China is often seen as a source of low-cost manufacturing. Yet today, many Chinese companies are building world-class brands that are overtaking global competitors at home—and are not fully understood by investors.

Brands are the lifeblood of business resilience. Companies with dominant brands enjoy huge competitive advantages and pricing power. However, investors discovering China today often focus on short-term financial results and underestimate the intangible value of brands. This is a big oversight, as Chinese consumers increasingly shun Western brands in favor of homegrown alternatives.

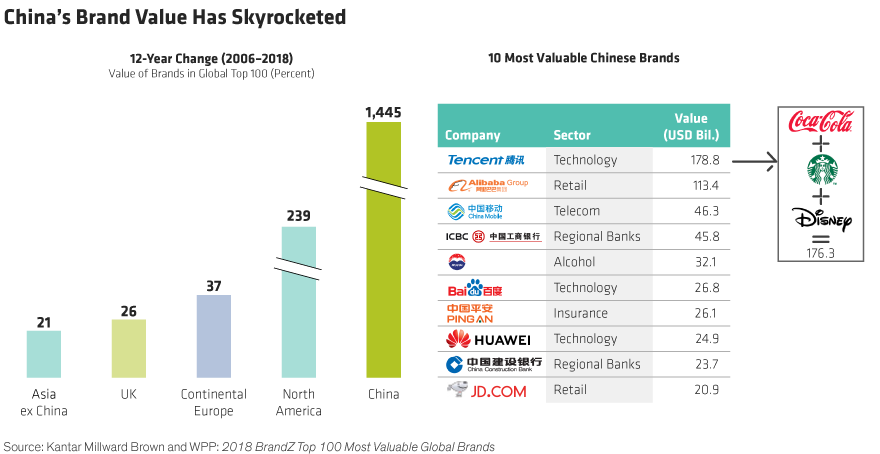

Chinese Brands Rise in Global Rankings

Investors don’t usually incorporate brand analysis into their financial forecasts. But in China, the rapid rise in the value of local brands is a key ingredient in the long-term growth potential of companies. In fact, 15 Chinese companies now rank among the top 100 global brands, according to a recent report by advertising group WPP. Two Chinese brands—Alibaba Group and Tencent—are in the top 10. And internet giant Tencent’s brand was valued at more than the combined brand value of Coca-Cola, Disney and Starbucks, three American brand icons.

The total value of Chinese brands in the top 100 has grown by 14 times since the first Chinese brand entered the list 12 years ago, outpacing developed-market brands by a wide margin (Display). And today, Chinese brands account for 14% of the value of the top 100 global brands.

Investors should care about these trends. Companies with strong brands have outperformed the S&P 500 and MSCI World indices by a large margin, according to WPP. And in our experience as growth investors in emerging markets, we believe finding companies that can protect their businesses with competitive moats is the key to success. Strong brands do exactly that.

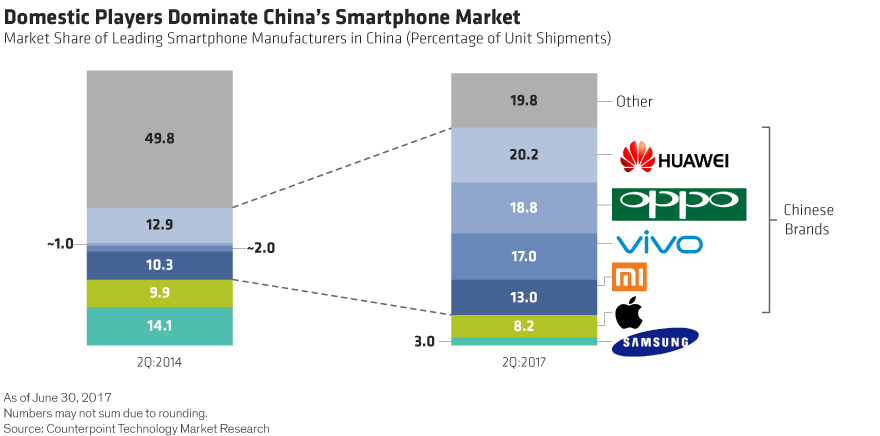

Smartphone Battles: Apple, Samsung Lose to Locals

China’s mobile handset market offers an insightful case study. Back in 2014, Samsung was a leader in China with a 14% market share. But the Korean brand has been crushed by local companies such as Huawei Technologies, OPPO and Vivo (Display). The Chinese companies offered similar products for much lower prices and understood local consumers better. For example, the Chinese firms offered higher-resolution front-facing cameras to support the local craze for selfies and more diverse color schemes for the phones.

Today, Chinese brands dominate the market with 69% of handsets, while Apple and Samsung have just 11% combined. We believe that by firmly establishing their brands as high-quality alternatives to global giants, Chinese smartphone makers are positioned to sustain domestic growth and expand abroad.

E-Commerce Brands Dominate

Internet brands also top the charts in China. E-commerce giant Alibaba controls more than 60% of the business-to-consumer market. Jack Ma, Alibaba’s co-founder, once said the company succeeded because it took off when customer acquisition was cheap. Today, any new rival would have to spend heavily to build a customer base. Alibaba’s brand lures customers through its virtual doors effortlessly and is supporting its expansion into new businesses such as offline retail, payments and cloud services.

Kweichow Moutai: Booze Brand Is Booming

China’s branding revolution goes beyond technology. Kweichow Moutai, a leading alcoholic-beverage maker, has a market cap of $128 billion. It’s the world’s most valuable liquor company, dwarfing runner-up Diageo at $90 billion. Prices for Moutai’s white liquor (baijiu) can reach US$290 for a 500-milliliter bottle.

With an estimated brand value of $32 billion in 2018, Moutai spends only 5% of revenue on advertising—much lower than the company’s Western peers. And its net profit margins of 54% are more than double Diageo’s.

In white goods, Chinese groups like Midea and Haier have improved product quality, invested in R&D and taken share from developed-market peers. Chinese brands held 85% of the refrigerator market and 70% of the air-conditioner market in 2016. Some have even acquired foreign brands to expand abroad.

Why Brands Matter for Investors

Outside China, we think the brand power of these companies is underrated. Perhaps that’s because you need to experience brands to fully appreciate them. It took years for investors to realize that Samsung was evolving from a cheap manufacturer of low-quality products to a top global brand. Even Japanese cars were once seen as inferior in the US, until a critical mass of drivers personally experienced their improved quality.

Today, many Chinese companies are delivering higher-quality products and better service, far from Western investors’ eyes. As a result, investors may not fully appreciate how brand power creates pricing power and reduces the cost of customer acquisition, both of which contribute to profit margins. And these attributes support sustainable earnings growth, which in turn helps drive stock returns.

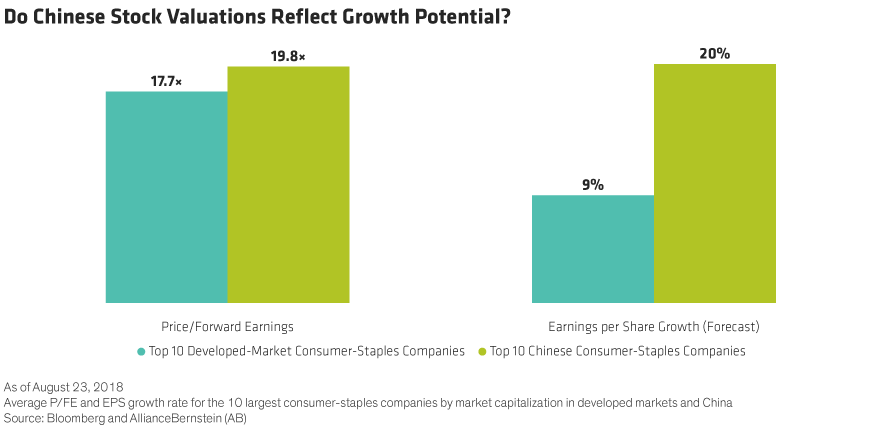

We believe Chinese brands are undervalued, given their potential to drive earnings growth. In consumer staples, valuations of the top 10 Chinese companies are about 11% higher than developed-market peers (Display). Yet the forecast growth rate of the Chinese companies is more than double.

These days, many investors in China are fixated on the escalating trade war with the US. But this concern is largely irrelevant to domestic consumer industries that are driving China’s economic growth. With a greater grasp of China’s emerging brand prowess, investors can identify resilient companies with true growth potential that can withstand the test of time.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

Logos, brands and other trademarks in this presentation are the property of their respective trademark holders. They are used for illustrative purposes only, and are not intended to convey any endorsement or sponsorship by, or association or affiliation with, the trademark holders.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein