Schwab Market Perspective: Mixed Messages Sending a Clear Signal?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Points

-

U.S. stock indexes again hit record highs but sentiment and action below the surface may indicate a less bullish picture. The uptrend should continue, but risks have risen, and we believe the signal is for investors to have a neutral stance.

-

The economy looks strong, but are housing and autos sending a different signal? The Federal Reserve again boosted rates, and looks set to continue, but are they moving from removing accommodation to tightening?

-

Higher oil prices could benefit Canadian and emerging market stocks, but also have the potential to impact central bank actions.

“I’m not lost for I know where I am. But however, where I am may be lost.”

- Winnie-the-Pooh

Mixed messages

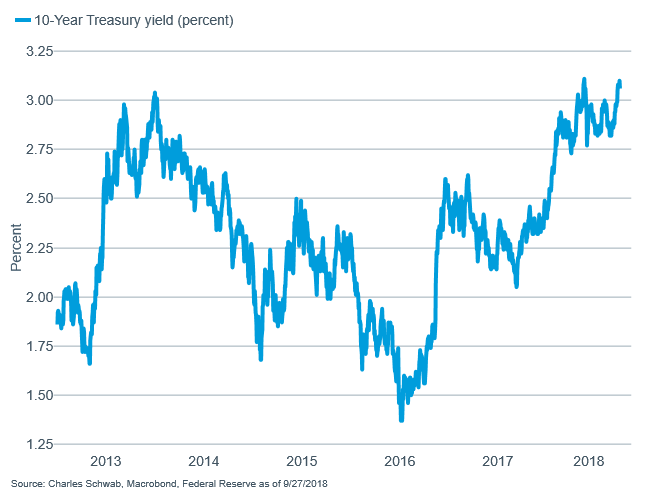

We know where we are: it’s easy to look at equity indexes in the United States hitting record highs and believe that all signs point to further bullish action. But below the surface there are some developments that we believe warrant a bit of caution. Investor sentiment is in the overly optimistic zone according to the Ned Davis Research Crowd Sentiment Poll, which can herald a near-term pullback. In contrast, investors’ actions don’t appear to match the sentiment, as money flows into equity mutual funds and exchange-traded funds (ETFs) remains negative according to Evercore ISI Research. Also, some of the former leading sectors, such as technology stocks—especially those in the social media space—have shown signs of weakness. This could represent a broadening of leadership, or a shift away from areas that are perceived as higher risk—or both. Meanwhile, the industrial sector has surged, perhaps bolstered by the recently weaker dollar, which has occurred despite 10-year Treasury yield again moving above 3%.

Weaker dollar could aid international sales

While rising yields haven’t hurt stocks…yet

Rising bond yields, however, could pose a problem for stocks in the not too distant future should the trend continue. Higher yields have made the valuation picture more difficult to justify, while they also have the potential to make fixed income securities more attractive; which could move even more money flow from equities to fixed income. Finally, stocks largely shrugged off the announcement of additional tariffs between China and the United States—perhaps relieved that they weren’t as large as might have been expected. But the threat of further escalation remains very much in play.

U.S. economy looks strong, but are there cracks below the surface?

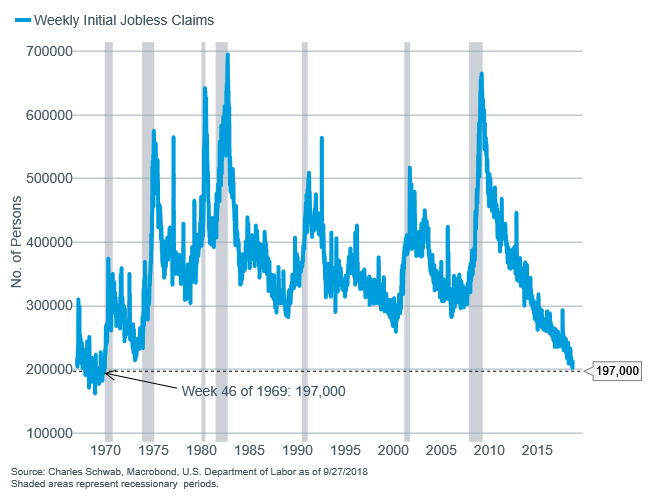

Trade disputes don’t seem to be having a significant impact on the U.S. economy as of yet, although the boost in tariffs on Chinese goods just occurred and aren’t yet reflected in the data. Business confidence remains elevated, with the National Federation of Independent Business (NFIB) Optimism Index recently hitting a record high; while capital expenditure plans remain elevated. But although both the manufacturing and services surveys done by the Institute of Supply Management (ISM) moved higher at the beginning of the month, almost half of respondents also noted they were concerned about trade. There is the risk that concern turns into action should trade disputes drag on or escalate even further. With the end of the third quarter closing in, investors will soon be able to hear the latest from management during reporting season, which we also believe is a risk to the continuing uptrend in stocks. With estimates for S&P 500 year-over-year earnings growth standing at about 21%, the bar is set quite high, and it could be difficult for the majority of companies to beat those elevated estimates. For now, earnings growth remains a support for stocks, and the healthy corporate picture is boosting the consumer via job growth and confidence. Initial jobless claims are at their lowest levels since the late-1960s and now “threatening” to move below the 200k mark, which is almost unheard of.

Jobless claims historically low…

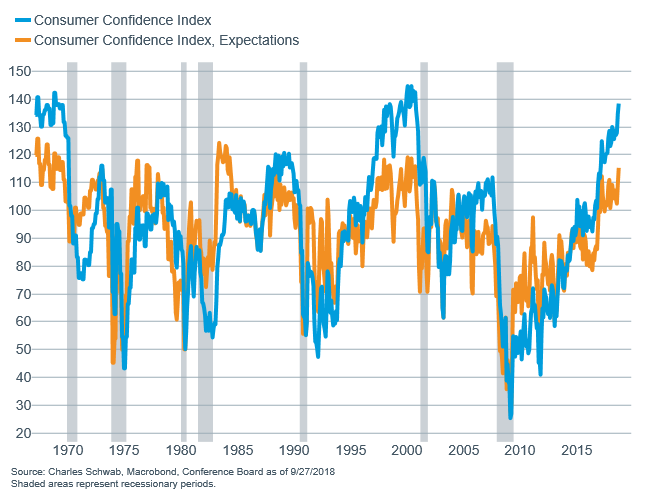

The strong labor market has boosted consumer confidence, which continues to hover near record highs. Which brings another cautionary note, we don’t know if this is the high for consumer confidence, but stocks have tended to struggle mightily following what in hindsight has been highs in consumer confidence.

…helping consumer confidence reach historic highs…

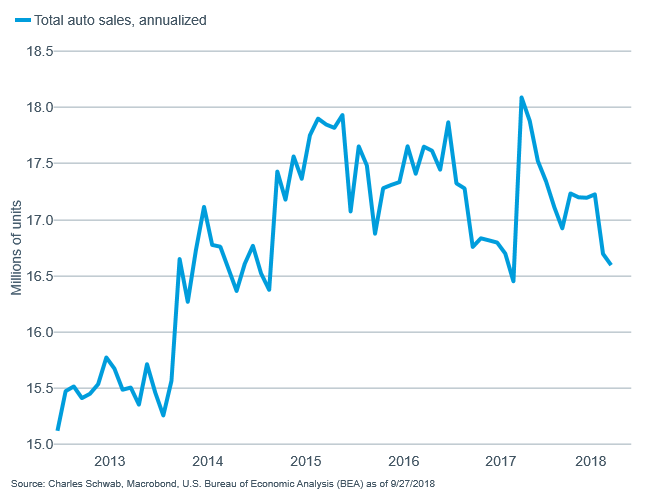

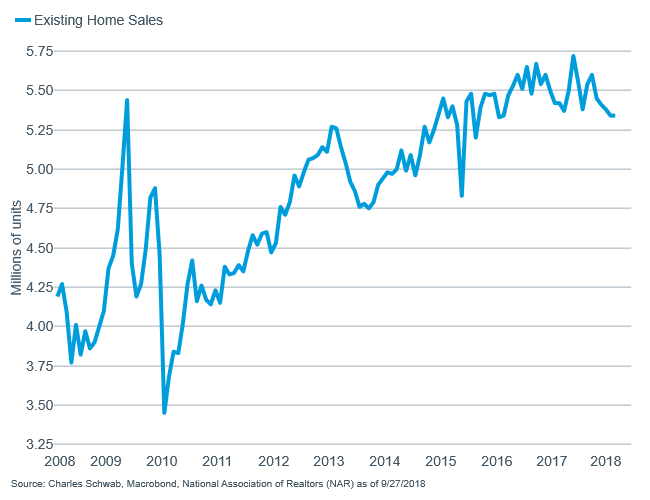

But here too we have a bit of a mixed message. Confidence is high but auto and home sales have been weaker (for more on housing read Liz Ann’s article With or Without You: Can the Economy Still Hum if Housing Falters?).

…but auto sales have weakened…

…and housing looks sluggish.

We like to look at actions more than words and consumers’ actions appear to us to be still relatively cautious. Expectations for the holiday shopping season (yes, already thinking about that) are likely to be elevated given the strong economy, but if consumers remain cautious, there could be some disappointments in store.

Much like the stock market, we think the trend in the economy will continue higher and that a recession is not in the near-term cards; but upside surprises may be difficult to come by, potentially limiting potential market gains as we finish out the year.

Fed sending mixed messages as well?

The Federal Reserve again surprised no one by raising rates this week and did little to dissuade rising expectations of another hike in December (for more on the Fed decision read: Tighten Up: Fed Raises Rates Again). But while they are expressing little concern of overheating inflation and have shown no desire to crimp economic activity, the Federal Open Market Committee (FOMC) removed the reference to policy remaining “accommodative;” in keeping with the real (inflation-adjusted) federal funds rate now being in positive territory for the first time post-financial crisis. Coupled with the ongoing shrinkage of the Fed’s balance sheet, monetary policy has moved from loose to tighter (if not yet tight). We don’t believe the Fed has a desire to hurt stock prices, but the possibility of a monetary policy mistake adds to our belief that a neutral stance in U.S. stocks remains appropriate.

Oiled up

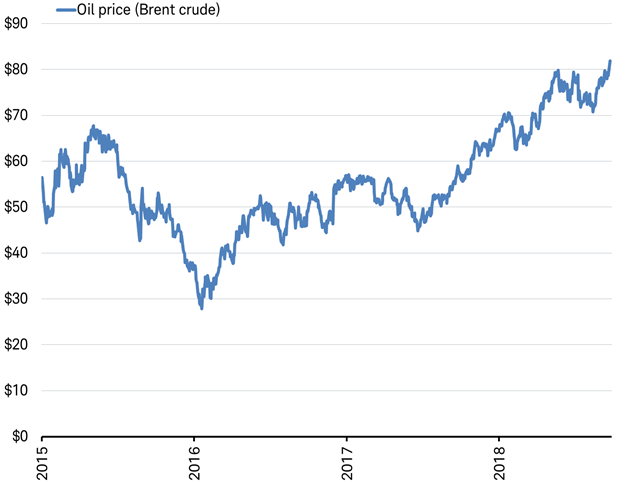

As mentioned, much attention has been focused on President Trump’s trade policies and his confrontation with China, and for good reason; but his confrontation with Iran may be having more of an immediate impact in the markets. The global benchmark for oil is Brent Crude and the price of a barrel is up 22% this year with a 15% increase in just the past five weeks—bringing the price to $82, the highest level since 2014.

Oil price highest in years

Source: Charles Schwab, Bloomberg data as of 9/25/2018.

Past performance is no guarantee of future results.

Price is per barrel.

Despite President Trump’s mentions of OPEC “ripping off the nations of the world” and his calls on Twitter for OPEC to lower prices, crude oil prices are rising. Members of OPEC and other producers are struggling to make up for Iran's falling production, which is trailing off ahead of U.S. sanctions going into effect on November 4. The International Energy Agency (IEA) noted in their latest Oil Market Report that “evidence provided by tanker tracking data suggests that Iran's exports have already fallen significantly.” The half million barrels per day of reduced production seen so far may grow.

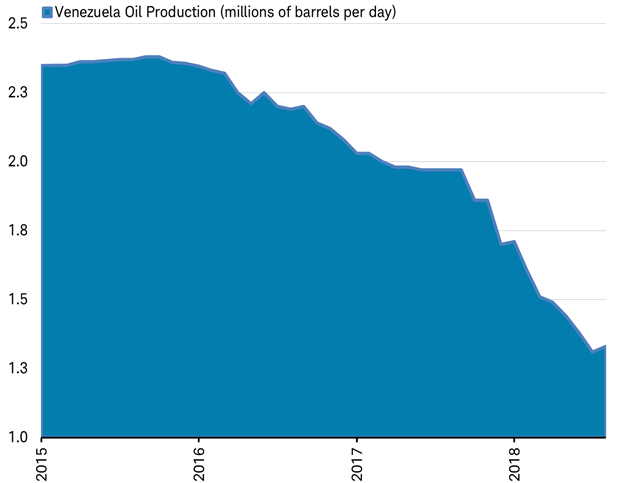

The majority of production taken offline by OPEC member countries in the past year or so has largely been from declines that don’t appear to be easily or quickly brought back. For example, Venezuela's production has collapsed by nearly 1 million barrels per day since 2015. Half of that decline came this year as that country’s economic collapse has intensified.

Plunging Venezuela production

Source: Charles Schwab, Bloomberg data as of 9/25/2018.

OPEC production is down 1.5 million barrels per day from its peak a few years ago (International Energy Agency, IEA). In contrast, U.S. oil production has risen by 1.5 million barrels per day from a year ago to 11 million barrels a day according to the Energy Information Agency (EIA). However U.S. production plateaued this summer due to infrastructure bottlenecks. Production from Libya has returned to near 1 million barrels per day, but remains vulnerable to disruption. Meanwhile, demand for oil continues to rise, with an expected increase of 1.4 million barrels per day in 2018 and 1.5 million in 2019, per the IEA. As a result, oil inventories are falling: as of the end of July they were 50 million barrels below the five-year average. These factors may provide support for higher oil prices to persist.

If oil prices remain elevated or move higher, there may be winners and losers. Historically, two winners from higher oil prices are likely Canadian and emerging market stocks.

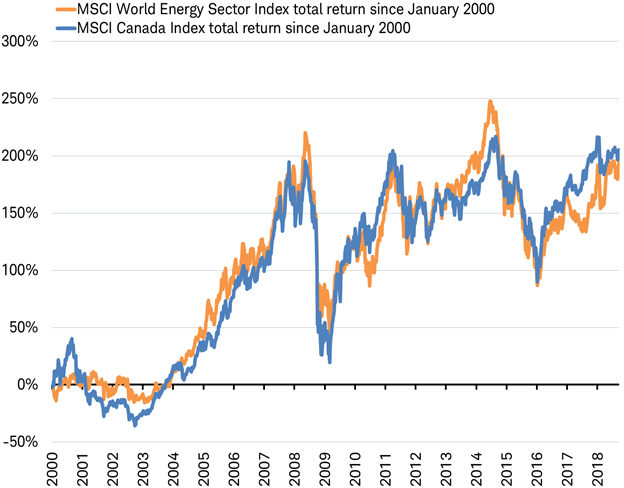

- The energy sector tends to move with oil prices and that may be good news for Canadian equities. Energy is not the biggest sector of the Canadian stock market, but energy carries broad implications for the Canadian economy and companies. In fact, world energy stocks and the Canadian stock market have moved together closely for two decades, as you can see in the chart below.

From the same barrel: Canada and energy stocks

Source: Charles Schwab, Bloomberg data as of 9/25/2018. Past Performance is no guarantee of future results.

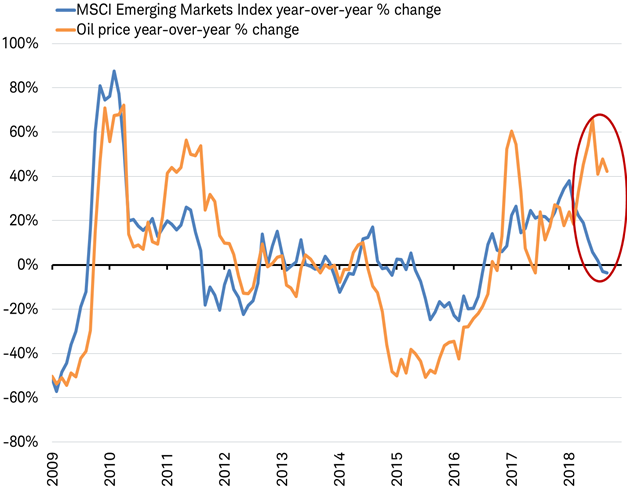

- Emerging market (EM) stocks also have usually performed well when oil prices are rising. But that relationship has become stretched in 2018 with EM stocks sliding as oil has risen, as you can see in the chart below. This divergence may suggest either a snapback in EM stocks or moderating oil prices in the months ahead.

Decoupling: emerging market stocks and oil prices

Source: Charles Schwab, Bloomberg data as of 9/25/2018. Past Performance is no indication of future results.

What about losers from high oil prices? Higher oil prices can act as a drag on global growth. Counterintuitively, they also usually act as a boost to global aggregate corporate earnings. The energy sector, which benefits from higher prices, comprises about 16.6% of the earnings of companies in the MSCI World index. This share exceeds the 9.5% from consumer discretionary sector and 0.6% from the airline industry, where the drag from higher oil prices is felt the most.

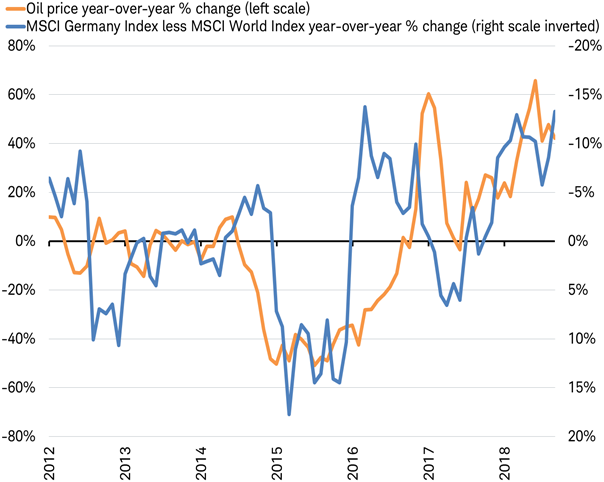

Demand for consumer discretionary products can be impacted negatively by higher energy prices, especially for cars. The auto-driven German stock market illustrates this closely, with Germany underperforming the rest of the world as oil prices rise, as you can see in the chart below (the scale for German stock market performance relative to the rest of the world is inverted to show how closely it tracks oil prices but in the opposite direction).

Source: Charles Schwab, Bloomberg data as of 9/25/2018. Past performance is no indication of future results.

The push and pull on oil prices from U.S. policies seems to be balancing out in the form of higher prices, which may benefit Canadian and emerging market stocks, and act as a drag on Germany. More broadly, this may push up headline inflation readings and force global central banks to consider responding with higher rates than currently expected by the markets, which could bring about a premature end of the business cycle. Typically central banks “look through” increases in energy prices that tend to have a temporary effect on inflation and don’t result in prices rising across economies. If that ends up being the case this time, the impact on stock prices and economic growth could also be temporary. We’ll be watching closely.

So what?

Recent records in the U.S. stock market do not, in our view, mean that investors should get more aggressive in their investment stance. High expectations, elevated investor sentiment, trade disputes, and the possibility of a monetary mistake lead us to take a more cautious stance. In particular, the aforementioned surge in oil prices could eventually take a bit out of the U.S. economic expansion as oil price spikes have often contributed to recessions unfolding. In the meantime, the bull market should continue, with a solid economic and earnings backdrop, but gains are likely to be more muted and bouts of volatility and corrective phases are more likely. Higher oil prices do have potential winners in the form of Canadian and emerging market stocks and have an impact on central bank actions, so we’ll be watching developments in the energy space closely.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Ned Davis Research (NDR) Sentiment Poll shows perspective on a composite sentiment indicator designed to highlight short- to intermediate-term swings in investor psychology.

The Intercontinental Exchange (ICE) U.S. Dollar Index is an index of the of the United States dollar relative to a basket of foreign currencies, and is a weighted geometric mean of the dollar’s compared to the Euro (EUR), Japanese yen (JPY), Pound sterling (GBP), Canadian dollar (CAD), Swedish krona (SEK) and Swiss franc (CHF) relative to March 1973.

The National Federation of Independent Business (NFIB) Small Business Optimism Survey which is based on the responses of 740 randomly sampled small businesses in NFIB's membership, surveyed monthly.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Institute for Supply Management Non-manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms' purchasing and supply executives, within 60 sectors across the nation, by the Institute of Supply Management (ISM). The ISM Non-Manufacturing Index tracks economic data, like the ISM Non-Manufacturing Business Activity Index.

The Consumer Confidence Index is a survey by the Conference Board that measures how optimistic or pessimistic consumers are with respect to the economy in the near future

MSCI Canada Index is designed to measure the performance of the large and mid cap segments of the Canada market. With 90 constituents the index covers approximately 85 % of the free float-adjusted market capitalization in Canada.

MSCI World Energy Index is composed of more than 1,400 stocks listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. The MSCI World Energy Index is the Energy sector of the MSCI World Index.

The MSCI Emerging Markets Index captures large and mid cap representation across 23 Emerging Markets (EM) countries*. With 1137 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country

The MSCI Germany Index is designed to measure the performance of the large and mid cap segments of the German market. With 67 constituents, the index covers about 85% of the equity universe in Germany.

The MSCI World Index captures large and mid-cap representation across 23 Developed Markets (DM) countries. With 1,648 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The S&P 500 Composite Index is a market capitalization-weighted index of 500 of the most widely-held U.S. companies in the industrial, transportation, utility, and financial sectors.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© 2018 Charles Schwab & Co., Inc, All rights reserved.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All