Recent market gyrations have many people asking: Is it time to pivot from a growth equities allocation to a value equities allocation? But that’s the wrong question. Instead of asking which style is likely to outperform, investors should be asking why they’re performing differently.

US growth stocks surged for much of 2018. In the first three quarters, the Russell 1000 Growth Index advanced by 17.1%, outperforming the Russell 1000 Value Index by 13.2%. But as the markets became more challenging in October, the value index outperformed the growth index by 7.1% through the end of November.

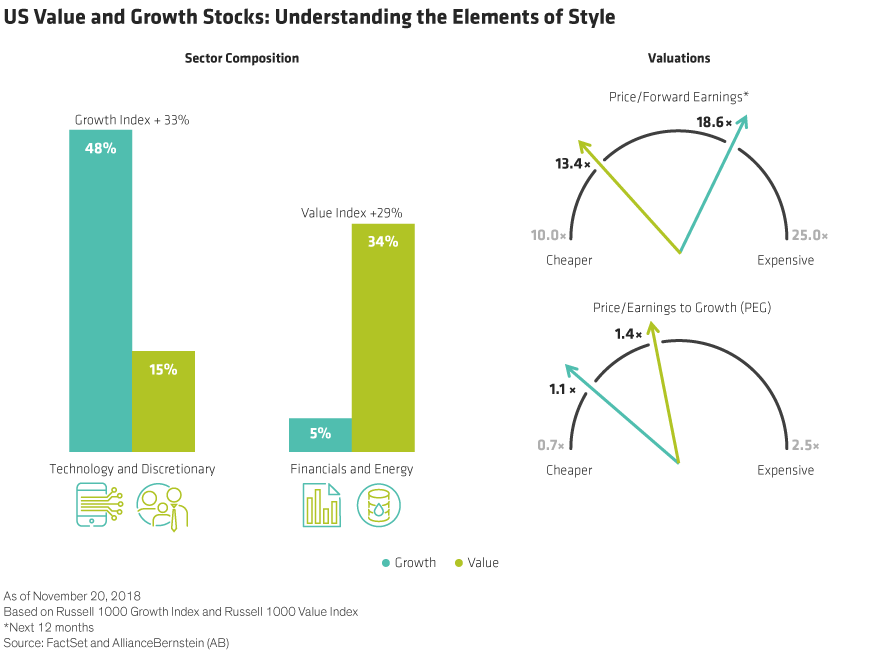

Sector Weights Fuel Performance

What’s behind these performance patterns? Each index is tilted toward different sectors (Display, left). The growth index has large weights in consumer discretionary and technology stocks—both which underperformed in the recent sell-off. The value index is heavily concentrated in the energy and financial sectors. That means its performance is often heavily influenced by the direction of oil prices (which are slumping) and interest rates (which are rising). In October and November, US financial stocks held up relatively well versus other sectors, which supported the relative resilience of value stocks as the broader market declined.

Valuations Are Complex

Valuations are also tricky (Display, right). Based on price/forward earnings—perhaps the most popular valuation metric—value stocks are about 28% cheaper than growth stocks, which are trading at 18.6x. But based on price/earnings to growth (PEG), the growth index is about 21% cheaper than the value index.

Sound confusing? Not really. It just means that after a nine-year bull market, and at a late stage in the US economic cycle, a simplistic choice between value or growth isn’t quite enough. Selective investors can find attractive candidates in both styles. Companies with solid balance sheets and low levels of debt that don’t depend on the economic cycle for growth are good growth candidates, in our view. On the value side, stocks with attractive valuations that stand to benefit from a promising catalyst are worth considering. Value and growth aren’t going out of style—but investors should look beyond the style indices for active strategies that aim to capture return potential in complex market conditions.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein