Recent volatility reminds us that new risks are testing standard defensive equity strategies. Portfolios that offer downside protection need to go beyond standard risk models and position themselves for changing challenges ranging from trade wars to European political instability.

Managing risk is an integral component of any investing strategy. But standard risk-management tools aren’t always adequate. Tracking error, for example, tells you how much a portfolio deviates from its benchmark, yet it doesn’t really indicate how hard performance might suffer in a market meltdown. Meanwhile, standard risk models are built to work on averages, over long periods of time, but aren’t designed to predict the potential fallout from specific events such as trade wars or Brexit.

Looking Out for Unexpected Risks

Portfolio managers must constantly be on the lookout for new risks. Of course, a solid strategy will be built on clear investment and risk-management processes. But even the best-laid plans can’t anticipate the myriad challenges that will arise along an investment journey.

In today’s markets, risk is a moving target. But three big risks that surfaced this year have escalated in recent weeks. Each requires a creative response. The goal should be to identify companies that are vulnerable as well as those that may present opportunities amid the uncertainty.

Risk 1: Trade Wars

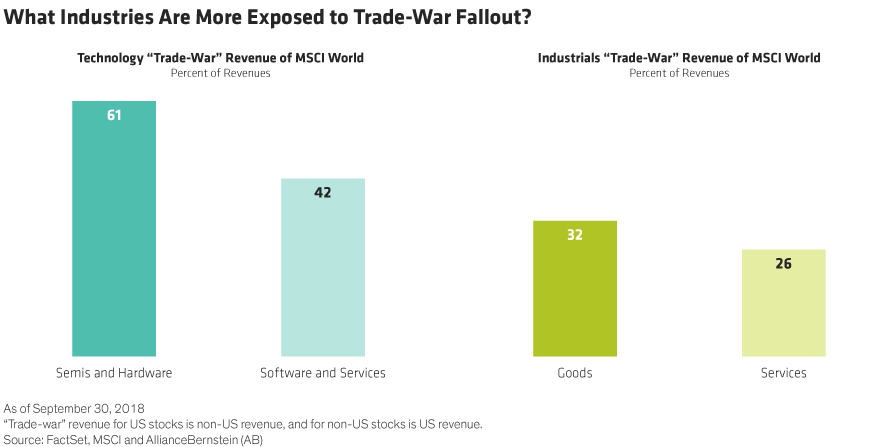

The US-China trade war tops the list of new risks. Nobody can predict how it will unfold, so it would be imprudent to position a portfolio for a particular outcome. Still, it’s important to figure out which types of companies could get caught in the crossfire if things get worse. The technology and industrial sectors are both more exposed to trade winds than most. Yet a closer look within the sectors reveals that not all companies are equally at risk.

We assessed the revenue that is susceptible to trade wars within each sector as well as within key subindustries. For US companies, we defined non-US revenue as exposed, while for non-US stocks, we defined US revenue as exposed. Technology stands out as particularly exposed, but in the semiconductor and hardware industries, about 61% of revenue is at risk, while in software and services, only 42% of revenue is exposed (Display). Within industrials, about a third of industrial goods are exposed to trade wars versus 26% of services revenue. When we search for individual stocks within these sectors, companies with more revenue exposed to trade wars should be handled with care, in our view.

Risk 2: China’s Slowdown

Emerging markets have had a tough year. Uncertainty about China has been one of the big risk factors for investors in the developing world as the world’s second-largest economy struggles to manage a slowdown of growth. At the same time, China is trying to reduce debt levels across its economy and improve its environmental performance. These huge tasks are further complicated by the trade war with the US.

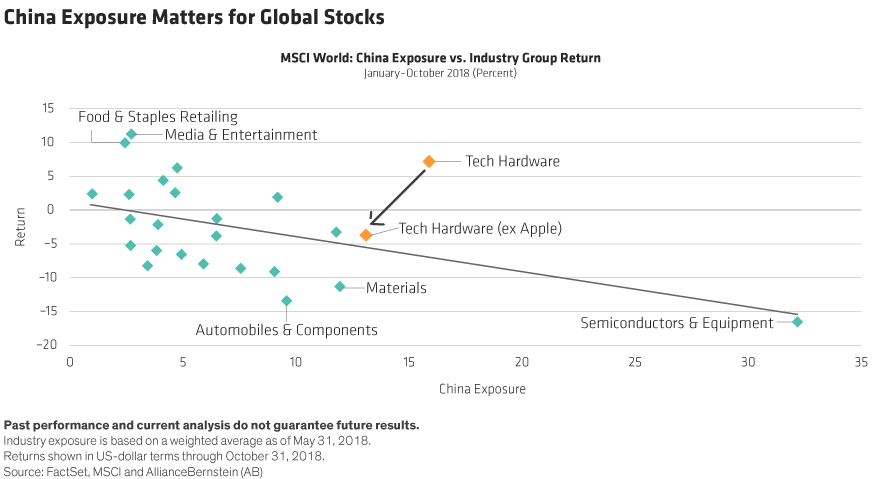

In this environment, investors need to be wary of companies with a large exposure to China. For example, our research shows that the returns of global stocks in industries with greater exposure to China, such as materials and semiconductors, have been hit especially hard (Display). Industries with less exposure to China, such as media and food retailing, have fared relatively well.

Looking even closer, the one real outlier, tech hardware, is largely driven by the results of Apple. When Apple is excluded from the industry (the orange diamonds in the Display above), the pattern holds up really well.

We’re not suggesting that investors avoid China completely. China is still home to many exciting companies that offer global investors access to the country’s long-term growth story. But it’s important to look beyond the obvious pockets of risk. For example, supply chains that run through China in diverse industries ranging from technology to clothing may get tangled up in China’s challenges. So a highly risk-aware approach is more important than ever.

Risk 3: European Politics

In Europe, multiple political risks are unsettling markets. Italy’s populist government is in a standoff with the European Commission over plans to increase public spending, which threatens to fuel borrowing costs in an already shaky economy. And the ongoing Brexit negotiations have left a cloud of uncertainty over Britain’s economic future.

Financials are widely seen as a sector at risk to the Italian issue. However, some businesses, like property and casualty insurers, are much less vulnerable to these risks than are commercial banks. And exchange companies might even benefit as the anxiety fuels trading.

Similarly, for stocks listed in the UK, it’s not all about Brexit. Many large multinational companies that are based in Britain actually have little direct exposure to the domestic economy. Other sectors, like consumer discretionary, may get caught up in post-Brexit weakness, if the domestic economy takes a hit from unfavorable trade terms.

Shifting Defensive Formations

Managing each of these risks requires a similar mindset. For all three situations, understanding the drivers of risk, and what types of companies are really vulnerable, is the first step toward developing a defensive plan. Move away from standard risk models. Look for thematic exposures to changing risks and identify vulnerable sectors and industries.

Delivering downside protection requires constant refining and adjusting. Portfolio managers who aim to reduce losses in downturns must be prepared to shift their defensive formations regularly and to look in new directions for stocks that can help anchor stability in an allocation as the risk landscape changes.

The value of an investment can go down as well as up and investors may not get back the full amount they invested. The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein