Stock market gains have accelerated and it has the markings of a melt-up or “blow-off” phase. At this point, the surge has been accompanied by a commensurate improvement to corporate earnings, but risks are also likely rising.

The U.S. economy has stepped up its pace of growth, but the rate of improvement appears to be moderating, which could lead to more lackluster and/or volatile stock market performance in the coming months.

European growth is booming relative to recent history, but there are some potential pitfalls to watch for in the coming months.

Melt-up!

U.S. stock market gains have accelerated in the first month of the year, leading to the appearance of a melt-up or blow-off phase of the bull market.

Looking suspiciously like a melt-up

Source: FactSet, Standard & Poor's. As of Jan. 19, 2018. Past performance is no indication of future results.

We’ve often warned that melt-ups can feel good at the time but typically end in melt-downs, even if only briefly. Melt-ups can last for a decent amount of time and investors who bail could miss out on potential gains. We are in the relatively early stages of this move, but a catalyst for a pullback could come at any time.

Anecdotally, the heightened scrutiny of the rally and skepticism around its sustainability suggests investor sentiment—although exuberant—is not irrational. That said, the Ned Davis Research Crowd Sentiment Poll has reached its highest-ever level of optimism since the index was created in 2002. But on the behavioral side, we still see money coming out of equity mutual funds and exchange-traded funds (ETFs), with Evercore ISI Research reporting that $44 billion was pulled out during the three weeks ending January 12.

As mentioned, earnings have been accelerating along with stock prices, keeping valuation expansion to a minimum. For example, the forward P/E (price-to-earnings) ratio for the S&P 500 is currently about 18.5 according to data from Thomson Reuters. Although elevated, it’s well below the 24-26 level at the 2000 peak. In the multi-year run-up to the 2000 peak, Federal Reserve Chairman Alan Greenspan made his famous reference to the possibility of “irrational exuberance”—but that was in 1996, and the bull market continued for more than three years. But with optimism elevated and valuations rich, the cushion in the market has been reduced—which could lead to more volatility and more sizable pullbacks this year than we saw last year. As you can see in the table below, years with exceptionally low volatility (as measured by maximum intra-year drawdown) tended to be followed by years with more volatility/drawdowns.

Source: Bloomberg, Strategas Research Partners LLC. For illustrative purposes only. Past performance is no indication of future results.

Economic growth takes a step forward

In addition to strong earnings, the uptick in U.S. economic growth supports a continuation of the bull market. In short, we don’t see any sign of a recession on the horizon, which has been typically what it takes to ignite a bear market. Case in point is the latest acceleration in the leading indicators—indicative of not only continued growth, but an accelerating rate of growth.

LEI doesn’t indicate trouble on the horizon

Source: FactSet, U.S. Conference Board. As of Jan. 19, 2018.

But not all is rosy. The Empire Manufacturing Index recently fell to a still-strong 17.7 from a robust 19.6, and the Philly Fed Index fell to an again solid 22.2 from 27.9. Also, the Citigroup Economic Surprise Index—which measures how economic is coming in relative to expectations—has rolled over, which was to be expected given it’s a mean-reverting index.

Surprise Index rolling over

Source: FactSet, Citigroup. As of Jan. 19, 2018.

The deterioration in this index in the first half of last year was not met with weak stock market performance, so fewer positive surprises isn’t necessarily the death knell for stocks. And with the impact of the Tax Cut and Jobs Act still coming into focus and the rebuilding from last year’s hurricanes still ongoing, the potential path to even better economic growth appears to be in place.

Potential Pitfalls

Some of the potential risks to the current rally may come from Washington. Although the market has largely ignored the “shutdown” drama, as has tended to be the case historically, investors should not become complacent about the risk of political dysfunction. In addition, trade protectionism—including possibly pulling out of NAFTA—and tariffs could be a meaningful risk for stocks, especially if they contribute to higher inflation. Finally, the approach to the midterm elections could add to the market’s volatility; but also could put limits on what can be done legislatively.

The Federal Reserve’s upcoming meeting has investors’ attention. The meeting next week—Chair Janet Yellen’s final meeting—is expected to yield no change to interest rates, but the statement will be closely watched for signs that inflation is becoming a bigger concern due to the tight labor market and tax-related fiscal stimulus. Higher inflation remains the most formidable risk in our view, as it would put added pressure on the Fed and downward pressure on stock market valuations.

Risks to the Euroboom

The United States isn’t the only place where there are potential stumbling blocks in the road. There are three near-term risks we believe are worth watching overseas; but they may not be enough to end the Euroboom: the upcoming Italian election, euro currency strength, and trade threats.

Italian election: Italian voters will head to the polls on March 4. A broad coalition of moderate, pro-European parties is the most likely outcome. However, there is a risk that increasing support for populist parties and ideas may force Italy to veer from a sustainable fiscal path, reigniting a problem for its own debt that could be felt across the Eurozone. Since mid-December, when the election date was announced:

The spread between Italian and German bonds has tightened (going from 1.55% to 1.50% currently).

Italy has been the best performing European stock market, returning close to 8%.

The euro currency has risen against the dollar.

Since markets are not pricing in much risk from the Italian election, they may be vulnerable to a surprise if populist parties perform better than expected. Polling will be closely watched by market participants in the coming weeks.

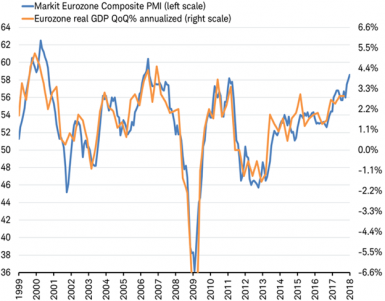

Euro currency strength: The euro relative to the U.S. dollar is up from about 1.07 a year ago to about 1.24; a rise of 16% with about half of that coming in just the past two months, as it surged to the highest level against the dollar in more than three years. The impact of a sharply rising currency may be starting to negatively impact growth in the Eurozone. The January Eurozone PMI data showed that manufacturing activity slowed in January, even as services picked up, suggesting that the euro’s gains may be weighing on exports. So far, the strength is coming along with booming growth. The Eurozone composite PMI points to gross domestic product (GDP) growth that may have exceeded an annualized 4% in the fourth quarter—the fastest growth seen in 20 years. We believe, this has allowed Eurozone stocks to post strong gains over the past year, despite the rise in the euro. Yet if more signs emerge that the stronger currency is weighing on growth the markets could reassess their outlook.

Euroboom: GDP growth may have exceed 4% in the fourth quarter

Source: Charles Schwab, Bloomberg data as of 1/24/2018.

Trade threats: Investors have been worried about a big move toward trade protectionism from the Trump administration from day one. After hinting at new trade moves for months, the Trump administration approved International Trade Commission recommendations that were made public a few months ago to impose tariffs for three to four years on imported solar cells and washing machines. The announcement comes just ahead of Trump’s trip to Davos and his State of the Union address. Markets have shrugged these moves off as more of what we saw last year—more bark than bite. So far, U.S. trade measures have been narrow with little negative impact on targeted sectors and have come with little to no economic risk in our view This is a far cry from President Trump’s 2016 election campaign threat to impose a 45% across-the-board tariff on Chinese goods.

However, there may be more announcements coming. President Trump has about 90 days to decide whether to impose tariffs on imported steel (as his predecessor did) and aluminum, while investigating China’s intellectual-property practices. Chinese officials have voiced disappointment in response to the tariffs, but their response was restrained rather than promising retaliation. In addition, another round of NAFTA negotiations took place this week with talks bogged down. We believe Mexico has the most to lose; yet Mexico’s stock market is up about 6% this year (measured in U.S. dollars), in line with the 6% gain in U.S. stocks through January 22. So far, there is no sign of a change in President Trump’s approach on U.S. trade that would be sharply negative for international markets—but we’ll keep watching, since a major shift in strategy could have a material impact on global markets and spark a long absent correction.

Meanwhile, trade news remains favorable for economic and earnings growth in Europe, the largest trading partner for most countries. In fact, the Trans Pacific Partnership (TPP)—viewed as dead a year ago after President Trump pulled the United States out of the agreement—has been agreed to by 11 other nations (creating a free trade zone with a combined GDP of $13.7 billion according to the Wall Street Journal) with a signing ceremony set for March.

So what?

U.S. stocks may have entered a melt-up phase but for now it is relatively well supported by earnings growth; and although sentiment is extended, behavioral measures indicate still some skepticism. However, given elevated valuations, and the aforementioned overly optimistic sentiment, volatility is likely to increase and more frequent pullbacks are possible. The bull should continue to run, but likely with a bit more drama, so it’s important to stay diversified and disciplined around your long-term asset allocation.