U.S. stocks have been trending higher, but endured some rough water over the past few weeks. Although bumpy, major U.S. indexes have moved to the top of the recent range and the secular bull market should stay intact.

The U.S. economy is in good shape and likely able to withstand some of the brewing storms. Bouts of volatility are unlikely to diminish Fed tightening expectations and a June hike remains a near certainty.

Trade concerns are ramping up; and although the major global players look able to withstand at least some trade stress, the margin for error is narrowing.

“He that will not sail ‘till all dangers are over must never put to sea.” - Dr. Thomas Fuller

Choppy waters

Investors in U.S. stocks may have felt like being on a boat where passengers are running to one side, then deciding all of a sudden to rush to the other side. It can be stomach churning, but risks are part of investing and bouts of volatility should persist. Joining the shifting crowd is not a successful way to invest; rather those that remain calm during the storms and keep their focus on the horizon have a much better chance of achieving their goals..

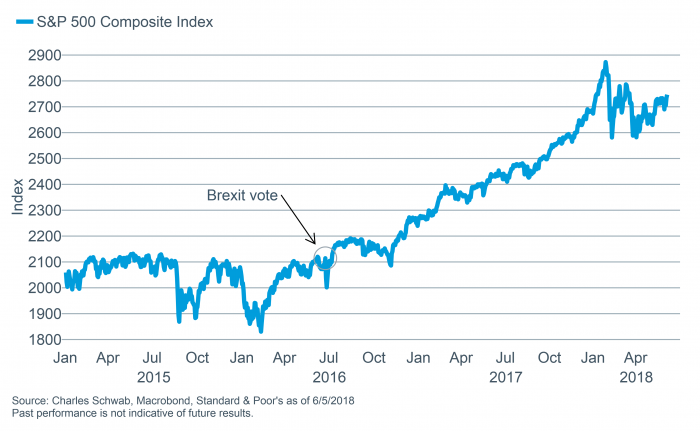

Déjà vu: a European country having political problems and fear rising that its membership in the Eurozone may be in doubt. This time it was Italy, with some sharp down moves on the initial political/election uncertainty—amid a spike in Italian yields. But a calming in those tensions helped U.S. stocks move to the top of their recent range. Continued turbulence is to be expected as the structural constraints in Europe remain but we don’t see long-lasting damage at this point. As a reminder, in another potential European “crisis”, the reaction to the Brexit vote in June 2016 was violent at the time, but looking back it was a minor squall in an ongoing bull market.

Brexit vote reaction looks minor in hindsight

More broadly, what we are likely experiencing are fissures associated with a receding tide of global liquidity, tighter financial conditions, a strengthening U.S. dollar, and of course trade tensions. On trade, the United States let the originally-announced steel and aluminum tariff exemptions expire, and there were retaliatory actions from several of our trading partners. This is another step closer to a more damaging trade war, with rhetoric having ramped up lately. On the dollar and tighter financial conditions/less global liquidity: an apt analogy is fishing with dynamite. We’ve begun to see emerge some “small fish” in the emerging market world have problems with the strengthening dollar (such as Turkey). The money that many emerging countries have borrowed in U.S. dollars becomes more expensive to service. For now the problems appear contained, but we are watching indicators for signs that bigger fish may float to the surface. As we have been cautioning, when the liquidity tide begins to recede, it’s time to start to look for who has been swimming naked.

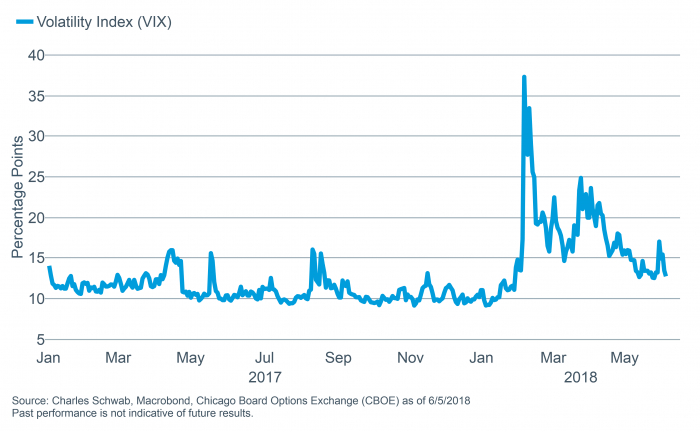

A sign of coming attractions? Volatility ticked higher recently

The U.S. ship remains solid

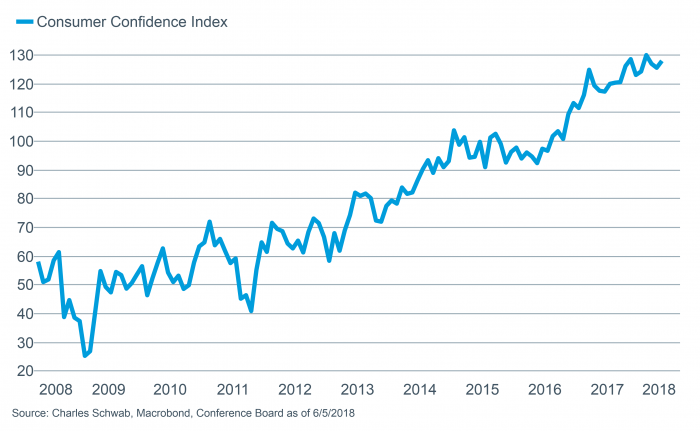

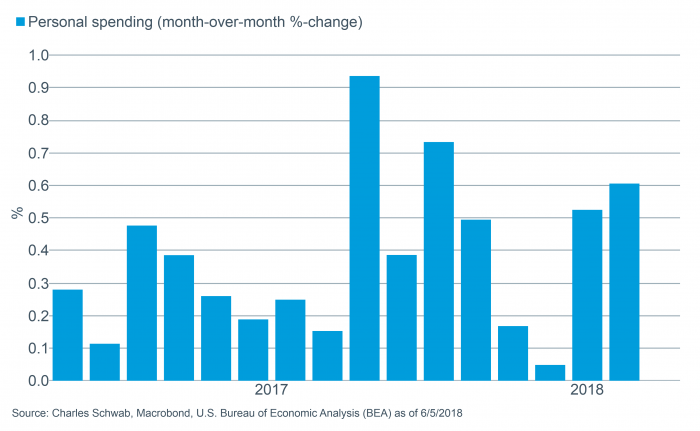

It’s nice to have a solid vessel with which to navigate rough waters, and it appears that the U.S. economy is just that. Consumers are gaining conviction in the economic expansion, with The Conference Board reporting a jump in consumer confidence; while the Bureau of Economic Analysis (BEA) reported that personal spending rose a better than expected 0.6%, continuing a rebound from softness seen earlier in the year.

Consumer confidence is high…

…helping spending to rebound

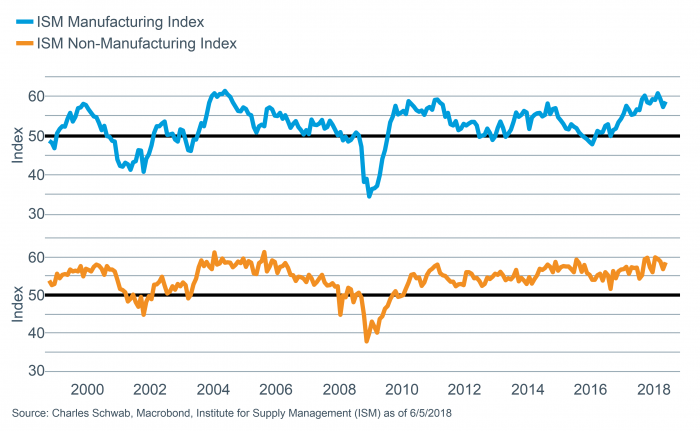

Businesses are equally confident, with regional manufacturing surveys continuing to surprise on the upside; backed up by the national Institute for Supply Management’s (ISM) manufacturing index rising to a solid 58.7, while the new order reading rose to 63.7. Meanwhile the larger service side of the ledger remains strong, with the ISM non-manufacturing index rising to 58.6, while the new order component ticked higher to a robust 60.5.

Business sentiment remains strong

And while the pricing components of these surveys have risen, the core personal consumption expenditure (PCE) measure of inflation—a favored measure of the Fed’s—is up only 1.8% versus the year ago period. Still-subdued inflation is somewhat remarkable given the tightness in labor market: payroll growth surprised on the upside with 223,000 jobs added in May, while the unemployment rate dipped to 3.8%—the lowest level since April 2000.

Fed expectations changing?

As a result of the continued solid U.S. economy and strong labor market, we believe the Federal Reserve will bump rates up again during its two-day meeting which concludes on June 13th. The tumult mentioned above, both internationally and domestically, resulted initially in the probabilities, as calculated by the fed fund futures market, of the pace of future hikes to be downgraded. But in the immediate aftermath of the strong May jobs report, those expectations bumped higher again. That said, some members of the Federal Open Market Committee (FOMC) have expressed some concern about the possibility of the yield curve inverting (when shorter-term rates become higher than longer-term rates), so there will likely remain heightened sensitivity to yield curve-related comments in the FOMC statement and subsequent press conference.

Will inversion concerns influence Fed actions?

With near-term inflation risk still fairly benign, and global geopolitical pressures rising, we’ll be watching to see if other FOMC members join Minneapolis Fed President Neel Kashkari in believing that rates may already be near the “neutral rate”—a perceived level which doesn’t add to or deter economic growth—and that numerous future hikes may not be needed.

Trade talk: G7 and recession

The leaders of the G7 member nations (United States, United Kingdom, Japan, Canada, Germany, France and Italy) gathered for their annual meeting today. It has been relatively rare in the past six years that all of these countries’ economies were growing at the same time. Economic recessions, defined as back-to-back quarters of shrinking GDP (although that is not the official definition for the United States), were experienced:

in Canada in 2015,

in both Japan and France in 2014,

Italy in 2013, and

in Germany in 2012.

A focus of the G7 meeting will be on the importance of trade in keeping their economies out of recession. Which begs the question: how vulnerable to recession are they right now, ahead of any potential major trade conflict? The unemployment data released in the past week may help answer that question.

Despite all the attention it gets each month, the unemployment rate as an economic indicator often gets a bad rap, as it seeks to tell us the percentage of people in the labor force looking for work. Three common criticisms leveled at the unemployment rate are:

Some find fault in how it measures labor market conditions by ignoring those people that are temporarily giving up on finding a job and dropping out of the labor force.

Others criticize the way it doesn’t measure the quality of the job—if someone just took a lower-skilled job than they had before because they couldn’t find anything else they still count as employed.

Still others cite the fact that no matter how it is measured unemployment has typically acted as a lagging, and not a leading, indicator of the economy. The unemployment rate typically begins falling after a recovery is well underway, and usually only starts to rise after a slowdown has already impacted sales for companies (and the slowdown has already shown up in other economic readings).

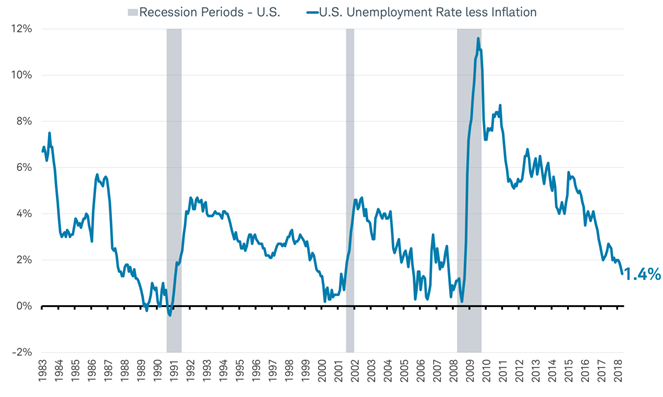

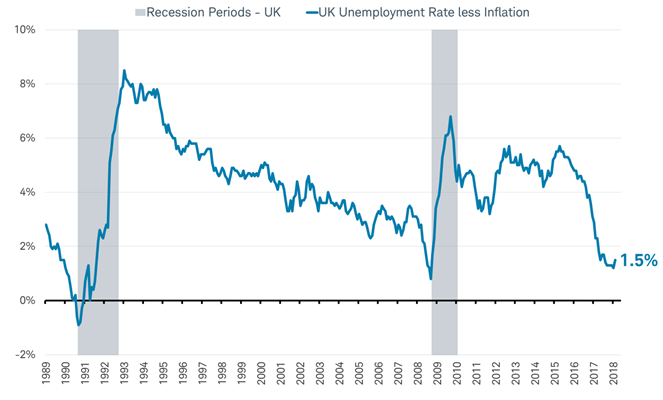

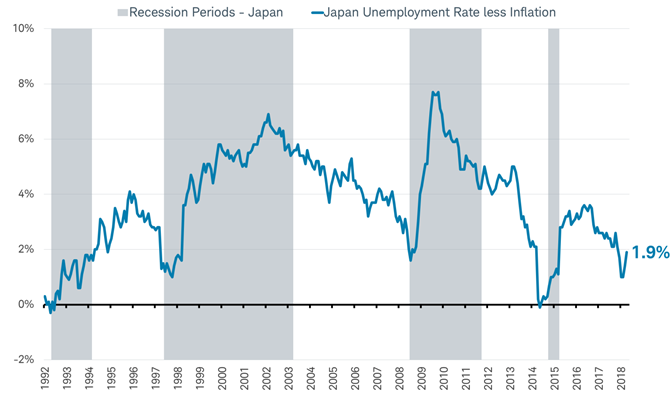

While all of these are valid criticisms, we don’t believe the attention the unemployment rate gets is misplaced. In fact, when combined with the rate of inflation, a country’s unemployment rate can give a signal that has been useful in signaling a peak in the economy that typically accompanies the start of a bear market for stocks. This is because of how these two indicators work together to describe the stage of the economic cycle. Early in the start of a new economic cycle the unemployment rate is high following the layoffs from the recession and the rate of inflation is usually low, reflecting the lack of demand for products and services relative to the capacity for supply. The gap between the unemployment rate and the rate of inflation is relatively wide. But as the economic cycle matures the unemployment rate falls with more people finding work and inflation rises as demand picks up and capacity becomes constrained. Late in the cycle, the gap between the unemployment rate and the inflation rate closes and in the past that has signaled an economy is near a peak.

The charts below show the gap between the unemployment rate and the inflation rate (CPI) closing as each economy nears or enters a recession (the grey shaded areas). Fortunately, each of them show that while the gap has been closing, it has not yet closed—signaling there may be more time left in the economic cycle before a recession in many major countries.

United States

Source: Charles Schwab, Factset data as of 6/5/2018.

United Kingdom

Source: Charles Schwab, Factset data as of 6/5/2018.

Japan

Source: Charles Schwab, Factset data as of 6/5/2018.

The other four G7 countries (Canada, Germany, Italy and France) also have not seen the gap in their unemployment and inflation rates close to the levels that have preceeded recessions in their countries during the past 30 years. Yet, the gap has been closing for many of the G7 nations, suggesting their economic cycles are maturing, which may increase their vulnerability to trade risks, making it an increasingly important topic of conversation for the nations’ leaders.

So what?

U.S. stocks have moved toward the top of the recent range but volatility is likely to rise at times during the summer as investors deal with various global geopolitical headwinds. Further strength in the U.S. dollar would likely exacerbate the volatility—particularly within emerging markets. But limited signs of pending recession risk—at least in the United States—should keep the path of least resistance for the stock market higher. That said, patience and discipline are more important than ever in the face of sometimes ominous-sounding headlines.