With cabinet ministers resigning by the hour, it’s tempting to think that British Prime Minister Theresa May’s Brexit deal with the European Union (EU) is dead on arrival, and that a hard Brexit is now the most likely way forward. But some form of soft Brexit is still the most likely scenario, in our view.

Brexit is a ferociously complicated and divisive subject, and it was always going to be like this as we entered the end game. In Brexit jargon, the meaning of “soft” and “hard” Brexit has changed a lot since the June 2016 referendum on EU membership. Initially, soft Brexit meant the UK opting for a Norway-style relationship with the EU while hard Brexit meant leaving on World Trade Organization (WTO) terms (in the worst case) or opting for a Canada-style trade deal.

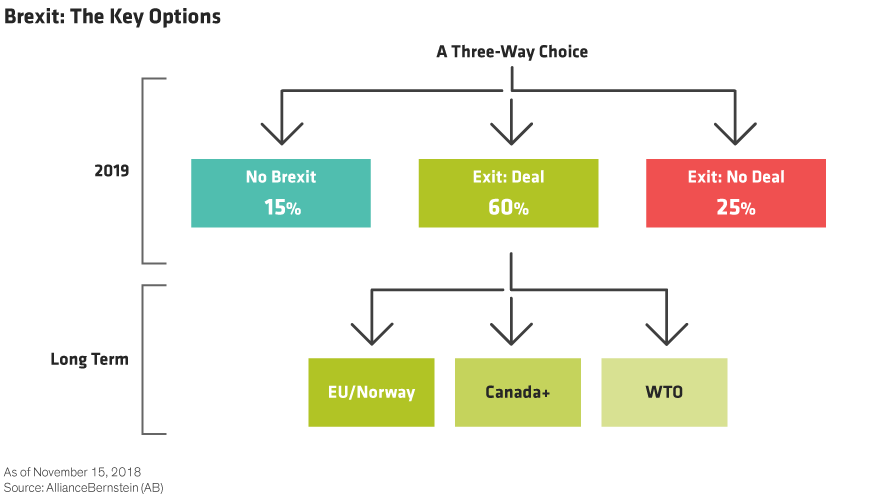

From a longer-term perspective, these choices are still hugely important, but the terms soft and hard Brexit now mean something quite different: whether the UK leaves with a deal that provides a smooth transition to its (undecided) future trading relationship with the EU or whether it crashes out of the EU without a deal at all (Display). Looked at this way, these two scenarios might be better thought of as exit-deal Brexit and no-deal Brexit. The other possibility, of course, is that after making an enormous amount of fuss the UK backtracks and withdraws its request to leave the EU.

What is the likely impact of these different scenarios?

Exit-Deal Brexit (60% Probability)

Assuming a deal was reached, the UK would enter a transition phase next March. During this time, its trading relationship with the EU wouldn’t change—but uncertainty about the end game would remain high. In other words, the threat of near-term economic chaos would recede but the overall backdrop would be much the same as now.

This would give a small boost to the economy, with the pound likely to benefit from a perceived reduction in Brexit risk. But there would still be considerable uncertainty about the nature of the UK’s future trading relationship with the EU, so we doubt that the impact would be material.

Longer term, there are several routes forward under this scenario. One possibility is that the UK could remain permanently in the “temporary” customs union that both sides hope will help sidestep the complex issues created by the Northern Irish land border with the EU. Otherwise, all these options would be on the table:

•A return to the EU

•The Norway option (a slightly watered-down version of EU membership)

•An enhanced version of the trade deal that Canada recently struck with the EU

•A move to WTO terms

Each of these potential outcomes would have very different implications for the UK economy and asset prices, but they’re unlikely to become relevant until 2020 or well beyond.

No-Deal Brexit (25% Probability)

A hard Brexit would be hugely damaging for the British economy and the resulting disruption would probably catapult the UK into a major recession—the UK is an island and virtually no preparations have been made for a no-deal Brexit. The pound would fall sharply, perhaps toward parity against the US dollar, and the Bank of England would probably cut interest rates and resume quantitative easing. Moreover, the government would struggle to survive such a calamity, which means the pound and gilt market might have to adjust to life under a Labour government intent on pursuing a far-left agenda.

But that’s not where the bad news from a no-deal Brexit ends. The rest of Europe would not be as badly hit by a no-deal Brexit as the UK, but it’s hard to imagine that it wouldn’t be significantly impacted (consider the financial linkages between the UK and the rest of Europe as well as London’s role as Europe’s financial hub). This blow would come at a time when European growth is already slowing and the market is beginning to question debt sustainability in Italy. In our view, a hard Brexit could unleash a second phase of the sovereign-debt crisis and has the potential to become a globally systemic event.

Against this background, Prime Minister Theresa May is trying to get her Brexit deal through Parliament. The problem is that she has negotiated an agreement that virtually nobody likes. Ultimately, the government’s strategy boils down to a high-stakes game of political poker in which her chances of getting the deal through Parliament rest on the hope that enough MPs will regard any deal—no matter how bad—as better than the disruption caused by a hard Brexit.

No Brexit (15%)

But there’s a third possibility, which is that the UK decides to withdraw its request to leave altogether. This would be the most positive near-term outcome for the economy. But how likely is it? It would require a second referendum in which the British public reverses the exit decision of 2016, while the EU would have to push back Brexit day from March 29 (there simply isn’t enough time for a referendum before then). These requirements make it a tall order and the least likely of our three scenarios, but it’s one for which parliamentary and public support is slowly starting to build.

What Happens Now?

It’s almost impossible to predict how things will develop in coming weeks. The prime minister looks increasingly likely to face a leadership contest and, even if she survives, the odds are heavily stacked against her winning a parliamentary vote on her Brexit deal.

But that’s unlikely to be the end of the story. Very few people voted for the chaos that a no-deal Brexit could unleash, and it’s an outcome that neither the UK nor the EU wants. But like Greece a few years ago, the British Parliament may need to stare into the abyss before taking decisive steps to avoid it. In the meantime, markets should be prepared for even more volatility.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

© Franklin Templeton Investments

© AllianceBernstein

Read more commentaries by AllianceBernstein