Key Points

- Geopolitical, U.S. political and "bubble" concerns rose recently, putting a dent in the market's recent run. U.S. political turmoil is likely to keep market volatility elevated in the near term, but we believe the bull market still has legs.

- U.S. economic growth continues to be fairly healthy, and earnings season was positive for both bottom- and top-line growth; lending support to the bulls. But the storm in Washington is picking up velocity, especially as the upcoming debt ceiling fight looms large.

- Asia has been the center of recent geopolitical unrest but stocks in the region have largely followed corporate fundamentals.

Correcting conditions?

A couple of weeks ago we wrote in this space how the odds of a melt-up were increasing, as nothing seemed to dent the upward trend in stocks. What a difference a couple of weeks can make. The wall of worry that we were concerned was eroding has been at least partially built back up, and the uptrend took a hit. As a result sentiment conditions have corrected from overly optimistic levels based on most of the traditional metrics. In addition, the volatility index (VIX) spiked, rapidly pulled back, and spiked again—reminding investors that conditions can change quickly.

Volatility makes a comeback

Source: FactSet, Chicago Board Options Exchange. As of Aug. 14, 2017.

The first brick in the rebuilt wall was an increase in the warnings of "bubbles" forming. From former Federal Reserve Chairman Greenspan telling CNBC that a bond bubble was brewing, to warnings from various other pundits that housing, tech stocks, and/or the overall stock market were in bubbles—the warnings increased over the past couple of weeks. Perhaps the warnings themselves helped alleviate overly-optimistic sentiment. We are again reminded of one of our favorite quotes from one of the titans of finance, Sir John Templeton, who opined, "Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria." We have argued for some time that this bull market has been one of the least respected in history, with skepticism remaining high among investors—helping the bull market to persist. But we are mindful of the growing risks and believe the market could struggle in the near-term. Even before the latest selloff, market breadth had been deteriorating and we are in the midst of a period of typical-seasonal weakness. For now though, we believe any corrective phase is in the context of an ongoing secular bull market. The first significant reversal occurred when rhetoric surrounding North Korea ramped up with nuclear threats from Kim Jong Un and President Trump's "fire and fury" volley back. As of now it looks like North Korea has backed down and investors have breathed a sigh of relief; but attention is now on the drama in the Trump administration and growing concerns about getting pro-growth policies passed, which has contributed to another sizable pullback in the market.

No bear in sight

Ultimately, we think traditional fundamentals will define market behavior. After a weak first quarter, U.S. economic growth has rebounded, with an improving employment picture, tightening labor market, rising median wage growth, and a relatively healthy consumer. Even though past performance is no indication of future results, a prolonged bear market has never occurred outside the context of a recessionary environment. Looking at the Index of Leading Economic Indicators (LEI) from the Conference Board, there are no signs of a coming recession.

Source: FactSet, U.S. Conference Board. As of Aug. 14, 2017.

Additionally, the U.S. economy is getting some support from the rest of the world—with the leading economic indicator for the Organization for Economic Cooperation and Development (OECD) having turned up from its 2016 low.

Global growth may finally be helping

Source: FactSet, OECD. As of Aug. 14, 2017.

Also, now that earnings reporting season is largely complete, the corporate picture also looks quite healthy. Although we've seen modest pullbacks in some corporate surveys such as the Institute for Supply Management (ISM) Manufacturing and Non-Manufacturing Indexes, the National Federation of Independent Business (NFIB) optimism index—which measure the sentiment of the important small business sector—actually rose in the most recent reading.

Small business optimism remains high

Source: FactSet, Natl. Federation of Independent Business. As of Aug. 14, 2017.

As mentioned, the labor market continues to improve and tighten, with the unemployment rate down to 4.3%, forward-looking jobless claims remaining near historic lows, and the Job Openings and Labor Turnover Survey (JOLTS) showing a record number (6.2 million) of job openings.

Businesses are looking to hire

Source: FactSet, U.S. Dept. of Labor. As of Aug. 14, 2017.

The healthy job market may finally be translating to increased spending as retail sales, according to the Census Bureau, rose a better-than-expected 0.6% in July, while June was revised higher.

Washington could throw a wrench in things

After a week of extraordinary tension and turmoil following the horrific events in Charlottesville, questions abound about the upcoming debt ceiling fight specifically; and the Trump administration's agenda specifically. Trump's business-oriented councils have disbanded, healthcare reform is already off the table for now and tax reform looks less likely until the debt ceiling is raised and a budget is agreed to. Markets have begun to take it on the chin as what were already likely to be contentious negotiations are likely to become even testier given the drama in DC.

On the QT

Separately, the Federal Reserve is likely to embark on its quantitative tightening (QT) plan, in order to slowly unwind its bloated balance sheet. We have confidence that the Fed has little desire to jolt the financial markets, but it and the market are in uncharted territory as unwinding a $4.5 trillion balance has never been done historically. We continue to believe this will be an additional volatility-driver.

Asia outlook

As noted above, much of the geopolitical focus over the past couple of weeks has been on Asia as it has become the key region of conflict. Investors are used to looking to the Middle East for geopolitical risks that impact the markets, but recent developments have been focused in Asia, and these include:

- North Korea: Tensions between the United States and North Korea have escalated in recent months, but appear to have stalled with North Korea seeming to back off a threatened missile test toward Guam.

- India: Indian soldiers have been sent to a disputed Himalayan border with China in response to China’s road-construction, resulting in thousands of soldiers on each side of a military stand-off.

- South China Sea: China continues to assert its dominance over an area of the South China Sea also claimed by four of its neighbors and vital to global trade.

Yet, stocks in Asia are tracking corporate fundamentals, not geopolitical developments, even with North Korea dominating headlines.

For example, stocks in South Korea are tracking the earnings outlook, as you can see in the chart below. The South Korean stock market index (KOSPI) is up 23% so far this year through August 17, tracking the 21% rise in analysts' consensus estimates for earnings in the coming year for the stocks in the index (both measured in U.S. dollars).

Korea stocks have been tracking the trend in earnings rather than geopolitical developments

Source: Charles Schwab, Factset data as of 8/15/2017. Past performance is no guarantee of future results.

- Some global stock market volatility stemming from the news flow is to be expected, but we believe Asian stocks are likely to track the trend in economic and earnings growth in the second half of the year. After better-than-expected growth in the first half of the year, growth in Asia is likely to be solid in the second half of the year among the three biggest economies in Asia: China, Japan, and South Korea. China's economy saw an upside surprise to growth in the first half of 2017, but the data for the first month of the second half demonstrated that China's growth momentum may be softening slightly. The major data points released by the Chinese Government were lower in July than in June; dragged down by slower industrial output, cooler retail and housing sales, and construction activity. Yet the growth picture remains solid, supported by strong export growth, strong consumer demand, and policy support to lending through the leadership transition this fall. China's growth has a large impact on economic and earnings growth in the region.

- Japan's growth was outstanding in the first half of the year, capped with a 4% gross domestic product (GDP) growth rate reported by the Japanese government in the second quarter. Caveat: This pace of growth is unsustainable for Japan. The manufacturing purchasing managers' index (PMI) has slipped for the second month in a row and the stronger yen may have led to a slower pace of new export orders. Yet consumer spending may support solid, if not spectacular, growth. Japan's stock market tends to track the financial sector which has been one of the top three performing sectors of the world stock market (MSCI AC World Index) over the past three months, helping to sustain the Japanese stock market’s total return of 13% through August 15.

- In South Korea, consumer sentiment has held on to this year's strong gain to a six-year high, while growth in semiconductor exports—a key industry—has climbed to a 50% year-over-year pace according to South Korea’s trade ministry. The tech-focused economy—with nearly 50% of its stock market capitalization in the information technology sector—that has helped to produce strong stock market gains in the first half of the year. While we expect steady growth in coming quarters, economic policy initiatives of the new administration may shape the growth outlook.

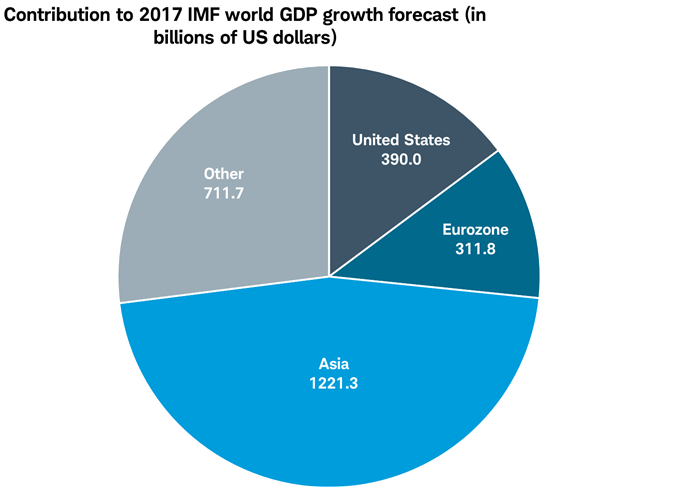

Asian economies currently contribute nearly half of global GDP growth, and almost double that of the United States and Eurozone combined, as you can see in the chart below.

Asia to contribute nearly half of global growth in 2017

Source: Charles Schwab, International Monetary Fund data as of 8/15/2017.

The potential for geopolitical military conflict has often been centered in less-economically impactful parts of the world, such as the Middle East; with the economic impact usually transmitted through changes in oil prices. That makes the potential for conflict in Asia different given its sizeable economic impact. While geopolitical risk of economic disruption is elevated, it is not high; leaving stocks to likely continue to track the solid growth in the region this year.

So what?

The latest bout of volatility illustrates why investors should stay focused on the longer-term. Risks for a more substantial pullback in the near-term still exist, as valuations remain elevated; but we believe solid U.S. and global economic growth, strong earnings, low inflation and still-ample global liquidity should allow the bull market to continue.

© Charles Schwab

www.schwab.com

© Charles Schwab

Read more commentaries by Charles Schwab