Incredible, Amazing…Unstop-a-bull?

Key Points

-

The bull market continues to be undisturbed by myriad actual or potential negative events and momentum favors the bulls for the foreseeable future. However, elevated valuations and growing investor complacency pose risks that could lead to a long-awaited pullback and/or a pickup in volatility from today’s extremely low base.

-

Third quarter earnings season is largely complete and can be characterized as a positive one—with strong “beat rates” for both top- and bottom-line results; while economic data continues to indicate solid growth. The new Federal Reserve chair nominee, Jerome Powell, is seen as quite acceptable to the market, while the House tax reform bill did little to move stocks.

-

The biggest shopping day of the year may not be what you think, and President Trump continues to talk trade.

Due to the Thanksgiving holiday, the next version of the Schwab Market Perspective will be published on December 8, 2017.

Unstop-a-bull?

The long-running bull market continues and has shown few signs of faltering. Even modest pullbacks have failed to gain any momentum and the uptrend has been largely intact throughout the course of 2017. There are signs that the potential for a “melt up” is heightened. Investor sentiment is well into the extreme optimism zone based on the Ned Davis Research Crowd Sentiment Index. Strategas Research reports that the S&P 500 has posted a 15% year-to-date gain through October, 17 times since 1950, including this year. While past performance is no indication of future results, the average return in those years for November and December was 2.7% and 4.9% respectively, above the historical average for those months of 1.5% and 3.2%. Additional support for the ongoing bull market could come from the holiday shopping season, which is shaping up to be a good one. For starters, there are 32 days between Thanksgiving and Christmas—the second most possible—and consumer confidence is quite high heading into the most important period of consumerism each year.

The ongoing bull market...

Source: FactSet, Standard & Poor's. As of Nov. 6, 2017. Past performance is no guarantee of future results.

...could be supported by a confident consumer heading into the holidays

Source: FactSet, Conference Board. As of Nov. 6, 2017.

We don’t want investors to be complacent however, as pullbacks are always possible and exogenous events are inherently unpredictable. Stretched valuations, combined with signs that investors may be complacent and/or overly optimistic, mean that the risk of pullback is elevated.

Economy and earning support ongoing bull

That solid backdrop has been bolstered by third quarter earnings season. According to FactSet, with 81% of the S&P 500 having reported, 74% have beaten earnings estimates, while 66% have beaten revenue estimates—both above their longer-term averages. However, the earnings season has also contributed to our belief that we are entering the latter innings of this bull market, as those companies that have even modestly disappointed have largely seen their stock prices face harsher declines than usual. EvercoreISI reports that S&P 500 companies that have missed estimates on both the revenue and earnings sides have seen their shares underperform over the ensuing three days by 3.47%, over 75 basis points more underperformance than the historical average.

Solid earnings are made possible by a strong economy, which appears to be more and more the case in the United States. Although some data continues to be skewed by the natural disasters, especially in the housing and auto areas, the majority of releases continue to point to solid growth. Personal spending rose a healthy 1.0% in September according to the Commerce Department, which was the largest increase since 2009; while the Chicago PMI supported other regional manufacturing surveys by rising to 66.2, its best level since March 2011. These solid regional surveys help feed into the Institute of Supply Management (ISM) survey that showed the manufacturing index remains in strong growth territory at 58.7, while the forward-looking new orders component posted a robust 63.4 reading. The significantly larger services side of the economy also looks healthy, with the Non-Manufacturing ISM rising to a boom level of 60.1, while the orders component remained strong at 62.8.

Manufacturing and services both looking strong

Source: FactSet, Institute for Supply Management. As of Nov. 6, 2017.

The labor market is becoming increasingly tight, which is filtering through to wage growth. Although average hourly earnings growth remains relatively tepid, the Atlanta Fed’s Wage Tracker—which measures median wage growth—shows significantly stronger growth of 3.6% on an annualized basis. In addition, the leading indicator of unemployment claims readings has recovered from its brief move higher during the hurricanes and is back at historical lows.

Claims are back at historical lows

Source: FactSet, U.S. Dept. of Labor. As of Nov. 6, 2017.

The latest employment report from the Department of Labor for October showed 261,000 jobs were added, rebounding from the hurricane-induced weakness seen in September; while the unemployment rate fell to the lowest level since 2000 at 4.1%.

New Fed head and major tax announcement fail to move markets

Two potentially historic announcements came recently, but failed to move markets to any great degree. President Trump nominated current Fed governor Jerome “Jay” Powell to replace Janet Yellen as Chairman of the Federal Reserve when her term ends early next year. The move was largely expected and greeted relatively favorably by the market as he is, like Yellen, a relatively dovish consensus builder; and therefore will represent continuity as the Fed continues its monetary policy normalization process. Given the aforementioned strong economic data and the pickup in some measures of wage growth, we believe the Fed will hike rates for the third time this year next month.

Great mall of China

Part of Washington went east and President Trump’s trip to Asia included a stop in China. While the recent buildup of U.S. military resources in Asia ahead of his visit may seem to suggest North Korea is the main focus; the topic of trade has gathered a lot of attention. The United States has a large trade deficit with China, but it hasn’t widened in the past three years, according to data from the U.S. Commerce department. In fact, China’s imports from the United States are up 14% over the past 12 months, compared with the 8% rise in U.S. imports from China. More broadly, China is importing more from the rest of the world. China’s merchandise trade surplus with the rest of the world peaked in 2015 and has been cut in half since then. The Chinese consumer is becoming more important to global companies. This year, Chinese consumers have become more confident, as you can see in the chart below.

Consumer confidence in China soared in 2017

Source: Charles Schwab, Bloomberg data as of 11/7/2017.

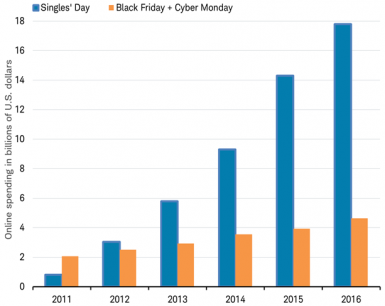

November 11 marks the biggest shopping holiday in the world—no, it isn’t Black Friday already—it’s “Singles' Day.” It started as an alternative to Valentine’s Day in China, where there are 30 million more men than women, and it is held every year on 11-11. It’s China's version of Black Friday, but several times larger. This year, China’s online sales may again rival all U.S. online and in-store sales on Black Friday, with this year’s Singles’ Day sales to be reported by Alibaba likely to be above $20 billion. Last year, the Chinese spent $17.8 billion on Singles’ Day, nearly four times what Americans spent online on Black Friday and Cyber Monday combined.

The biggest shopping holiday in the world is getting bigger

Source: Charles Schwab, Alibaba, comScore. Data as of 11/8/2017.

Many of the world’s biggest retailers participate in Singles' Day, but their online deals are focused on Chinese shoppers. Asia is rapidly becoming the focal point for global consumer spending with middle class spending in China to rival that of the U.S. middle class by 2020 according to World Bank estimates. A few examples of global companies citing Singles’ Day in their fourth quarter earnings reports from last year highlight the increasing importance of this holiday:

- Apple, Inc. - “On Singles’ Day, which is a huge day in China, as you know, we were the most popular U.S. brand on Alibaba.”

- Nike, Inc. - “We had our biggest Singles’ Day ever, reaching nearly three times last year's sales.”

- Lululemon Athletica, Inc. - “… our presence on Tmall [an Alibaba shopping website] has shown tremendous growth, led by our performance on Singles' Day last quarter.”

- The Hershey Co. - “We estimate that our e-commerce business has about a 10% share of the market in China and look to build on that over the remainder of the year, driven by Singles’ Day in November.”

- Kimberly Clark - “… we have lots of innovation coming out of Huggies, including a new super premium diaper pant that we recently launched on Singles' Day in November.”

*Any mention of individual companies is for illustrative purposes only and should not be viewed as any sort of investment recommendation.

President Trump’s meetings in Asia appear to be focusing on narrowing the U.S.-China trade gap by growing China’s imports from the United States rather than restricting Chinese–made products in U.S. markets (outside of a few products such as steel). The growth of Singles’ Day is a reminder that global trade is important to corporate earnings growth. Fortunately, despite heightened fears of protectionism at the start of 2017, global trade this year has been growing at the fastest pace in six years.

So what?

Earnings season, both in the United States and globally, has been solid, while economic growth has accelerated across much of the globe—all supportive of an ongoing global bull market. Elevated optimism and complacency could lead to pullbacks, but we believe it would be in the context of an ongoing bull market.

© Charles Schwab