Many investors have started to scrutinize the shape of the US Treasury yield curve, worried that a potential yield-curve inversion would mean imminent recession. In our view, things aren’t that simple.

The yield curve has flattened considerably since the Federal Reserve began raising short-term interest rates. Long-term rates aren’t rising nearly as fast, leaving 10-year US Treasury yields only about 0.25% higher than two-year yields.

In past economic cycles, an inverted yield curve—with 10-year yields dropping below two-year yields—has preceded recessions. If the yield curve does invert in the near future, does it mean trouble is right ahead for the US economy, or could this time be different?

A Useful Signal—But Certainly Not a Perfect One

The logic behind the inverted yield curve as a recession indicator is simple: if long-term yields are lower than short-term yields, the market’s view is that growth will slow in the coming years. More often than not, that view has been right. An inverted curve has preceded every recession in the post-WWII era.

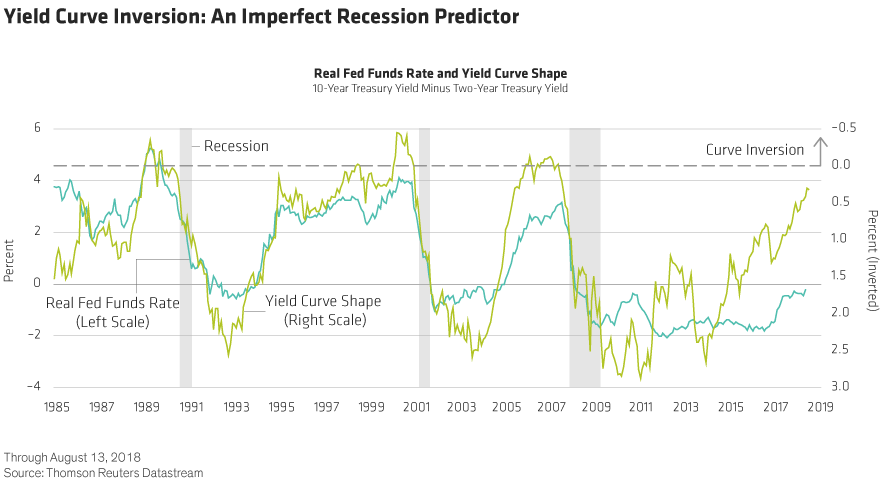

But the track record is by no means perfect (Display).

In some cases, the US yield curve inverted but wasn’t followed by a recession. In the late 1980s, for example, the yield curve inverted and then steepened again, before inverting again later on before recession. The curve also inverted very briefly in the late 1990s, too, and again in 2005–2006.

Even when a recession does happen, the amount of time before it starts has varied widely: sometimes it’s taken nearly two years and sometimes only a handful of months. So, even if investors believe that the shape of the yield curve is a powerful predictor of recessions, it’s not exactly a strong trading rule.

Distortions from Quantitative Easing

It’s also possible that the yield-curve signal may be somewhat distorted this time around.

Typically, a flattening curve indicates that monetary policy is too tight—short-term rates have risen too far for the economy to handle without going into recession. In this case, though, that argument is hard to make. Adjusted for inflation, the “real” short-term interest rate is still below 0%. It’s reasonable to think rates will peak at much lower levels this cycle than in the past, but it doesn’t seem likely that 0% is too high for the economy to handle.

So, if the yield curve isn’t signaling tight money, why is the curve flattening?

There are several possibilities, but we think the most likely one is that quantitative easing is distorting the long end of the yield curve. The Fed’s balance sheet may be shrinking, but it still dwarfs its size in past cycles. In fact, it’s larger by multiples.

Also, the European Central Bank and Bank of Japan are still buying their own long-term securities. This action is keeping longer-term yields much lower than they would otherwise be, driving investors who might otherwise buy those securities into the higher-yielding US Treasury market. These “artificial” purchasers are pushing US Treasury yields lower than they would be in a non-QE world.

Is the Short-Term Curve Shape a Better Gauge?

Recent Federal Reserve research has tried to adjust for this distortion by focusing on the shape of the yield curve at shorter maturities, which are more directly linked to monetary policy. This analysis has found that shorter-term rates predict recessions more effectively than longer-term rates do. And based on the Fed’s research, the shape of the yield curve at shorter maturities isn’t setting off alarm bells.

Let’s see if we can sum up what all of this means for the yield curve and what signal is being sent today.

The yield curve seems all but certain to invert again before the next US recession, so it’s a useful benchmark as the economic cycle progresses. But the signal is never perfect—and is likely to be even more imperfect this time around. There may also be a very long delay between the yield-curve inversion and the eventual start of the next US recession.

Based on this assessment, we don’t think it makes sense for investors to build their economic expectations based on the shape of the yield curve. And they certainly shouldn’t manage their portfolios under the assumption that a flattening or inverted yield curve means that a recession is imminent.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein