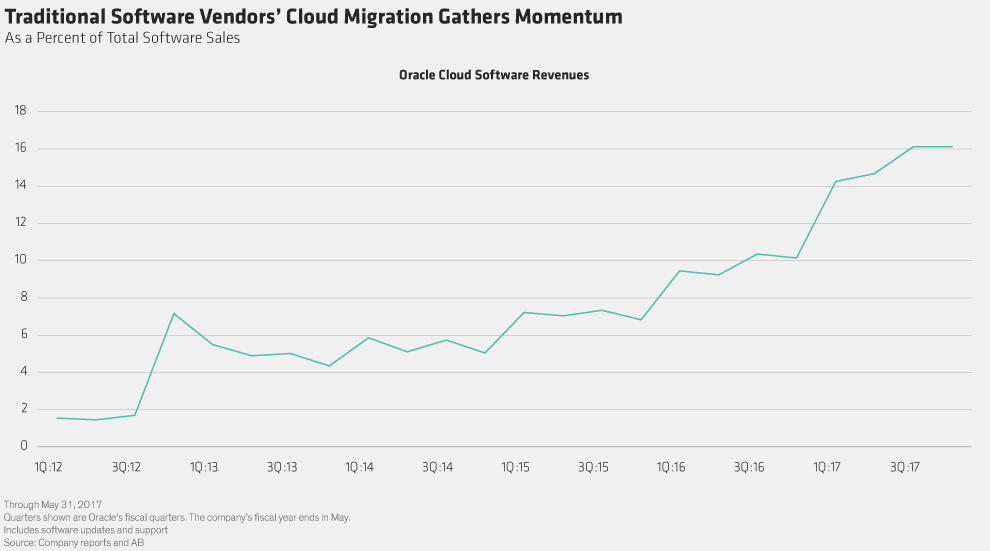

#2. EVERYTHING IS MOVING TO THE CLOUD

Companies are adopting cloud services at a remarkable pace. Gartner predicts that, by 2020, businesses without a cloud-based IT strategy will be as rare as one without Internet services today.

It’s been a rough transition for the traditional software vendors. While building their own cloud platforms, they still had to support their enormous yet dwindling on-premises businesses. The gradual shift from wholly license-based pricing models—where customers pay large upfront fees for software they can use indefinitely—to an increasing mix of subscription-based, cloud-delivered models initially hurt revenues (Display) and strained margins.

But the tides have turned. Though they’ve taken very different paths, legacy players such as Microsoft, Oracle and SAP have successfully weathered their cloud migrations, leveraging their huge installed bases and long-standing customer connections, which have proved extremely tough to sever, especially for mission-critical applications. In other words, their already sticky businesses have become even stickier.

#3: WEAK FINANCIALS-SECTOR PROFITS ARE FOREVER

Many financial services groups are struggling to cope with stubbornly low interest rates and the growing disintermediation trend. Investors wonder if weak financial-services profitability is here to stay. But this generalization misses the opportunities in the exceptions. For example, banks in countries with highly concentrated, conservatively run financial systems, such as Australia, Singapore, Canada and the Nordic countries, look headed for healthier loan growth and margin improvement as global growth revives. Future earnings don’t rely on higher global rates or looser regulation, though that would help.

Insurance brokers’ role as intermediaries has improved, thanks to the industry’s consolidation and investments in analytics, which have increased survivors’ clout as information-service providers. Other asset-light businesses, such as credit card payment and consumer credit reporting, are unaffected by regulation, and their wealth of consumer data makes them difficult to displace.

THE KEY TO WEALTH CREATION

Many of the companies in these pockets of resilience enjoy durably profitable business models and strong balance sheets, which give them greater control of their destinies. And, because their perseverance is underappreciated, their stocks tend to be reasonably valued—an important factor at a time when quality and stability are relatively expensive.

But finding fundamental resilience without overpaying isn’t easy. It requires skill, research and a broad, flexible view of risk and return, one that can pivot as market conditions do. This combination of quality, stability and reasonable valuation fits nicely with our investment approach, which emphasizes downside protection as the core of long-term wealth creation.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© 2017 AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein