Debt Bulge Raises Stakes for US Equity Investors

US corporate debt has surged over the past decade. As rates begin to rise from historic lows, focusing on quality companies with healthy balance sheets can help equity investors avoid danger zones.

Ultralow interest rates have fueled financial markets for years. Many companies have taken advantage of the comfortable financing conditions to increase borrowing. But as conditions change, higher rates could force investors to confront some nasty side effects of the easy-money policy.

GE’s Debt Troubles: Sign of a Deeper Malaise?

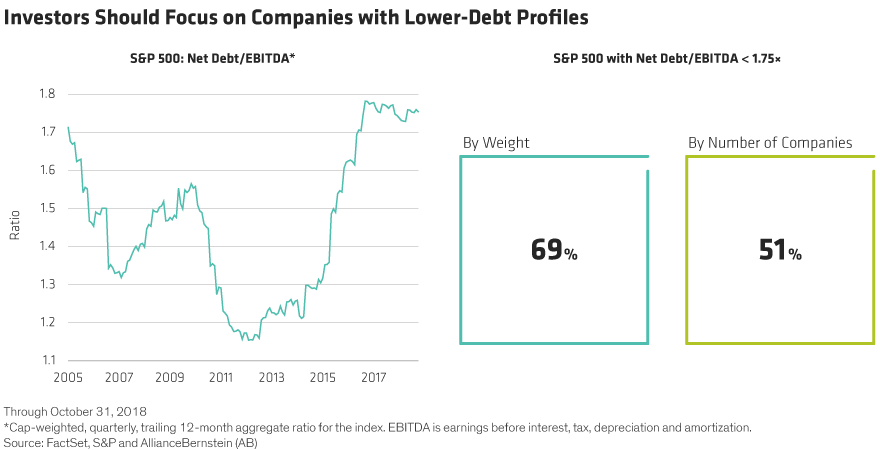

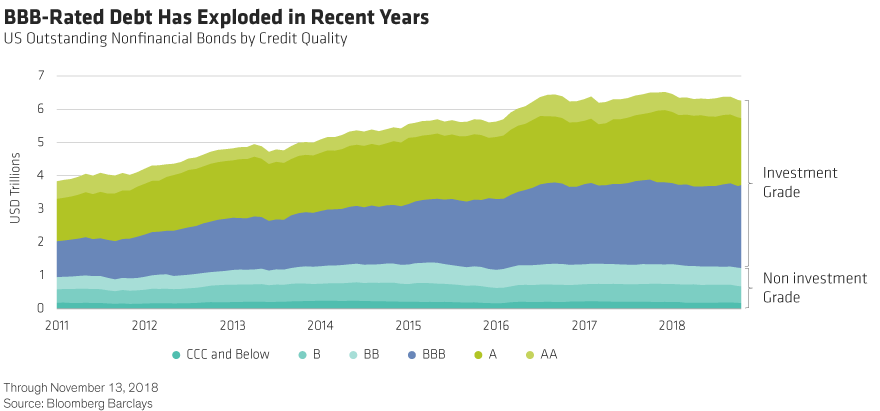

US outstanding nonfinancial bonds have risen by 63% to $6.3 trillion since 2011 (Display). And the S&P 500’s net debt/EBITDA—a measure of corporate indebtedness—ballooned by more than 50% in late 2011 to 1.75x today. What’s really worrying, though, is how much of that borrowing binge is being driven by lower-quality companies. Debt with a BBB credit rating—at the lower end of investment-grade credit—has more than doubled since 2011 and represents about 50% of the US investment-grade bond index today.

GE’s troubles illustrate the risks. In recent weeks, the company’s shares have plunged and its credit ratings were cut to BBB, putting it on the brink of slipping into noninvestment-grade status. Although GE’s troubles are rooted in its history of excessive borrowing to fund bad acquisitions and share buybacks, its predicament should be ringing alarm bells. In a market saturated with BBB debt, companies that have borrowed too much, like GE, could be pushed over the edge as rates rise.

Deteriorating Debt Quality and Rising Rates: A Toxic Combination

High rates would boost financing costs for companies saddled with too much floating debt. Rising inflation could increase costs and squeeze profit margins, which could cause coverage ratios to deteriorate and trigger debt downgrades. This scenario, in turn, would push funding costs even higher in a potentially devastating debt spiral. To make matters worse, when the debt squeeze comes, companies that levered up to buy back shares at high valuations could be forced to issue equity at trough valuations to delever.

Of course, investors should always scrutinize company balance sheets. These days, we think it’s more important than ever. Deteriorating debt quality and rising rates are a toxic combination that could ultimately undermine earnings and stock prices, in our view. There are signs that this situation is already happening. Our research shows that stocks of US companies with high leverage underperformed stocks of companies with low leverage by 7.2% as of this year through the end of October.