On May 14, new Municipal Securities Rulemaking Board (MSRB) regulations will require the disclosure of the often dramatic markups, or transaction costs, that retail investors are subject to when buying individual municipal bonds.

Specifically, the new regulations will require confirmation statements to show both the dollar and percentage amount of the markup (or markdown), the date and time of the trade, and a link to emma.msrb.org, where the public can get more investor-friendly information about muni bond prices, market trends and more. All of this is good.

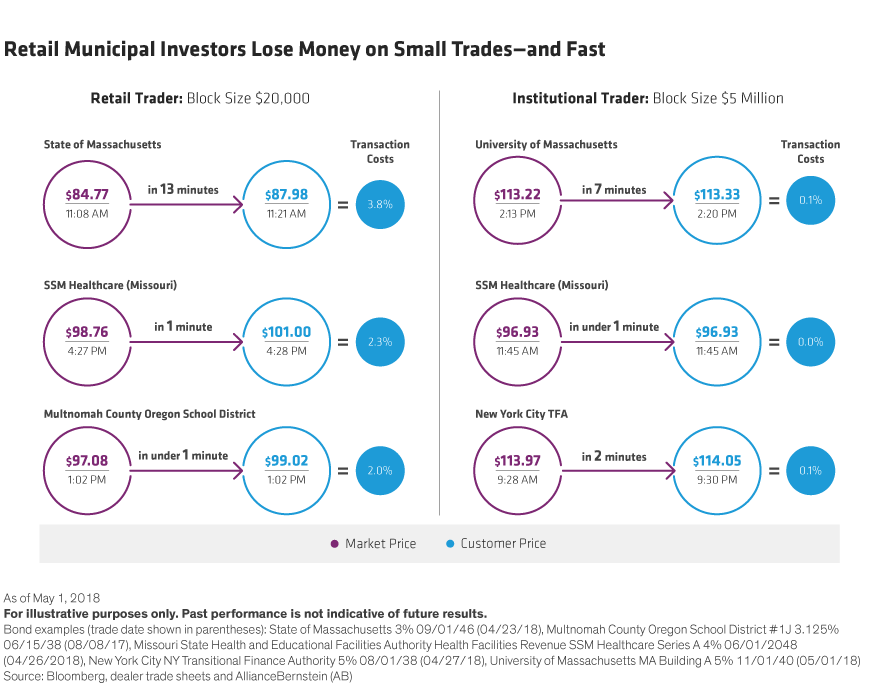

And yet, it’s likely to outrage many investors. Why? Because until now, many of them thought they’d been getting something for nothing, and as is clear from the above Display,that isn’t so.

Not All Prices Are Equal

It’s not uncommon for individual investors to think that their execution price—the “price paid” that they see on their pre-May 14 confirmation statement—is the price procured by all municipal bond investors at that time. Many believe that there is no fee or cost associated with their transaction. But that’s not the case.

The reason there’s a cost has to do with volume and convenience, and it’s a familiar story. The brand-name specialty dog or cat food on the shelves of your local boutique pet store is expensive. But the exact same brand of pet food is also available in a large bag from Amazon.com, where it costs a whole lot less—a function of both quantity and conveyance.

Similarly, there’s a significant markup on small trades made in the bond market compared with the large-block trades made by mutual funds, ETFs and separately managed accounts (SMAs). When a dealer sells a small block to a retail investor, it’s priced higher than a large block sold to an institutional investor such as an asset manager, because of the volume and inconvenience of trading to multiple partners.

What constitutes a large trade versus a small trade? Large blocks are measured in the millions of dollars, with $5 million blocks a frequently traded unit. Individual (retail) investors commonly trade in lots of $20,000 or $25,000. While that’s unquestionably a lot of money, even lots running up to $100,000 are not large enough to avoid big markup penalties.

According to S&P Global, retail markups averaged roughly 1.1% in 2016, and our own research turned up much larger markups in the first three recent examples we found on Bloomberg, which we used in our Display. Larger studies cited by the Securities and Exchange Commission have found that retail investors pay average transaction costs of 2%—and sometimes pay as much as 5%. And the overall impact is enormous: the Securities Litigation & Consulting Group estimates that between 2005 and 2013, markups and markdowns resulted in net costs of at least $20 billion to retail investors.

But sizable transaction costs aren’t the only problem. To add insult to injury, retail investors can also be shut out of the best pricing on new-issue deals. Our example of SSM Healthcare in the Display above shows an institutional investor (right)—likely an asset manager—receiving the initial offering price on the bond at 11:45 a.m., as soon as it hit the market.

Two hours later, at 1:45 p.m., the issue became free to trade in the secondary market, at which point individual investors began to trade as well, and the price on the security began to rise, because the bond was in high demand. Our retail investor (left) bought the bond shortly thereafter, not only at a significant markup of $2.24, or 2.3%, but also at a much higher overall price ($101.00) than our institutional investor paid ($96.93).

Not only does the damage hit the individual investor’s bottom line at the start, but the pain continues long after. Having paid more for the bonds at the outset, the investor has less money invested, less portfolio growth potential and less income earned.

Individual Investors Ponder How to Respond

Investors now face a choice. They may choose to continue with the status quo of buying bonds in small blocks. Or they may move into passive funds, active mutual funds or even active SMAs. Any of the latter three would give investors the advantage of pooling their assets with other investors’ monies and eliminating the huge transaction costs they’re currently subject to.

A recent Bloomberg article posits that the new regulations are likely to accelerate the existing trend in increased individual ownership of mutual funds and SMAs, both of which average lower fees than the transaction costs associated with individual bond purchases. And active management has many advantages over passive investing, as we’ve described previously. The decision as to which of the four paths to follow is, of course, up to the individual investor.

Unfortunately, loopholes will remain around the new transparency regulations, hampering many investors’ ability to decide. For example, markups will be disclosed only when the dealer has bought the security and sold it to the retail investor on the same day. That means that if the security was purchased by the dealer the previous afternoon and sold to the investor the next morning, the markup will not be revealed. Also, the size of the dealer’s block must be equal to or greater than what the dealer sells to the customer in order to prompt any disclosure.

So what exactly happens come May 14? Regulators will say to investors, Here are just someof the shocking facts—the decision is yours.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein