The stock market has clearly entered a more volatile phase; in keeping with late-cycle tendencies and evident risks about which we’ve been writing all year. It’s too soon to declare the bull market over, but we’d caution against adding risk to portfolios.

Earnings season has been decent on its face, but investor reaction has often been severe. For both earnings and the economy, we are likely past the peak in growth rates. Meanwhile, Fed uncertainty is adding to the consternation of investors.

Global stock markets have struggled as the season of “sugar highs” appears to be coming to an end.

“There is a time for everything, and a season for every activity under the heavens.” - Ecclesiastes 3:1

Seasonality changes

The last several weeks have brought a distinct change in market behavior and character; with elevated volatility, triple digit moves in the Dow back in vogue, and the NASDAQ and Russell 2000 (small caps) entering correction territory.

Volatility has increased

This shouldn’t be much of a surprise as interest rates have moved higher, financial conditions have tightened, worries about peak growth have increased, trade concerns have grown, midterm election rhetoric has escalated, global growth has slowed, and Fed uncertainty has risen. Put this more uncertain “season” on top of the worst month of the year historically for equity returns and you have the recipe for more volatility. But a potential positive offset is that we’re entering what has historically been a strong seasonal period for the markets. Novembers and Decembers of midterm election years have historically been quite strong. And in all years, going back to 1952, the three-month period beginning in November has been the best three months of the year. Of course past performance is no guarantee of future results but it can be comforting to have some historical tailwinds.

Additionally, the recent uptick in volatility has allowed investor sentiment—a contrarian indicator—to drop out of the excessive optimism zone according to the New Davis Research (NDR) Crowd Sentiment Poll (which aggregates seven distinct sentiment measures). This could provide more near-term support for stocks and set the stage for further relief rallies. That said, we remain cautious about equities and continue to recommend investors take no risk beyond their longer-term strategic U.S. equity allocations, and use volatility to rebalance as necessary. We have also expressed this caution with our bias toward large caps over small caps; and our sector recommendations, which have become more defensive in nature, offering a ballast within equity portfolios (for more see Interested in Some Defense?) .

Peak season?

Earnings season has been decent as far as results go to this point but as we often say, “better or worse matters more than good or bad.” Earnings growth rates have been trending down this year, from 27% in the first quarter, to 25% in the second quarter, to an expected 24% in the third quarter and an expected 19% in the fourth quarter (according to ThomsonReuters). But growth then takes a meaningful dip in 2019; largely thanks to simple “math:” Once we move into 2019, earnings will be compared in year-over-year growth rate terms with the tax-cut juiced earnings of this year. Expectations are for 8-9% earnings growth for next year’s first half (ThomsonReuters). And although current earnings remain strong and the “beat rate” remains healthy at more than 80%, investors’ reaction to results has been fairly severe. According to Bespoke Investment Group, for the third quarter earnings season through October 24, the one-day decline for earnings misses averaged nearly -5%; but perhaps more telling is that even earnings beats saw an average decline (albeit a slight one). Additionally, tariff concerns are increasingly being mentioned in corporate conference calls according to data from FactSet, which could impact companies’ willingness to spend on capital expenditures as well as dent profitability. As an aside, the latest Federal Reserve’s Beige Book report on the economy had a rash of references to pessimistic corporate commentary associated with tariffs’ impact on business. And the major area of concern, the Unites States’ dispute with China, shows few signs of thawing, with both administrations appearing to dig in their heels.

The tariffs are not yet having a discernable impact on the U.S. economy, with industrial production continuing to move higher (see first chart below) and most regional surveys such as the Empire Manufacturing Index remaining elevated (the Richmond Fed survey was decidedly less rosy). In addition, if the remaining pending and potential tariffs kick in, the impact on U.S. gross domestic product (GDP) will become more significant (see second chart below).

Little sign of tariff trouble here, yet…

…but the potential for impact is noticeable.

Source: Charles Schwab, Cornerstone Macro.

In addition, we are seeing some cracks in the housing and auto industries (see charts below) as it appears that higher interest rates may be taking a toll on both, and tariffs adding to that negative force for autos. Whether they are canaries in the coal mine is yet to be seen; but we do believe the risk of a recession within the next year or two is higher than the consensus believes, especially if we continue to slide deeper down the trade war rabbit hole.

Housing showing some weakness…

…as affordability declines…

…as interest rates rise…

…which could be impacting autos as well (despite uptick last month).

Open season on the Fed?

The rise in interest rates, and resulting heighted volatility in equities, has resulted in elevated uncertainty as to whether the Fed can smoothly navigate the monetary policy normalization process without a “mistake.” The Fed’s continued hawkish tilt, as seen in the recently-released Federal Open Market Committee (FOMC) minutes, has raised concerns about the Fed moving too quickly or too far—especially given still-subdued inflation. The core consumer price index (CPI) is up a modest 2.2% over the year ago period, but that is above the Fed’s 2% target. And although wage growth has been slow in coming this cycle, it has picked up pace more recently.

Inflation modest…

…as are wage gains

There are broader inflationary signs simmering below the surface. Tariffs, as mentioned above, are typically inflationary: as U.S. companies face rising tariff costs associated with imports, they often pass those “taxes” on to consumers. And the labor market continues to tighten, with the number of available jobs recently outpacing the number of available workers by more than 900k. It’s likely that companies are going to have to increase wages in order to lure workers away from other employers—also inflationary if it should start to take hold.

Worker shortage could add to inflationary pressures

We continue to believe that the Fed has little desire to slow down economic growth and will continue to be cautious, but if inflation takes hold it will behoove the Fed to keep tapping on the brakes; arguing for a more cautious stance by investors.

Halloween marks end of a “sugar high”

As of October 24, the MSCI World Index was down 3% for the year-to-date, after last year’s gain of 22%. Yet, for both years, global GDP growth is expected to be 3.7%, and earnings growth is in the double-digits (ThomsonReuters). While some might point to trade tensions posing a risk to future global growth as a primary cause of the difference in performance, it may also be something few have pointed to: tax cuts.

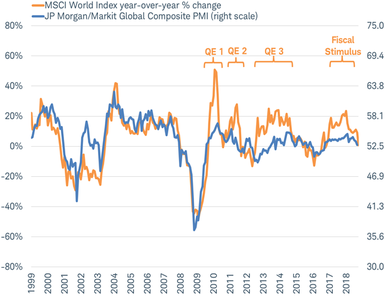

The global composite Purchasing Managers Index (PMI) is a widely-watched and timely economic indicator incorporating over 30 countries and representing about 85% of global GDP. Global stock market performance (in orange) and the economy—as measured by the global composite PMI (in blue)—have generally tracked each other over the past 20 years since the inception of the PMI. As you can see in the chart below, global stock market performance has now reconnected with the underlying trend in the global economy.

Stocks and economy have reconnected

Source: Charles Schwab, Bloomberg data as of 10/23/2018. Past Performance is no guarantee of future returns.

Global stock market performance has rarely disconnected for long from the global economy. Each disconnect was related to a stimulus “sugar high”—the first three disconnects were during the Federal Reserve’s quantitative easing (QE) programs. Although those bond buying programs appeared to do little to lift global economic performance as measured by the PMI, the monetary stimulus did lift stocks during the duration of those programs. In 2017, rising expectations of fiscal stimulus in the form of tax cuts bolstered investor optimism and pushed the global stock market higher, prompting another disconnect. That wave of optimism peaked as tax cuts took effect in January in the United States, France and Japan. Since January of this year, the “sugar high” has faded; acting as a drag on performance this year, with stocks slumping as they have reconnected with the economic reality measured by the PMI.

Maybe it is ironic that a holiday known for candy, Halloween, has marked the end of the “sugar high” for stocks. While the reconnect may mean the end of the drag on global stock market performance, even if the global PMI stabilizes at the current level in the coming months, it points to relatively flat performance for stocks (as you can see in the chart above). It may take a lift in global economic growth to see global stocks deliver gains. It is possible that this may come as the economic stimulus being applied in China in recent months begins to be felt; or if another round of fiscal stimulus in the United States is introduced. However, the likely outcome of the U.S. midterm elections may make it hard to produce another major fiscal stimulus boost (for our latest take on the mid-term elections see: Midterm Elections: What’s at Stake in the House?).

So what?

October has again been a scary month for investors, even though past performance does not indicate future results, history shows that stocks tend to face a seasonal tailwind heading into the end of the year. There will likely be more volatility but at least overly optimistic investor sentiment has eased, U.S. economic growth remains solid, and the midterm elections will soon be over, all of which could trigger at least a relief rally off the recent lows. But gains both here and globally are likely limited by myriad late-cycle pressures. Remain disciplined, consider diversification and rebalancing, and consider establishing a more tactically defensive positioning.