The media and some market observers are bracing for a blizzard of BBB-rated bonds to get downgraded to junk as the credit cycle turns. We expect it will be closer to a flurry.

Investors are right to be concerned, of course. US corporate debt surged when interest rates were low. And companies at the bottom of the investment-grade credit ladder were among the biggest borrowers.

BBB bonds accounted for nearly half the US investment-grade index when 2018 began, from about 33% in late 2008. Excluding financial issuers (whom regulators have forced to deleverage since the crisis), BBBs went from 52% in 2008 to 57% in this year.

It’s important to remember, though, that not all BBB-rated bonds are the same. Investors who can separate the strong from the weak before the credit rating agencies act may be able to improve their return potential.

Rising Rates, Rising Anxiety

BBB credits are in the spotlight now because rising rates and inflation are pushing up firms’ financing and input costs, squeezing profit margins. Some investors worry that billions of dollars’ worth of debt could tumble to junk, locking in losses for anyone who owns these “fallen angels,” as ex-high-grade bonds are known. A mass downgrade to junk would spark disruptive repricing in the high-yield market, too.

We understand why these concerns are keeping some bond investors up at night. But it’s important to keep things in perspective. Will some issuers lose their investment-grade status? Of course. But predicting when is difficult. The process for many could take years to play out, especially with the US economy still likely to grow in 2019.

Based on our credit analysis and expectation for continued—if slower—US growth next year, we estimate that a small percentage of the investment-grade market is at risk of a downgrade to high yield, and not all at once.

That’s not insignificant. But it’s hardly a blizzard.

Not All BBBs Are Created Equal

The problem, as we see it, is that the market hasn’t been doing a great job of factoring the differences among BBB issuers into how their bonds are priced. This is largely because the rating agencies have so far given companies a lot of leeway when it comes to maintaining an investment-grade rating—even when the credit metrics say they should be high yield. In many cases, the agencies have given companies credit for deleveraging plans that have yet to become reality.

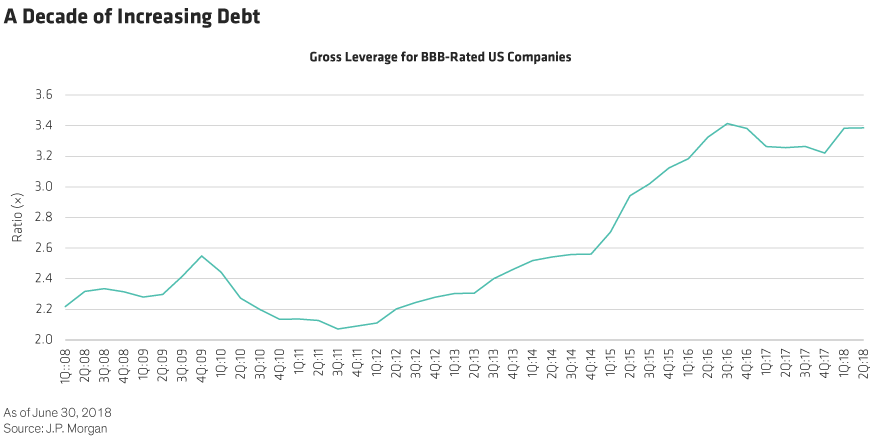

Nearly every company in the index took on more leverage over the last decade when interest rates were at record lows, with the median gross leverage for BBB-rated industrials rising from 2.2 times earnings in 2008 to nearly 3.4 times in mid-2018 (Display). That paved the way for some to misallocate capital. Now, with rates rising and liquidity scarcer, firms that misused their capital are slowly being exposed.

This is why it’s important to know how much firms borrowed—and what they did with the money—when assessing fallen angel risk.

For example, companies in the food-and-beverage sector whose business models are facing disruption ramped up leverage aggressively—often by as much as five times their earnings. Their intention was to “buy” growth through mergers and acquisitions. In many cases, these tactics didn’t work. And with food companies no longer able to rely on their brands to give them pricing power, investors shouldn’t assume they’ll be able to reduce debt quickly. That leaves them vulnerable to a downgrade.

Compare that with a wireless or cable satellite company facing similar challenges but with half the leverage. These issuers have time yet to fine-tune their business models as they try to diversify and stay profitable.

Energy—another sector in the BBB universe that’s seen a sharp increase in leverage over the years—is in better shape because the companies that avoided downgrades to high yield after oil prices plunged in 2014 have cut costs and prioritized debt reduction over dividends and share buybacks.

Pharmaceutical companies, meanwhile, never really pushed the limits of investment grade, leaving them with more sustainable debt loads and lower downgrade risk.

An Active Approach Can Help

Using our own internal ratings, we can isolate those investment-grade bonds that come with high-yield risk but investment-grade prices. The securities that fall into this category are the ones we consider most vulnerable to a downgrade.

That’s important for all types of investors to know. For managers who are prohibited from owning high-yield bonds, avoiding the riskiest BBBs in today’s market should be a top priority. Since these investors must sell any high-yield credits, they’ll be better off unloading the vulnerable securities before the rating agencies act.

For investors who can hold high-yield debt, owning some of these angels after they’ve fallen may make sense. This is because fallen angels tend to enter the high-yield universe undervalued relative to their credit fundamentals and often end up outperforming original-issue high-yield bonds. Many of the BBB companies at risk of a downgrade are still profitable, and losing their investment-grade status may act as an incentive for them to repair their balance sheets.

This is where having an active investment approach can help. Managers who do their own internal credit analysis don’t have to rely on official ratings and can avoid bonds that aren’t properly compensating investors for their risk.

Taking risk is part and parcel of investing in corporate bonds. Downgrades can be upsetting and can make credit markets more volatile in the short run. But as valuations adjust, investors will be better able to ensure that they’re being properly compensated for the risks they’re taking.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein